CapitaLand Limited (SGX: C31) is one of the largest real estate corporations in Asia. As at 30 June 2017, it owns and manages a global property portfolio worth over S$80 billion comprising residential and commercial developments, retail malls, serviced residences, and real estate investment trusts (REITs).

In this article, I’ll bring a detailed account of CapitaLand’s achievements thus far, the challenges it faces, and its targets for the immediate future. Here are the 10 things you need to know about CapitaLand before you invest.

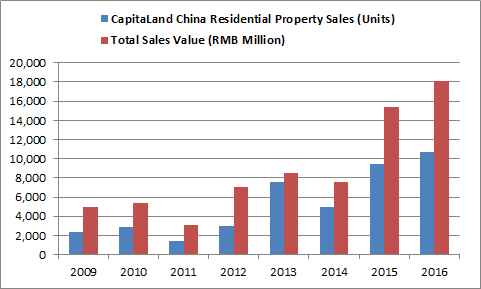

1. CapitaLand China is the main revenue contributor of CapitaLand, accounting 45.2% of group revenues in 2016. Presently, it is a leading foreign real estate developer in China with a presence in major cities such as Beijing, Tianjin, Shanghai, Hangzhou, Suzhou, Ningbo, Guangzhou, Shenzhen, Chengdu, Chongqing and Wuhan. Over the last seven years, CapitaLand China has achieved a CAGR of 23.87% in the number of residential property units sold, from 2,400 units in 2009 to 10,738 units in 2016. In terms of total sales value, it increased from RMB5.0 billion in 2009 to RMB18.1 billion in 2016. As such, CapitaLand China is also the fastest growing division of CapitaLand Limited.

Source: Annual Reports of CapitaLand

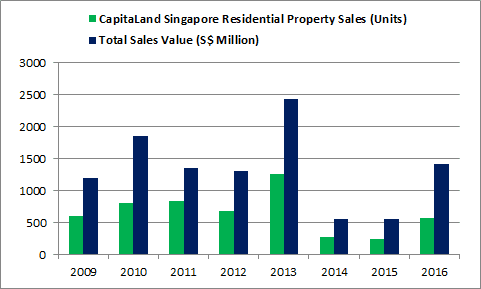

2. CapitaLand Singapore is the second largest revenue contributor, accounting 22.7% of group revenues in 2016. This division recorded lower property sales from 2014 to 2016 as it was impacted by the ongoing property cooling measures undertaken by the Singapore government since 2013.

Source: Annual Reports of CapitaLand

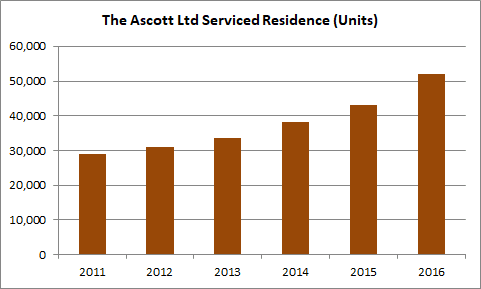

3. The Ascott Limited is the third largest revenue contributor, accounting 19.6% of group revenues in 2016. Presently, The Ascott is one of the leading multinational serviced residence owners and operators in the world. Over the last five years, The Ascott has achieved a CAGR of 12.39% in the number of serviced residence units in its portfolio, from 29,000 units in 2011 to 52,000 units in 2016.

Source: Annual Reports of The Ascott Limited

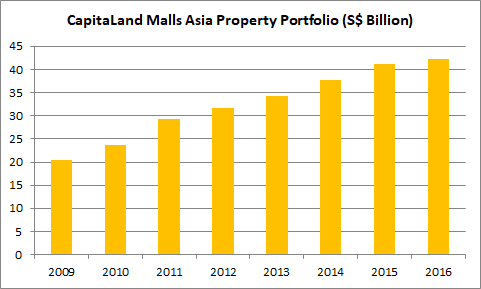

4. CapitaLand Malls Asia is the fourth largest revenue contributor, accounting 11.2% of group revenues in 2016. As I write, it is one of the largest mall developers, owners, and managers in Asia. This division has enlarged its portfolio of retail malls from 86 in 2009 to 104 in 2016. During the period, it achieved a CAGR of 10.98% in the total value of its shopping mall properties, from S$20.4 billion in 2009 to S$42.3 billion in 2016.

Source: Annual Reports of CapitaLand

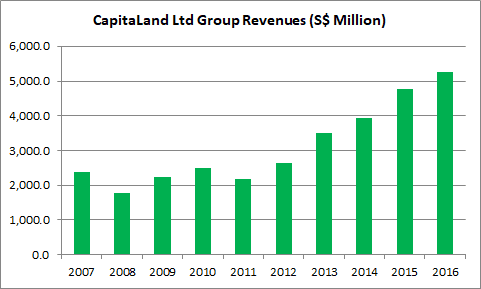

5. Overall, CapitaLand has achieved a CAGR of 19.19% in group revenues over the last five years, from S$2.18 billion in 2011 to S$5.25 billion in 2016. This is an improvement from the flat sales recorded from 2007 to 2011. The growth was directly attributed to higher property sales achieved by CapitaLand China and sales contributed from The Ascott from 2011 onwards.

Source: Annual Reports of CapitaLand. Revenue excludes sales derived from Australand as Australand was disposed in 2014.

