CapitaLand Mall Trust (CMT) is the largest retail REIT in Singapore. It owns/co-owns 16 retail malls in Singapore, many of which are familiar to locals including Plaza Singapura, Junction 8, Bugis Junction, Bugis+, Bedok Mall, and Tampines Mall. As at 31 December 2017, CMT’s property portfolio is valued at $8.7 billion.

Since it first listed in 2002, CMT has always been the ‘preeminent’ retail REIT in Singapore with its high-quality malls in great locations around Singapore. I attended the CMT’s annual meeting to evaluate its past year’s performance and its outlook ahead.

Here are eight things I learned from the 2018 CapitaLand Mall Trust AGM:

1. Gross revenue fell 1.5% year-on-year to $795.4 million and net property income (NPI) remained flat at $563.0 million. CEO Tony Tan cited a stable set of results despite the tough retail environment and the closure of Funan mall for redevelopment since June 2016.

2. Distributable income and distribution per unit (DPU) both remained flat at $395.8 million and 11.16 cents respectively. CMT pays out 100% of its distributable income to unitholders. If DPU remains stable, CMT’s expected distribution yield is 5.3% based on its last closing price of $2.12 as at 19 April 2018.

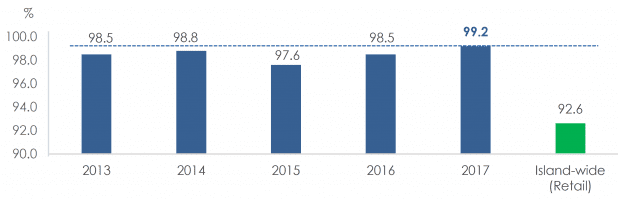

3. CMT’s portfolio occupancy rate is 99.2%, significantly higher than the 92.6% retail average in Singapore. However, annual shopper traffic fell 0.3% to 346.3 million and rental reversions were negative at 1.7%. Weighted average lease to expiry is 1.9 years, typical of the shorter leases seen in the retail sector. The CEO highlighted that Singapore has been (and still is) building a lot of new road and subway infrastructure. He anticipates that day-to-day commuter patterns will shift over time which may impact shopper traffic to CMT’s malls and is something that management is closely watching.

CapitaLand Mall Trust occupancy rate. Source: 2018 AGM presentation slides

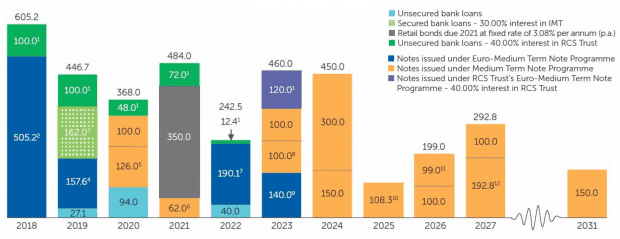

4. Gearing ratio is at 34.2%, which gives CMT a debt headroom of $1.1 billion before its hits 40% gearing. Average cost of debt is 3.2% and 95% of CMT’s borrowings are at fixed interest rates. CMT has a Moody’s credit rating of A2 which is the highest assigned to a Singapore REIT. Average debt maturity is 4.9 years (longest among Singapore REITS) and CMT aims to have around $500-600 million of debt expiring in any single year. From the chart below, CMT has a well-staggered debt maturity profile and the CEO added that the $505.2 million medium-term notes due in 2018 have already been repaid using internal sources and bank facilities.

CapitaLand Mall Trust debt maturity profile. Source: 2018 AGM presentation slides

5. With the growth of e-commerce and omni-channel retailing, CMT inked a deal with Alibaba and Lazada in 2017 to connect shoppers online and offline. CEO Tony Tan shared CMT will launch an exclusive online mall on Lazada.sg where shoppers have the option to collect their purchases at a CapitaLand mall. At the moment, there are seven of these ‘Click-and-Collect’ lounges located inside the malls.

6. To attract shoppers, CMT also runs a loyalty programme app called CapitaStar which currently has over 850,000 members. The loyalty programme helps CMT to track customer spending and understand which products and shops are popular with shoppers. CMT also launched StarPay, a new mobile payment service used in conjunction with the CapitaStar app, that will allow shoppers to make payments at participating retailers at CapitaLand malls. For now, StarPay is only available at Raffles City Shopping Centre and only allows users to add the American Express CapitaCard. But deputy chairman Lim Ming Yan said that StarPay will eventually allow users to add various methods of payment (e.g. credit cards, NETS, PayLah, etc.) in the near future.

7. The CEO gave an update on the redevelopment of Funan mall — construction is progressing very well and is expected to complete in the second half of 2019. American co-working office operator, WeWork, will lease 40,000 square feet of office space and 40% of Funan’s retail net lettable area (NLA) is already pre-committed. In 2017, CMT divested the serviced residence component of Funan to Ascott Ltd (a fully-owned subsidiary of CapitaLand). Ascott will develop and operate the serviced residences which will be named lyf Funan Singapore.

8. A unitholder questioned why the local retail environment was so tough when he noted from the annual report that Singapore’s shopping centre floor space per capita was only 5.8 square feet of NLA. In contrast, Hong Kong and the U.S. have figures of 10.1 and 23.6 respectively. The CEO explained that Hong Kong sees 60 million visitors annually, compared to 17 million for Singapore. Along with its larger population, Hong Kong is able to absorb the higher supply of retail space. The U.S., on the other hand, is over-malled as seen by the mass closing of malls there. Chairman Adj. Professor Richard R. Magnus added that a higher NLA per capita does not automatically translate to higher revenue; it is more important that CMT continue to adapt to consumer tastes and provide shoppers with a reason to always visit its malls.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

May I know how gearing ratio is calculated in this example, please? I tried using the balance sheet interest bearing loans plus convertible bonds (if available) to derive the debt figure, and divided the amount by the investment property valuation, but couldn’t arrive at 34.2%.

The exact figures that CMT uses are not shown, but the calculation is defined in its annual report as such:

“In accordance to Property Funds Appendix, CMT’s proportionate share of its joint ventures’ borrowings and total deposited property are included when computing the aggregate leverage. Funds raised ahead of the maturity of the existing borrowings of CMT are excluded from both borrowings and total deposited property for the purpose of computing the aggregate leverage as the funds are set aside solely for the purpose of repaying the existing borrowings of CMT.”