In 2002, Hartalega Holdings Berhad (Bursa: 5168) invented and introduced the first soft nitrile gloves to the world. Since then, the industry has been revolutionized as global demand for nitrile gloves has outgrown demand for conventional latex gloves.

Today, Hartalega is the largest nitrile glove producer and among the top three largest rubber glove manufacturers in the world. As I write, Hartalega is worth RM11.7 billion in market capitalization. It is the only rubber glove stock to exceed the RM10 billion mark on Bursa Malaysia.

In this article, I’ll bring a detailed account of Hartalega’s impressive growth since its IPO in 2008 and its plans to sustain growth in the future. Therefore, here are the 14 things you need to know about Hartalega before you invest.

Track record

1. In 2008, Hartalega constructed Plant 4 on its site in Bestari Jaya, Selangor. At that time, Hartalega had three operating plants that had a combined production capacity of 2.9 billion gloves per annum. The construction of Plant 4 was completed in 2009 and boosted Hartalega’s production capacity to 6.2 billion gloves per annum. In 2011, Hartalega completed the construction of Plant 5 with ten production lines. Shortly after, Hartalega installed two additional production lines. As a result, Hartalega increased its production capacity from 6.2 billion gloves per annum to 10.0 billion gloves per annum. In 2014, Hartalega completed the construction of Plant 6 (with 10 production lines) at a cost of RM175 million. Consequently, Hartalega grew its production capacity from 10.0 billion gloves per annum in 2011 to 13.6 billion gloves per annum in 2014.

2. Hartalega has increased its efficiency in producing nitrile gloves by investing in higher efficient production lines which are able to produce more nitrile gloves in less time. For instance, the production lines installed in Plant 4 can produce up to 30,000 gloves per hour. The ones in Plant 5 and Plant 6 are better as they can produce 36,000 and 45,000 gloves per hour respectively. This enables Hartalega to benefit from economies of scale and lower its cost per glove.

3. In 2014, Hartalega started an eight-year master growth plan known as the Next-Generation Integrated Glove Manufacturing Complex (NGC). Costing RM2.2 billion, the NGC will house six plants comprising 72 production lines with each line producing up to 45,000 gloves per hour. This master plan is executed in three different phases. Each phase consists of the development of two plants each with 12 production lines capable of producing 4.7 billion gloves per annum per plant. As I write, Phase 1 and a portion of Phase 2 have been completed. To date, 36 production lines are running and Hartalega has boosted its production capacity from 13.6 billion gloves per annum in 2014 to 26 billion gloves presently.

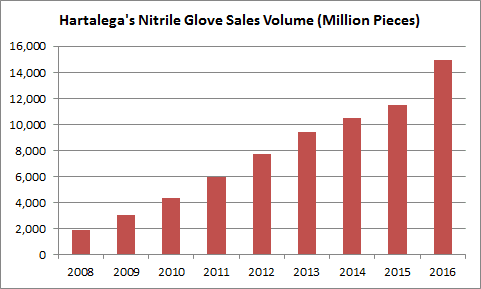

4. As a result, Hartalega has achieved a compound annual growth rate (CAGR) of 29.75% in nitrile glove sales from 1.86 billion pieces in 2008 to 14.94 billion pieces in 2016. This is due to substantial orders from key markets such as the United States and Europe over the eight-year period. Both these markets contributed approximately 80% of total revenues to Hartalega over the last five years.

Source: Hartalega annual reports

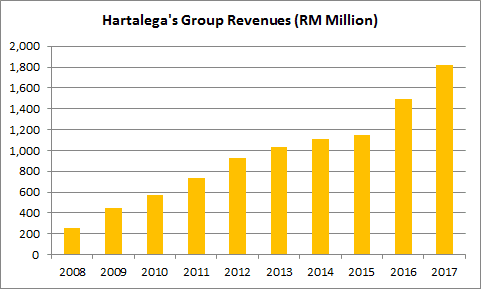

5. Hartalega achieved a CAGR of 24.28% in group revenues over the last nine years from RM257.82 million in 2008 to RM1.82 billion in 2017. This is contributed by continuous growth in sales and production capacity during the period.

Source: Hartalega annual reports & Q4 2017 report

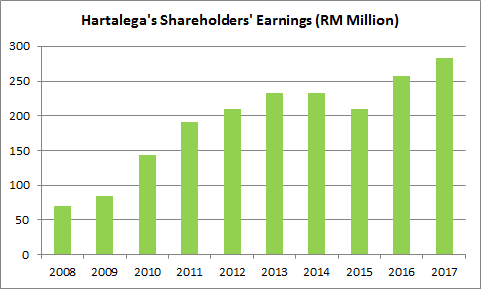

6. Hartalega achieved a CAGR of 16.88% in shareholders’ earnings over the last nine years from RM69.55 million in 2008 to RM283.04 million in 2017. The growth in earnings was slower as Hartalega has incurred higher cost of sales, administration and distribution expenses particularly from 2012 to 2017.

