Public Bank Berhad (Bursa: 1295) is the third largest banking group in Malaysia. As I write, Public Bank is worth RM78.62 billion in market capitalization.

In this article, I’ll bring a detailed account of Public Bank’s tremendous success and achievements thus far and its outlook towards the near future. Therefore, here are 16 things you need to know about Public Bank before you invest.

Track record

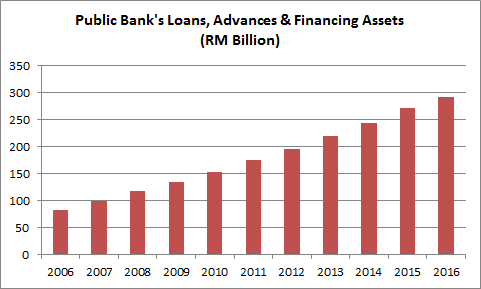

1. Public Bank has achieved a CAGR of 13.45% in loans, advances and financing assets over the last 10 years. It increased from RM82.79 billion in 2006 to RM292.43 billion in 2016. This is due to growth in lending in major segments such as purchase of residential and non-residential properties, purchase of vehicles, and working capital during the 10-year period.

Source: Public Bank annual reports

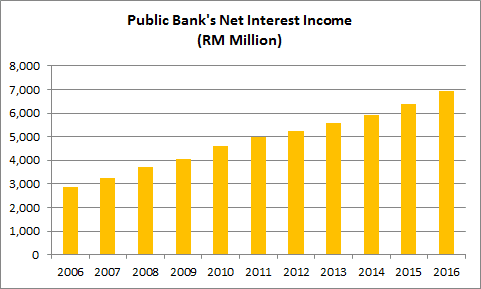

2. Public Bank has achieved a CAGR of 9.20% in net interest income over the last 10 years. It has increased from RM2.87 billion in 2006 to RM6.92 billion in 2016. This is because the continuous growth in Public Bank’s loans, advances and financing assets has exceeded its marginal decline in net interest margins during the period.

Source: Public Bank annual reports

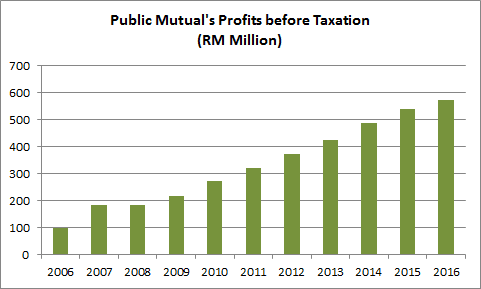

3. Public Mutual, a wholly-owned subsidiary of Public Bank, is the market leader in the unit trust industry in Malaysia with retail market share of 45.8% in February 2017. Over the last 10 years, Public Mutual has expanded its number of funds and enlarged its total assets under management (AUM) from RM16.19 billion in 2006 to RM70.29 billion in 2016. Consequently, Public Mutual has achieved consistent growth in both operating revenues and profits before taxation (PBT). From 2006 to 2016, operating revenues have grown from RM244.5 million in 2006 to RM967.5 million in 2016. Meanwhile, PBT increased from RM97.3 million in 2006 to RM572.9 million in 2016.

Source: Public Bank annual reports

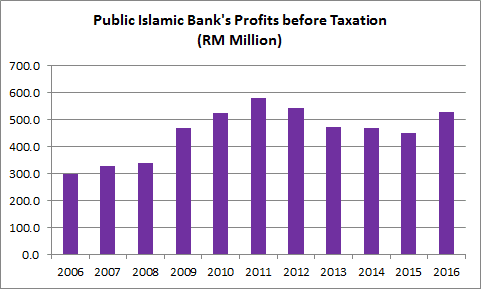

4. Public Islamic Bank, another wholly-owned subsidiary of Public Bank, has achieved a CAGR of 5.82% in profits before taxation (PBT) over the last 10 years. Overall, it increased from RM300.3 million in 2006 to RM528.7 million. In contrary to most segments which recorded consistent growth in profits, Public Islamic Bank has recorded lower PBT from RM581.0 million in 2011 to RM450.1 million in 2015 after a period of growth. This is because the increase in funding costs has exceeded Public Islamic Bank’s growth in gross financing assets during the period.

Source: Public Bank annual reports

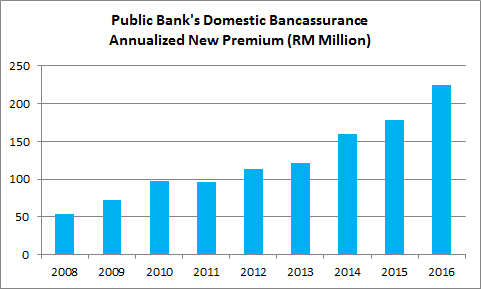

5. On 7 November 2007, Public Bank entered a 10-year exclusive distribution agreement with ING Insurance to provide life, health and investment-linked insurance products in Malaysia and Hong Kong. The bancassurance distribution agreement came into effect on 1 January 2008. Since then, Public Bank has achieved a CAGR of 19.56% in domestic annualized new premiums over the last eight years. It increased from RM53.8 million in 2008 to RM224.6 million in 2016.

