Incorporated in 1996 and listed on the Main Board of Bursa Malaysia in 2007, Aeon Credit Service (M) Berhad provides consumer financing through easy payment and hire purchase schemes for consumer durables and motor vehicles as well as personal financing and credit cards in Malaysia. The company currently has a network of more than 12,000 participating merchant outlets nationwide and more than 4.6 million card members for various products.

Aeon Credit is a subsidiary of Aeon Financial Service Co., Ltd., Japan, which is in turn part of the Aeon Group of companies, a global retail and financial services group that operates in Japan, Southeast Asia, China and India.

Aeon Credit has enjoyed steady growth in revenue and profit over the years. An investor who bought the stock at the IPO price of RM2.50 in 2007 would have made over a 500% gain by the end of 2018, excluding dividends, representing a compounded annual growth rate (CAGR) of 17.9%. I attended Aeon Credit’s AGM to find out more about the company.

Here are 11 things I learned from the Aeon Credit AGM:

1. Revenue grew 10.6% year-on-year to an all-time high of RM1.4 billion for the financial year ended 28 February 2019 (FY2019). This was attributed to increased contributions from the vehicle easy payment and personal financing segments.

2. Net profit grew 18.2% year-on-year to RM354.6 million in FY2019. Chairman Ng Eng Kiat attributed the growth to the higher financing receivables achieved across all segments, from personal financing (+26.8% YoY) to auto financing (+24.1% YoY).

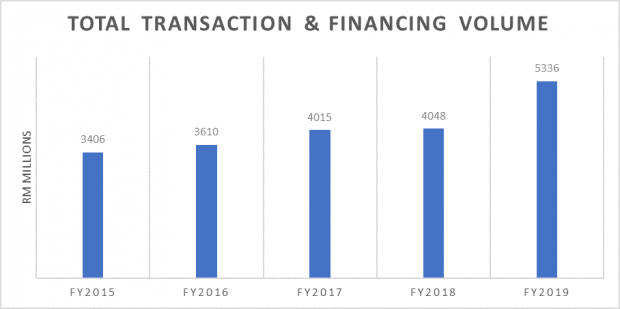

3. Total transaction and financing volume improved 31.8% year-on-year to RM5.4 billion in FY2019, mainly driven by personal financing (+56.0% YoY), motorcycle financing (+41.1% YoY) and credit card (+27.6% YoY). Ongoing marketing campaigns together with product innovation, promotion strategies, and quality customer service helped drive the growth.

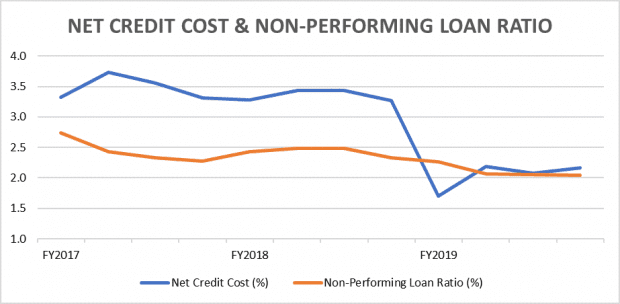

4. Receivables collection ratios remained stable in FY2019, which management attributed to better quality receivables and its strategic collection operation. Non-performing loan ratio in 4Q 2019 was lower at 2.04% (4Q 2018: 2.33%), thanks to improvement in delinquent receivables collection. Net credit cost was lower at 2.16% in 4Q 2019 (4Q 2018: 3.27%), supported by better quality receivables and higher bad debt recovery. CFO Lee Kit Seong revealed that AEON Credit enjoys financing with lower interest rates due to support from its Japanese parent company.

5. AEON Credit launched its e-money card AEON Member Plus Visa Card and e-wallet application AEON Wallet in November 2018 to provide AEON customers with cashless solutions (via QR code) at all AEON retail outlets. As of May 2019, its e-money card has registered over 700,000 cardholders, while its e-wallet app has over 200,000 downloads. Management targets to achieve 1.6 million cardholders and 1.0 million e-wallet users by FY2020. Lee said the move was in line with the direction set by Bank Negara Malaysia for Malaysia to go cashless. AEON Credit also plans to introduce its Corporate Card in FY2020 to capture more corporate customers by introducing its new credit settlement method.

6. Management said that as of end FY2019, AEON Credit’s customer income group ratio of B40:M40 was 70:30. The percentage of M40 customers increased in FY2019, and management targets to continue this expansion to 60:40 in FY2020, mainly to achieve better asset quality. Efforts to further penetrate this customer group include the introduction of its platinum card and risk-based pricing products, which were launched in FY2019.

7. Aeon Credit is transitioning from a business-to-business-to-consumer (B2B2C) model to a business-to-consumer-to-business (B2C2B) model in order to improve its customer touchpoints. The company is developing a new system and mobile application which could enable a more direct point of communication, as customers are able to check their financing limits before they purchase goods at Aeon’s merchants.

8. In January 2019, the Housing and Local Government Ministry granted Aeon Credit a money lending licence. Chief strategy officer Ajith Jayaram said that the approval would enable the company to market its products and services to a greater number of customers as well as expand its consumer financial products. A shareholder questioned the purpose of the licence as AEON Credit was already in the business of lending and voiced his concerned that having the licence would impose stricter requirements for future loans for its existing businesses. Ng assured that the licence would not have an impact on the company’s financials, while Lee added that Aeon Credit will also utilize the licence to expand the small and medium-sized enterprises (SME) financing business.

9. In December 2017, Aeon Credit was slapped with a RM96.8 million bill by the Inland Revenue Board for additional income taxes with penalties for alleged submission of incorrect returns for the years of assessment of 2010 to 2016. The company subsequently filed for an appeal. A shareholder asked about the progress of the issue and Ng replied that, after consultation with tax professionals, the management has reasonable grounds to believe that the company is not liable for the penalties, and have applied to the Court of Appeal to get a stay against the High Court’s decision in May 2019.

10. The Minority Shareholder Watch Group (MSWG) raised some questions about Aeon Credit’s credit card business. Management revealed its targets to maintain double-digit growth for credit cards in circulation annually. Lee explained that the credit card business complements the company’s existing business segments by offering a settlement option, and performance is currently within management’s expectations. The CFO further said that management will continue to expand the card business into the affluent T20 and M40 customer income groups, and SME segment with the newly launched platinum credit card. He revealed that Aeon Credit had issued 20,000 Platinum Cards since its launch in April 2018 and continues to see improvement in card issuance.

11. Looking forward, Aeon Credit will focus on strengthening customer loyalty and exploring new IT Infrastructure and fintech solutions. The introduction of new loyalty programs, benefits and, the e-wallet, and platinum card is expected to reach a wider group of consumers and improve customer engagement. In an answer to MSWG’s query, management revealed that part of the company’s investment budget of RM150 million for FY2018 to FY2020 are for investments in digital technology.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »