For most people, value investing makes a lot of sense. Find a business worth a dollar and buy it for 50 cents. Easy enough. And yet, many people (even self-professed long-term investors) find it extremely challenging to implement this in practice. Investors routinely enter the market at high points, only to exit collectively at the low points.

This isn’t for a lack of trying or expertise. Institutional behaviour is equally complicit in promoting this herd like mentality. There is no doubt in my mind that individuals armed with CFAs and MBAs working at investment management firms or brokerages are overwhelmingly hardworking and intelligent. And yet, the results of mutual funds, and even hedge funds have been overwhelmingly negative. Academic evidence has shown convincingly that investors would be far better of investing in low cost index funds.

But why is this so?

Market psychology and history are more important than you think

The technical aspects of fundamental analysis are easy enough to pick up. With some effort and diligence, anyone can understand quite easily read a balance sheet, calculate the financial ratios and make a reasoned judgment as to whether a company is a worthwhile investment candidate. The proliferation of resources available on the web make it far easier than ever to learn from the best and little costs.

What is lacking however, is enough information on the behavioural element of investing. Benjamin Graham dedicated a chapter to it in his seminal work, The Intelligent Investor. This ‘He’ refers to a business partner (aptly named “Mr. Market), who is manic-depressive, with his mood swinging from very pessimistic to wildly optimistic. Although the investor is free to decline Mr Market’s offer for his shares, many do not.

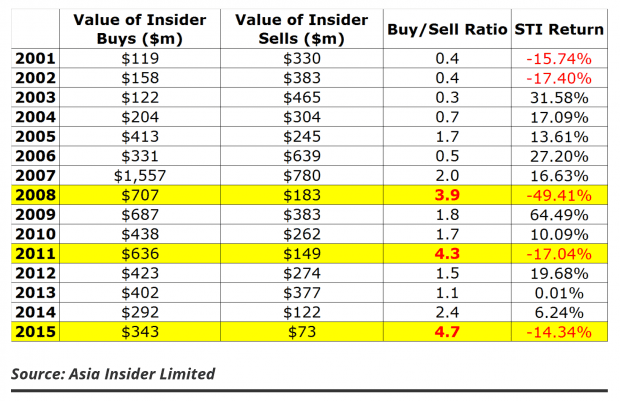

How many investors would be actively buying when such doom and gloom pervades the markets? And yet, without such headlines, one does not find “screaming bargains”. Investors can have cheap valuations or good news, but not both.

To the point, it’s easy enough to be a long-term investor when markets are going up – but it becomes far more challenging when you are underwater by 20% after the first six months. At this point, most investors choose to fold, abandoning their conviction.

Conviction without experience cannot be sustained

For retail investors, investing isn’t a full time profession. Most of the excitement comes from the initial euphoria of finding an “undervalued stock”. It’s the same excitement that is generated from “hot-tips”, or buying in a rising market. Unsurprisingly most investors tend to direct their attention here.

What is missing is an understanding of what happens after this. Investors are often surprised or shocked when prices move against them, or worst, a complete reversal of sentiment in the span of a few short months. Conviction without experience cannot be sustained. Doubts creep in, and questions about one’s judgment’s surfaces. Unfortunately, at this point, there is no way for an investor to know whether he is right or wrong. He has not accumulated enough experience on what to do.

History doesn’t repeat itself, but it sure does rhyme

“Those who don’t know history are doomed to repeat it.” – Edmund Burke

There are two ways to accumulate the experience needed to withstand the vicissitudes of the markets. The first is to experience it yourself. The obvious challenge is that market cycles can move in the duration of years, and it’s very hard to differentiate luck from skill. Bull markets often produce their own “heroes” who disappear as the tide recedes.

The better alternative in my view is to understand how markets work – not by understanding theories, but by understanding its history. In this vein, it is easy to understand why famed investors such as Jim Rogers, Warren Buffett or Charlie Munger advocate reading so much. It is the only way to gain a wide understanding of the forces that drive markets in a short span of time.

Plus ça change, plus c’est la même chose

“The more things change, the more they stay the same” – Jean-Baptiste Alphonse Karr

Herein my favourite quote lies a simple truth. No matter the type of political system, the country or the era, people never change. We are still prone to herd like behaviour, swing from greed to fear and back to greed again.

2015 was a year when this was exhibited in full force. Stock markets which once played little importance and were neglected suddenly sprung to life in China. The initial surge in profits from speculators led to more euphoria, and soon even farmers were in the game!

I remember vividly that manufacturers were declaring that making money in the stock market was far easier. References were made constantly about the Central Party, and how it would not let the market fall.

The outcome was predictable (even if the timing of its demise was not), and euphoria soon turned to widespread fear. The government soon turned to finding villains (short sellers, foreign speculators, corrupt officials) and to propping up the stock market by intervening in the market directly.

If any of this sounds familiar, it’s because a similar sequence of events resulted in the Great Financial Crisis in 2008 (watch The Big Short for a hilarious rendition of what happened). Investors were raking in “easy profits” from flipping houses. When the party ended, the government intervened heavily in the market, and the usual blame game around short sellers begun.

The 80/20 rule of investing

If there’s one point in which I hope to impress on you today, it’s that knowing your market history is pivotal in crafting an investment strategy… and actually implementing it. If I were to hasten a guess, my own estimation is that 80% of one’s results in fact comes from not the fundamentals, but in understanding the psychology of investing.

To that end, I have compiled 3 books which provide a road map that captures the important moments of history that I believe are crucial creating a solid bedrock of information to proceed on.

- Bull! – Maggie Mahar

- Devil Take the Hindmost: A History of Financial Speculation – Edward Chancellor

- Too Big to Fail: Inside the Battle to Save Wall Street – Andrew Ross Sorkin

Enjoy the reads!