Source: Public Bank annual reports

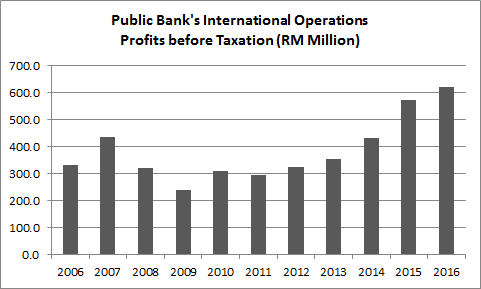

6. Public Bank has a regional presence in five countries including Hong Kong, Cambodia, Vietnam, Laos, and Sri Lanka. At present, Hong Kong and Cambodia remain the two largest profit contributors to Public Bank’s international operations division. From 2007 to 2009, this division reported a decline in PBT due to the global financial crisis. Since then, this division has achieved a CAGR of 14.55% in PBT from RM239.9 million in 2009 to RM620.7 million in 2016.

Source: Public Bank annual reports

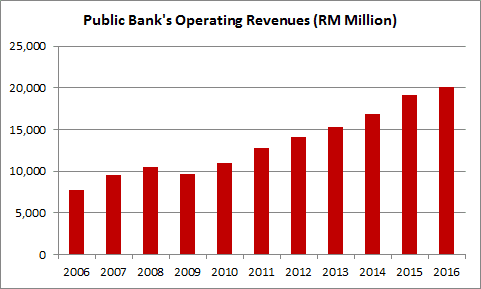

7. As a result, Public Bank has achieved a CAGR of 10.06% in operating revenues over the last 10 years. It increased from RM7.71 billion in 2006 to RM20.10 billion in 2016. This is directly contributed by continuous growth in net interest income and operating revenues of Public Mutual, Public Islamic Bank, bancassurance and its international operations as explained in Points 1-6.

Source: Public Bank annual reports

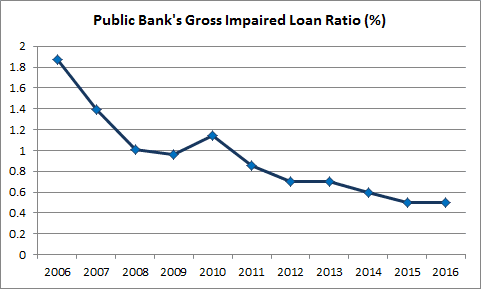

8. Public Bank has improved the quality of its loans, advances and financing assets over the last 10 years. This is evident as Public Bank has reduced its gross impaired loan ratio from 1.87% in 2006 to 0.50% in 2016. It is the lowest in the local banking industry.

Source: Public Bank annual reports

9. Public Bank has kept its cost-to-income ratio between 30% to 35% over the last 10 years. In 2016, Public Bank recorded 32.3% in cost-to-income ratio. Evidently, it is below the industry average of 45.8% and the lowest among its peers. This is due to adopting disciplined cost management across all its business operations.

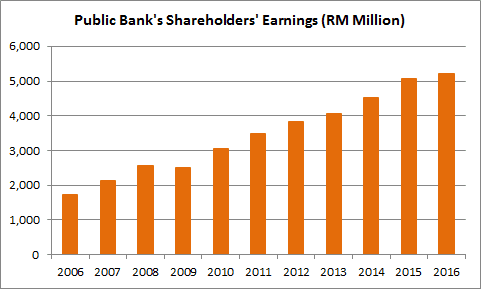

10. As a result, Public Bank has achieved a CAGR of 11.67% in shareholders’ earnings over the last 10 years. Earnings increased from RM1.73 billion in 2006 to RM5.21 billion in 2016. This is contributed by continuous growth in group operating revenues and a stable cost-to-income ratio during the period.

Source: Public Bank annual reports

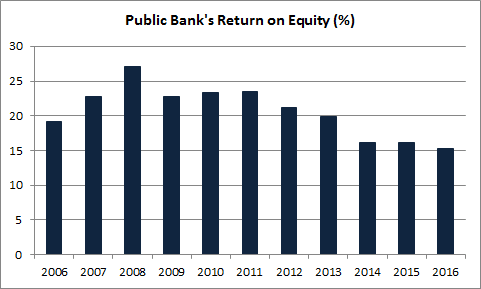

11. Over the last three years, Public Bank has recorded an ROE of 15% to 16% a year. This means, Public Bank has made, on average, RM15-16 in annual earnings from every RM100 in shareholders’ equity from 2014 to 2016. The level of ROE recorded from 2014 to 2016 is lower than the ROE recorded from 2007 to 2013 which was above 20% a year. This is despite a continuous growth in shareholders’ earnings over the last three years. It is because Public Bank has substantially increased its shareholders’ equity when it undertook a rights issue exercise in 2014. It is an effort of Public Bank to be well-capitalized to meet the requirements of the implementation of Basel Ⅲ in advance.