Source: Hartalega annual reports & Q4 2017 report

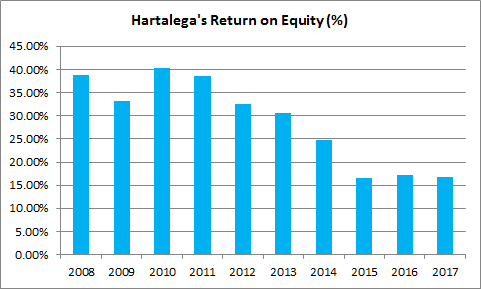

7. Hartalega achieved a CAGR of 28.23% in shareholders’ equity during the nine-year period from RM179.47 million in 2008 to RM1.68 billion in 2017. Evidently, Hartalega’s shareholders’ equity has outgrown its shareholders’ earnings during the period. This has caused return on equity to drop from 38.76% in 2008 to 16.83% in 2017 despite consistent growth in shareholders’ earnings.

Source: Hartalega annual reports & Q4 2017 report

8. From 2008 to 2017, Hartalega generated RM2.03 billion in cash flows from operations. It also raised RM449.07 million in net equities and long-term debt. Out of which, Hartalega has invested:

- RM342.02 million in property, plant & equipment

- RM1.45 billion in capital work-in-progress

- RM775.40 million in dividend payments

This means, Hartalega is a cash-producing business and doesn’t need to continually raise equity or debt to expand its business or reward its shareholders with dividends.

9. In 2012, Hartalega implemented a dividend policy to pay a minimum of 45% of annual net profits to its shareholders. Since then, Hartalega has increased its dividend payout ratio marginally from 45.3% in 2012 to 50.9% in 2016.

| 2012 | 2013 | 2014 | 2015 | 2016 | |

|---|---|---|---|---|---|

| Dividend per Share | 6.25 | 7.25 | 7.25 | 6.50 | 8.00 |

| Dividend Payout Ratio | 45.3% | 45.7% | 47.0% | 47.0% | 50.9% |

Source: Investors’ Presentation, 10th annual meeting of Hartalega

Figures for dividend per share (DPS) from 2012 to 2015 are adjusted to reflect the increase in number of shares from 801 million to 1.641 billion from a 1:1 bonus issue in September 2015.

10. Since January 2016, Hartalega has declared and paid RM0.02 in DPS per quarter. It is equivalent to RM0.08 in DPS per annum. As at 24 August 2017, Hartalega’s share price is RM6.89 a share. If Hartalega is able to maintain its DPS at RM0.08 over the next 12 months, its expected dividend yield is 1.16%.

Moving forward…

Hartalega will continue to derive income from its site at Bestari Jaya while pursuing sustainable growth from the NGC. Here are the major highlights of its future outlook.

11. At present, Hartalega has 45 production lines in Bestari Jaya which are capable of producing approximately 14.0 billion gloves per annum. The average output per line is 28,000 pieces per hour.

12. The NGC will boost Hartalega’s production capacity up to 42.4 billion gloves per annum upon completion in 2022. This is because the NGC will be equipped with 72 production lines which are capable of producing 28.0 billion gloves per annum. The average output per line at the NGC is 45,000 pieces per hour. Thus, it will also drive up Hartalega’s overall productivity as more production lines are introduced progressively.

Source: Investors’ Presentation, 7th annual meeting of Hartalega

13. Presently, Hartalega is embarking on Phase 2 of the NGC. A total of 36 production lines in Plant 3, Plant 4, Plant 5 and Plant 6 will be introduced on a progressive basis. Plant 3 is expected to contribute to Hartalega’s financial results in 2018. Meanwhile, Plant 5 and Plant 6 will begin commissioning in 2019-2020 under Phase 3 development of the NGC.

14. In addition, Hartalega has identified potential in China and India. On a per capita basis, China and India uses 5.3 and 4.0 pieces of gloves respectively compared to 166 pieces in the United States and 100 pieces in the European Union. Presently, two subsidiaries, Yancheng MUN Medical Equipment Co Ltd in China and MUN Health Product (India) Pvt Ltd in India have been established in 2012 and 2013 respectively to sell nitrile gloves in both countries. With ongoing healthcare reforms, China and India are expected to substantially increase their demand for rubber/nitrile gloves.

The fifth perspective

In conclusion, Hartalega has built a track record of delivering growth in sales and profits over the last nine years. As at 31 March 2017, Hartalega has RM120.26 million in cash reserves and a debt-to-equity ratio of 0.14. At present, Hartalega remains committed to maintain its growth momentum while placing efforts to ensure stable margins through cost optimization, economies of scale, and incremental productivity gains.

Hi Ian, thank you for the analysis. In your opinion, what would be the fair price to buy? The closing price last Friday is 6.85.

Hi Alice, thanks for your kind words. For a start, I don’t give a figure on the fair price of any stocks in my write-ups. This is because, different people would have different answers depending on their objective of stock investing. After all, what is fair to me may not necessarily be fair to you. But, I would leave you with two questions to help assess whether a stock deal is for you:

a. How much are you willing to invest to collect 8 sen in dividends per year?

b. If I have a business making RM 1 Million a year, what’s the max amount that you are willing to buy from me?

Regards

Ian

with those numbers, what’s ur estimate of their 30/9/2017 results which will be out soon? I mean the estimate of their net profit?

I can’t find analyst estimates for Malaysians counters