It’s that time of the year again when Warren Buffett pens his annual letter to Berkshire Hathaway shareholders and the investment world sit ups and takes note of what Buffett has to share. (Buffett has been writing his annual letters since 1965 and you can read many of his past letters here.)

I shared 10 things I learned from Buffett’s 2015 annual letter the previous year and, this year, Buffett has once again dropped his usual nuggets of wisdom and one-liners as he reveals his thoughts about the continued running and growth of Berkshire Hathaway.

So here are 14 things I learned from Warren Buffett’s 2016 annual letter to Berkshire shareholders.

- Berkshire’s per-share market value has grown 1,972,595% since 1965. Its per-share book value has grown 884,319% over the same period. The reason why Berkshire’s book value lags its market value is due accounting rules that write off goodwill for Berkshire’s losing business acquisitions. Conversely, the value of winning business acquisitions (of which Berkshire has many) has never been revalued upwards. Buffett argues that, over time, stock prices gravitate towards intrinsic value, which is why Berkshire’s market value far exceeds its book value.

- Buffett candidly shared the worst deal he ever made when he acquired Dexter Shoe for $434 million in 1993. He funded the acquisition with 25,503 shares of Berkshire stock which at yearend 2016 were worth more than $6 billion. Dexter Shoe eventually folded in 2001.

- He also revealed a similarly foolish move when he issued 272,00 new shares to purchase General Reinsurance in 1998. While General Re is doing well now, the share issuance increased Berkshire’s outstanding shares by 21.8% which diluted Berkshire’s per-share value and earnings, prompting Buffett to say:

“Today, I would rather prep for a colonoscopy than issue Berkshire shares.”

- Buffett still feels that American ingenuity, ambition, and economic dynamism is here to stay. He believes the system that has allowed America, starting from scratch in 1776, to amass $90 trillion in wealth over the last 240 years will continue to “deliver abundance beyond any dreams of our forefathers”.

“American business – and consequently a basket of stocks – is virtually certain to be worth far more in the years ahead. Innovation, productivity gains, entrepreneurial spirit and an abundance of capital will see to that.”

- He reminded that no one – not him, not economists, not the media – can predict when major market panics will happen. He gave two pieces of advice for market panics:

“First, widespread fear is your friend as an investor, because it serves up bargain purchases. Second, personal fear is your enemy. It will also be unwarranted.”

- Buffett explained that share repurchases (buybacks) only make sense if the shares are bought at a price below intrinsic value.

“If there are three equal partners in a business worth $3,000 and one is bought out by the partnership for $900, each of the remaining partners realizes an immediate gain of $50. If the exiting partner is paid $1,100, however, the continuing partners each suffer a loss of $50. The same math applies with corporations and their shareholders. Ergo, the question of whether a repurchase action is value-enhancing or value-destroying for continuing shareholders is entirely purchase-price dependent.”

- He then shared two exceptions when share repurchases should not take place even when shares are underpriced – when a business needs all its available cash to protect or expand its operations and it is reluctant to take on more debt, and when an investment opportunity presents far greater value than repurchasing shares.

- Buffett repeated his stand of repurchasing Berkshire shares when (or if ever) it hits 120% of book value or less because he believes that price is a significant discount to Berkshire’s intrinsic value. However, that has been hard to do because investors are well aware of Buffett’s entry point and the market has seldom allowed Berkshire to fall near that range.

- Insurance and the property/casualty (P/C) branch of that industry has been the engine that has propelled Berkshire’s growth since 1967. Buffett was attracted to the industry because P/C insurers are able to collect large sums of float which can be used for investments to generate gains and income. Berkshire owns three major insurance operations – Berkshire Hathaway Reinsurance Group, General Reinsurnace, GEICO – and a collection of smaller companies which collectively control a float of over $100 billion.

- Buffett also shared that the P/C industry is intensely competitive and sometimes causes the industry to operate at a significant underwriting loss. However, he was happy to report that Berkshire’s P/C companies have generated an underwriting profit for 14 consecutive years, earning a pre-tax gain of $28 billion over that period.

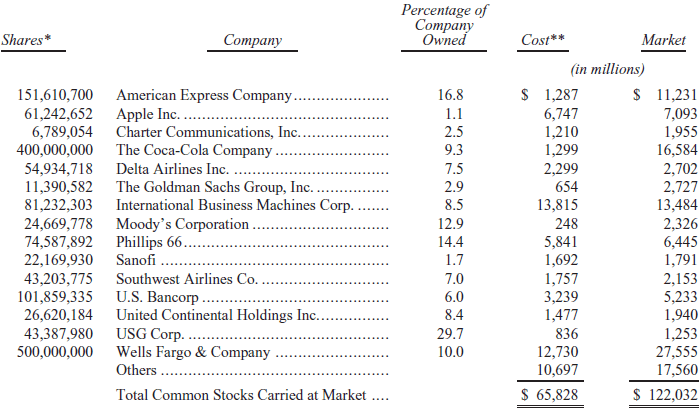

- Here are Berkshire’s top 15 largest investment holdings:

Notable additions include Apple Inc. and not one but three(!) airlines – Delta Airlines, Southwest Airlines Co., and United Continental Holdings Inc. Buffett’s aversion to tech and airline stocks is well-documented but he recently explained his change of heart and why bought into Apple and airlines.