Source: Public Bank annual reports

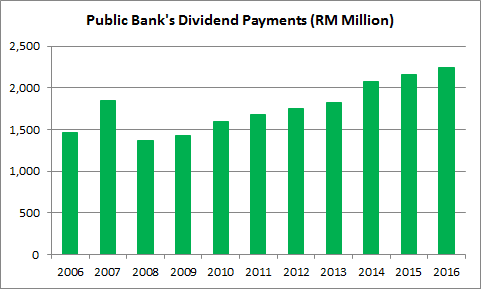

12. Public Bank has achieved a CAGR of 4.37% in dividend payments over the last 10 years. Dividends increased from RM1.46 billion in 2006 to RM2.24 billion in 2016. Evidently, the growth in dividend payments did not keep pace with its growth in shareholders’ earnings. Thus, Public Bank recorded lower dividend payout ratios for the latest five-year period (2012-2016) compared to the five-year period (2007-2011). From 2012 to 2016, Public Bank maintained a dividend payout ratio at 40% to 50% a year. This means, it has paid out, on average, RM40-50 in dividends from every RM100 in shareholders’ earnings during the period.

Source: Public Bank annual reports

13. Public Bank reported a total capital ratio of 15.2% in Q1 2017. It is above the total regulatory requirement of 9.25% set by Bank Negara Malaysia for 2017. The total regulatory requirement is the addition of 8.0% in minimum total capital and 1.25% in phase-in capital conservation buffer for 2017.

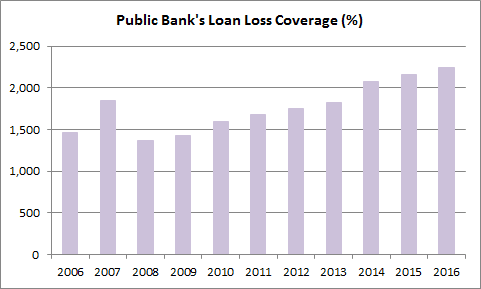

14. Public Bank reported a loan loss coverage of 104.0% in Q1 2017. It is currently above the industry average of 96.3% set by Bank Negara Malaysia in 2016. This means, Public Bank has set aside sufficient provisions to cover non-performing loans.

Source: Public Bank annual reports

Moving forward…

15. Public Bank has revealed six key performance targets for 2017. This include:

| 2016 Target | 2016 Actual | 2017 Target | |

|---|---|---|---|

| Net Return on Equity | >15% | 16.5% | 14-15% |

| Total Capital Ratio | >13% | 15.5% | >13% |

| Gross Impaired Loan Ratio | <1% | 0.5% | <1% |

| Cost-to-Income Ratio | <33% | 32.3% | 33-34% |

| Group Loan Growth | 8-9% | 7.5% | 6-7% |

| Group Deposit Growth | 7-8% | 2.9% | 5-6% |

Source: Public Bank annual reports

16. To achieve its targets for 2017, Public Bank has revealed areas of strategic focus. This include:

- Lending business. Public Bank’s consumer lending will focus on purchases of residential and non-residential properties and passenger vehicles. It will also continue to penetrate mid-market SME financing.

- Deposit-taking business. Public Bank will attempt to strike a balance between deposit growth and cost of funding by securing higher retail and lower cost deposits.

- Non-interest income. Public Bank will expand its fee-based income such as unit trust funds, bancassurance, card business, cash management services, remittance services and trade finance.

- International operations. Public Bank acquired the remaining 50% shareholding of Public Bank Vietnam Limited and as of 1 April 2016 is fully owned by Public Bank Berhad. In 2017, Public Bank Vietnam will expand as it targets to open six new branches in Vietnam.

The fifth perspective

In summary, Public Bank has built a track record of maintaining asset quality and delivering growth in operating revenues and shareholders’ earnings over the last 10 years.

In Q1 2017, Public Bank reported RM1.25 billion in shareholders’ earnings and placed itself for a positive start for 2017. Looking ahead, Public Bank is committed to take proactive efforts to sustain growth and quality in loans, advances and financing assets, maintain a healthy funding structure, drive non-interest revenues, promote high productivity and cost efficiency to ensure it remains on trajectory towards meeting its growth targets for 2017.