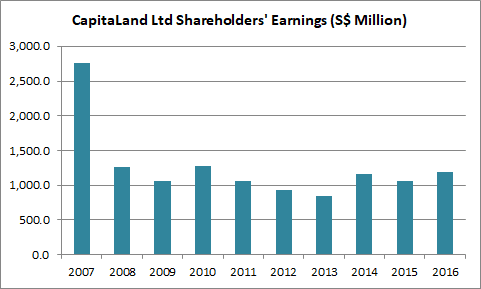

6. In 2007, CapitaLand reported S$2.76 billion in shareholders’ earnings. Profits were inflated high due to the S$918.5 million in divestment gains from several properties including 8 Shenton Way, a 50% stake in Chevron House, and a 45% stake in AIG Tower in Hong Kong. Australand also boasted higher profits then but has since been disposed in 2014. From 2008 onwards, CapitaLand’s shareholders’ earnings has hovered around S$1 billion a year. Profits remain flat despite a substantial increase in group revenues over the last five years. This is because CapitaLand has received lower profits from its investments in associate and joint venture companies. Overall, CapitaLand has an average five-year return on equity of 6.21%.

Source: Annual Reports of CapitaLand Ltd. The profit figures for 2012 and 2013 was restated as Australand was disposed in 2014.

7. From 2007 to 2016, CapitaLand generated S$5.51 billion in cash flows from operations. During the period, it received S$3.79 billion in dividends from its investments in associate and joint venture companies. It also raised S$8.8 billion in net equities and net long-term debt. Out of which, CapitaLand Ltd has spent:

- S$1.49 billion in capital expenditures

- S$1.23 billion in net acquisitions of subsidiaries

- S$4.31 billion in net acquisitions of associate & joint venture companies

- S$4.36 billion in net acquisitions of investment properties

- S$3.49 billion in dividend payments to shareholders

CapitaLand has been using a combination of positive cash flows from operations, dividend income, and long-term borrowings to expand its property portfolio and reward its shareholders with dividends. As at 30 June 2017, CapitaLand Ltd has S$4.82 billion in cash reserves, a current ratio of 1.77, and a debt-to-equity ratio of 0.81.

8. CapitaLand has an average five-year dividend payout ratio of 33.09%. During the period, CapitaLand increased its dividend per share from 7.0 cents in 2012 to 10.0 cents in 2016. As at 27 October 2017, CapitaLand Ltd is trading at S$ 3.73 a share. If CapitaLand maintains its dividend per share at 10.0 cents, its expected dividend yield is 2.68%.

| 2012 | 2013 | 2014 | 2015 | 2016 | |

|---|---|---|---|---|---|

| Dividend per share (in Singapore cents) | 7.0 | 8.0 | 9.0 | 9.0 | 10.0 |

9. Invariably, CapitaLand Ltd faces several risks which are inherent to the property industry. For instance:

- As at 30 June 2017, CapitaLand Ltd has S$4.76 billion worth of development properties held for sale, mainly in Singapore and China. Weak demand arising from an oversupply of residential properties, unfavourable government policies, and a slowdown in the economy could lead to downward pressure in future selling prices of these properties. Thus, there is a risk of incurring losses if the future selling prices of these properties are lower than their net realisable values or their development costs.

- As at 30 June 2017, CapitaLand Ltd has S$18.6 billion worth of investment properties. It is the single largest category of assets on its balance sheet. The valuation of these investment properties are highly sensitive to key assumptions such as capitalisation, discount, and terminal yield rates. Thus, a small change in the assumptions can have a significant impact to the valuation of these investment properties.

10. CapitaLand Ltd has revealed its targets to be achieved over the next few years. For instance:

- CapitaLand China has a strong pipeline of projects as it expects to complete over 10,000 residential units in the 2H 2017 and 2018. This ensures future revenue recognition to CapitaLand Ltd for both 2017 and 2018.

- CapitaLand is embarking on numerous commercial & integrated development projects. These include Suzhou Centre Mall, Capital Square in Shanghai, LuOne in Shanghai, Capital Tower in Shanghai, Raffles City Chongqing, Funan in Singapore, and the redevelopment of Golden Shoe Car Park in Singapore. They will be completed progressively over the next 4-5 years.

- CapitaLand Malls Asia is targeting to open five retail malls in 2017. One of the malls, Melawati Mall in Malaysia opened on 26 July 2017 with 71% in committed occupancy. In addition, CapitaLand Malls Asia intends to open another 12 retail malls in 2018 and beyond, bringing its total number of retail malls to 109.

- The Ascott has acquired an additional 60% stake in Quest Apartment Hotels in Australia, a freehold 100-unit serviced residence known as Quest Cannon Hill, and an 80% stake in Synergy Global Housing in the United States. Thus, The Ascott has increased its number of serviced residence from 52,000 units in 2016 to 70,000 units presently. The Ascott expects to open the Ascott Raffles City in Shenzhen in 2017 and Ascott Culture Village in Dubai between 2018 and 2020. Therefore, The Ascott Ltd is well on track to achieve its target of surpassing 80,000 serviced residence units by 2020.

The fifth perspective

Since 2008, CapitaLand Ltd has consistently made S$1 billion a year in profit and steadily increased its dividend payments to shareholders over the last five years. Presently, approximately 79% of its total assets are investment properties which contribute recurring income to CapitaLand. They add stability and income visibility to CapitaLand Ltd as it rides through market uncertainties with a resilient integrated business model. Moving ahead, CapitaLand Limited looks well-positioned to achieve its targets by pursuing opportunities to grow its property portfolio across Asia.

Interested in property conglomerates like CapitaLand, City Developments, and more? Here’s how you can invest profitably in property conglomerates in Singapore and Hong Kong.