Notable additions include Apple Inc. and not one but three(!) airlines – Delta Airlines, Southwest Airlines Co., and United Continental Holdings Inc. Buffett’s aversion to tech and airline stocks is well-documented but he recently explained his change of heart and why bought into Apple and airlines. - Berkshire still retains the warrant to purchase 700 million shares of Bank of America for $5 billion before 2 September 2021. As at 6 March 2017, that stake would be worth more than three times that amount at $17.8 billion. Berkshire currently owns $5 billion worth of Bank of America preferred shares which pay $300 million in dividends every year. Buffett has mentioned he could use the preferred shares to satisfy the cost of the warrant.

- Buffett clarified that he has never mentioned that would hold a stock “forever”.

“It is true that we own some stocks that I have no intention of selling for as far as the eye can see (and we’re talking 20/20 vision). But we have made no commitment that Berkshire will hold any of its marketable securities forever.”

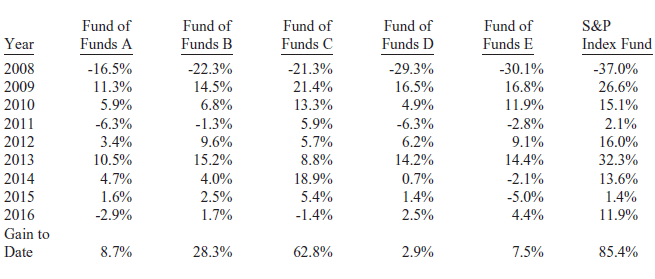

- Finally, Buffett gave an update of his half-million 10-year bet that a low-cost index fund would outperform a portfolio of funds of hedge funds after accounting for fees, costs, and expenses.

“I publicly offered to wager $500,000 that no investment pro could select a set of at least five hedge funds – wildly-popular and high-fee investing vehicles – that would over an extended period match the performance of an unmanaged S&P-500 index fund charging only token fees. I suggested a ten-year bet and named a low-cost Vanguard S&P fund as my contender. I then sat back and waited expectantly for a parade of fund managers – who could include their own fund as one of the five – to come forth and defend their occupation. After all, these managers urged others to bet billions on their abilities. Why should they fear putting a little of their own money on the line?”

Only one fund manager, Ted Seides, took up Warren’s bet and picked five funds-of-funds whose returns were to be averaged and compared against the Vanguard S&P index fund. These are the returns so far over nine years:

Overall, the index fund compounded 7.1% annually while the five fund-of-funds only compounded 2.2% annually. Buffett estimated that around 60%(!) of all gains made by the five fund-of-funds were swallowed up by fees and reiterated his point that investors could have achieved better returns on their own – with virtually no cost. Buffett will be donating his winnings to charity.

Notable additions include Apple Inc. and not one but three(!) airlines – Delta Airlines, Southwest Airlines Co., and United Continental Holdings Inc. Buffett’s aversion to tech and airline stocks is well-documented but he recently explained his change of heart and why bought into

Notable additions include Apple Inc. and not one but three(!) airlines – Delta Airlines, Southwest Airlines Co., and United Continental Holdings Inc. Buffett’s aversion to tech and airline stocks is well-documented but he recently explained his change of heart and why bought into  Overall, the index fund compounded 7.1% annually while the five fund-of-funds only compounded 2.2% annually. Buffett estimated that around 60%(!) of all gains made by the five fund-of-funds were swallowed up by fees and reiterated his point that investors could have achieved better returns on their own – with virtually no cost. Buffett will be donating his winnings to charity.

Overall, the index fund compounded 7.1% annually while the five fund-of-funds only compounded 2.2% annually. Buffett estimated that around 60%(!) of all gains made by the five fund-of-funds were swallowed up by fees and reiterated his point that investors could have achieved better returns on their own – with virtually no cost. Buffett will be donating his winnings to charity.One last bonus point: Berkshire’s annual meeting will once again be available via live webcast on Yahoo. To view the event, go to https://finance.yahoo.com/brklivestream at 9 a.m. Central Daylight Time (GMT-6) on Saturday, 6 May 2017.

If you’d like to read Buffett’s full 2016 annual letter to Berkshire shareholders (28 pages), you can click here.