Sino Grandness (SGX: T4B) is a China-based company listed on the SGX. The company is known for its loquat fruit juice which the company claims to have an 86% market share in China. The loquat fruit juice is housed under the company’s brand of fruit juices called Garden Fresh/鲜绿园. The brand is distributed not only in China but also internationally across the rest of Asia, Europe, and North America.

In 2013, Sino Grandness was considered a hot stock when its share price surged three-fold to as high as $1.60 in six months. My friend’s dad asked my opinion on Sino Grandness while we were playing a friendly game of Texas hold’em. I will not tell you what I told him that night but he basically gave the company a miss after he lost his stack of poker chips to his son. True story.

I thought I’d ever have to take a look at Sino Grandness again but we recently received a submission from Mr. Chua, one of our Alpha Lab members, who emailed us to request a case study on Sino Grandness and to include it on the watchlist of companies we monitor closely in Alpha Lab. (Thanks, Mr. Chua for the suggestion!) We took his suggestion onboard and I was assigned to look up the latest developments on Sino Grandness. Here is what I discovered.

Since its successful listing in 2009, Sino Grandness’s sales and earnings have grown by more than sevenfold to RMB3.3 billion and RMB0.5 billion respectively in 2015! (Realizing this, I’m lucky I haven’t received a call from my friend’s dad – and, possibly, why I have not been invited to a poker game since. Oops.)

At the time of this writing (7 August 2016), the share price of Sino Grandness is trading at $0.54 (the company did a 2-for-1 share split in 2013), its market cap is RMB1.73 billion (S$346 million) — which is equivalent to only 3.46 times earnings.

This sounds like an ideal value stock, doesn’t it?

Hold it there.

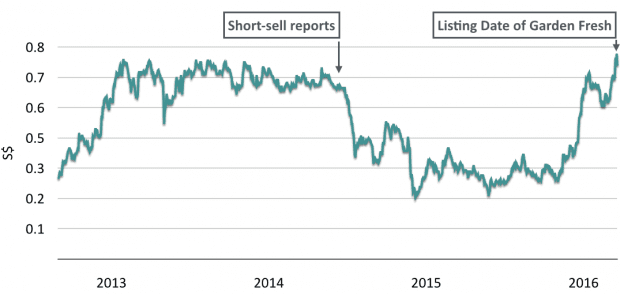

About a year after the poker game with my friend and his father, Sino Grandness was accused of overstating its sales and earnings by a user called “newman9” on valueinvestorsclub.com. Sino Grandness denied the allegations and the CEO flew to Singapore to calm shareholders down. Despite the CEO’s efforts, the share price of Sino Grandness headed downhill.

A month after the short seller’s first report, newman9 released another supplemental follow-up report with more proof that Sino Grandness misrepresented its financials. With two convertible bonds amounting to RMB652 million maturing in mid-2015, shareholders were worried if the company could pay off its debt assuming the short seller’s claims were true. The chain of events mercilessly shaved off Sino Grandness’s value by more than half from its peak.

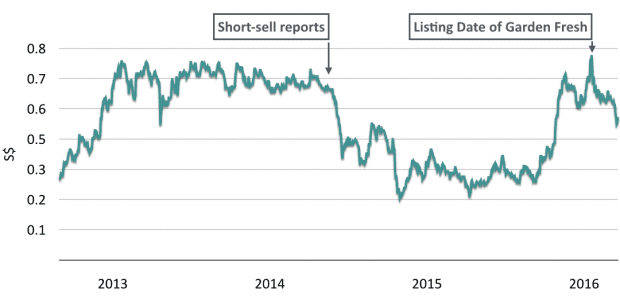

However, in a recent turn of events, Sino Grandness’s share price rebounded sharply in the first quarter of 2016 after shareholders approved the proposed listing of a subsidiary, Garden Fresh on the Hong Kong Stock Exchange on 6 July 2016. Garden Fresh accounted for 77% of Sino Grandness’s bottom line in 2015. If the listing is successful, shareholders can expect hidden value to be unlocked from the spin-off. Sino Grandness also announced it will redeem 40% of its outstanding bonds while the remaining bonds will be converted into shares of Garden Fresh.

The proposed listing of Garden Fresh and the restructuring of the convertible bonds were seemingly sufficient to nullify past concerns and lifted the share price back to levels last seen before the panic.

However, the share price of Sino Grandness seems to be losing steam again after Garden Fresh missed its expected listing date on 6 July 2016. (What is going on?)

So instead of getting excited about the possible spin-off or its dirt-cheap valuation, I prefer to go back to basics and focus on my circle of competence – which is to invest only in companies that I can fully understand. Again, this brings me back to the underlying challenge I face then and now: Chinese companies listed in Singapore (known as ‘S-chips’) are a real tough nut to crack and are oftentimes beyond my ability to make head or tail of.

The creditability of the financial reports sometimes come into question and there is no easy way for retail investors like me to verify them. Needless to say, I can’t put total faith in third parties like auditors to establish that kind of trust.

In my opinion, Sino Grandness’s situation is complicated and if I can’t be entirely sure about an investment, the best way to safeguard my downside is to stay out and simply watch the events unfold from the sidelines. That said, I do not own any shares of Sino Grandness and have no intention to initiate a position in the near future.

After running through my analysis, it is obvious to me that we should never invest in any stock that is too complex to understand and beyond one’s circle of competence – which is why Sino Grandness is not on our watchlist in Alpha Lab. It is better (and more profitable) to focus on a number of companies that you know intimately well and can soundly monitor on a regular basis. By doing so, we can build up a watchlist of high-quality companies over the years.

I might review my stand on Sino Grandness if the management is able to return its reported profits back to shareholders in years to come without the need to continuously raise capital from shareholders/bondholders. Ideally, the sum of money returned must exceed the sum of capital raised. At this point, I don’t see this happening anytime soon and it may take years to accomplish. Therefore, Sino Grandness is off my watchlist and Alpha Lab’s.

(Photo: Sino Grandness)

Hi I totally agree with you.

My S-chip Hong Xing is still under suspension after so many years on their account problems. I went in without even doing my due diligence as then I do not wish to be out of the economic gargantuan as it started its economic growth. Anything that you are not sure, best is stay out.