Photo credit: carrotmadman6 from Maritius

In 1993, Patrick J. Cusatis, James A. Miles and J. Randall Woolridge did a research study on the stock performance of spinoff companies from 1963 to 1988. From the research, they found that spinoffs outperformed the S&P 500 by about 10% per year in the first three years of their independence. The study also found that parent companies of spinoffs also outperformed the index by more than 6% per year for the same three years.

A 1999 McKinsey study researched the performance of spinoffs between 1988 and 1998 and showed that spinoffs gave shareholders 27% annualized returns over two years vs. 17% for the S&P 500.

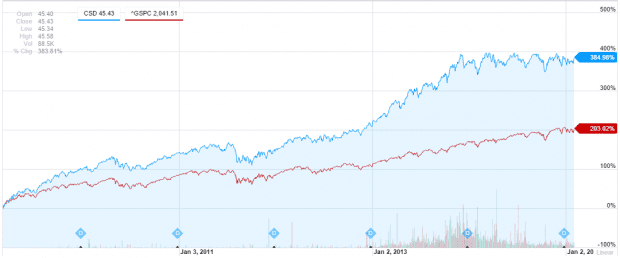

The Guggenheim Spin-Off ETF, which is based on the Beacon Spin-Off Index, has also generated a return of 384% since the March 9th 2009 bottom compared to 203% for the S&P 500 in the same time period.

Chart: Yahoo Finance

It looks as if investing in spinoffs are a great way to boost your investment returns in the short term!

What are Spinoffs?

Spinoffs are a form of corporate restructuring where a parent company, usually a conglomerate, decides to separate a subsidiary business as a new independent entity.

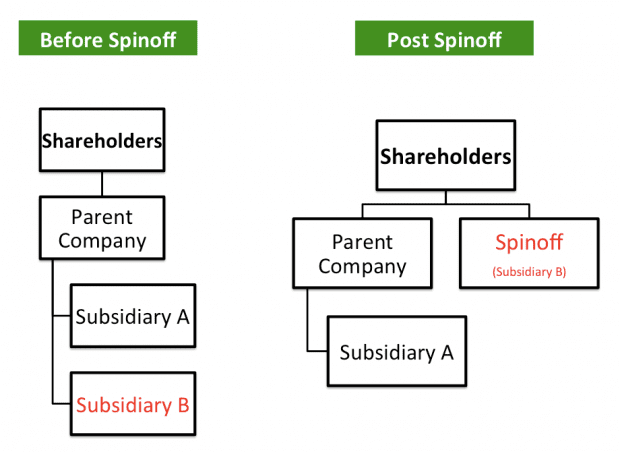

Referring to the diagram below: Pre-spinoff, shareholders only own shares of the parent company. The parent company owns two different businesses — subsidiary A and B. When subsidiary B is spun off as a new entity, the parent company will distribute the shares of this new company to existing shareholders.

Post-spinoff, shareholders now own shares of the parent company and the spinoff (Subsidiary B). The spinoff will have its own management team and board of directors, different from its parent company.

Types of Spinoffs

The scenario we described above is what we called a regular spinoff where 100% of the spinoff’s shares are distributed to shareholders of the parent company. But there are cases where management does a carve-out or split-off.

A carve-out happens when a parent company decides to sell a full or partial stake in its subsidiary to the public through an IPO. Unlike regular spinoffs, carve-outs raise fresh capital (cash) since shares are sold to the public via its IPO.

A split-off happens when a parent company offers shareholders to exchange their shares for shares of the new split-off. The new shares are usually offered at a discount. For example, the parent company will offer shareholders the option to exchange $100 worth of shares for $110 worth of the new split-off’s shares.

Why Spinoffs Outperform the Index in the Short Term

- Markets and investors generally favor pure play companies that are focused on one core business. Conglomerates, on the other hand, have the complexity of owning and operating multiple different businesses units under their umbrella.

- Many spinoffs are spun off to realize their full value as subsidiaries are usually undervalued when merged with its parent company. For this reason, many spinoffs significantly rise in value the moment they are separated

- Spinoffs have a smaller market capitalization compared to its parent. Consequently, many fund managers have to sell shares of spinoffs when they receive them because their funds’ mandate is to invest in large-cap companies. This sell-off drives down shares prices of the spinoff at the start, giving other investors a chance at a bargain investment.

- The new board of directors and management team usually own a stake in the spinoff. They are largely compensated based on equity incentives which is tagged to the performance of the new spinoff. It is their interest to ensure that the spinoff performs well.