CDL Hospitality Trust (CDLHT) is a REIT that invests in hospitality-related assets such as hotels and resorts. It currently owns 19 properties with a total of 5,088 hotel rooms across eight countries, namely Singapore, Australia, New Zealand, Japan, United Kingdom, Germany, Italy and Maldives. Singapore remains CDLHT’s largest revenue contributor, accounting for 60% of net property income. As of 31December 2018, these properties were valued at S$2.8 billion.

Despite growth in incoming tourist numbers over the past few years, the Singapore hospitality sector has been weak due to an uptick in supply. This caused local hotel room rates to decline over the past four years. With supply growth expected to ease going forward, the hospitality sector is finally seeing signs of recovery. With this in mind, I attended CDLHT’s 2019 AGM for more insights on the local market, and the company’s prospects going forward.

Here are eight things I learned from the 2019 CDL Hospitality Trust AGM:

1. Net property income (NPI) dipped 3.8% from S$151.8 million in 2017 to S$146.1 million in 2018. While results look lackluster, CDLHT actually recorded a modest 1.5% growth in income from its Singapore properties, which account for nearly 60% of its overall portfolio. The drop resulted from the divestment of two Australian hotels and the closure of the Dhevanafushi Maldives luxury resort for renovation. These properties collectively contributed S$6.53 million to the REIT’s NPI in 2017. While the REIT also acquired an Italian hotel in 2018, it had a negligible impact on NPI as the acquisition was completed only in late November 2018.

2. Despite the fall in NPI, distribution per unit (DPU) rose 0.4% from 9.22 cents in 2017 to 9.26 cents in 2018. The marginal increase in DPU resulted from the partial distribution of gains from the two divestments mentioned earlier.

3. CDLHT acquired a 95% stake in Hotel Cerretani Florence, a four-star Italian hotel with 86 rooms for €40.6 million in 2018. In his prepared remarks, CEO Vincent Yeo outlined a number of features that made this acquisition compelling. Firstly, it is located in a prime area within Florence’s city centre. In fact, the hotel is less than 300 meters from the Florence Cathedral, a popular tourist attraction. In addition, future supply of hotel rooms in Florence is limited. The Florence city council has ceased granting licenses for new hotels to prevent overcrowding. Lastly, Florence itself draws in millions of tourists a month. Besides being famous for Renaissance art and architecture, it is also home to the ‘Pitti Immagine Uomo’, a biannual fashion exhibition which attracted 36,000 visitors during its most recent edition. However, the property is yielding just 4.3% at this price point, a figure substantially lower than CDLHT’s current portfolio yield of 5.6%. According to the CEO, the property is undergoing a ‘gestation period’, with financials expected to improve going forward.

4. CDLHT’s gearing increased from 32.6% in 2017 to 34.2% in 2018. This leaves the company with S$577.9 million in debt headroom before reaching the maximum possible gearing of 45%. Other metrics such as cost of debt and term to maturity continue to remain healthy, at 2.4% and 2.8 years respectively. However, the company’s fixed rate borrowings constitute only 62% of its portfolio, which is a figure that is lower than most other REITs. The CEO assured investors that this figure will increase after the bridging loan for the acquisition of Hotel Cerretani is refinanced.

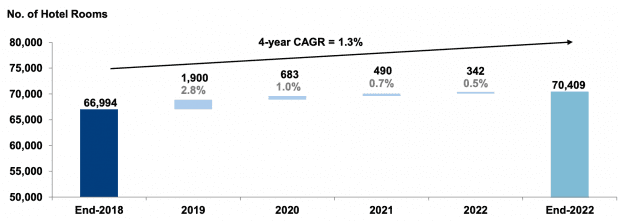

5. Management is optimistic on the Singapore hospitality sector. For one, they expect tourism numbers to continue rising. The government has recently announced a number of large-scale projects that will make Singapore an increasingly attractive tourist destination going forward. Besides an ambitious plan to develop the Jurong Lake District into a tourism hub by 2026, a recent agreement with the two integrated resort operators will see a total of S$9 billion invested in new attractions. To make things better, supply of hotel rooms is expected to grow at a CAGR of 1.3% over the next four years. This growth figure is very much subdued compared to the 5.5% supply growth between 2014 and 2017. In light of this, management expects revenues per available room (RevPAR) to recover barring an economic slowdown.

6. CDLHT’s large-scale asset enhancement initiatives (AEIs) are largely over for its Singapore hotels. CDLHT has completed a number of large AEIs for its Singapore hotels over the past few years. In 2016, the company revamped the lobby of Grand Copthorne Waterfront Hotel and refurbished a number of rooms at M Hotel. This was followed by the renovation of a restaurant and a number of rooms at the Orchard Hotel in 2018, which was followed by the refurbishment of the lobby and a number of public areas in the first half of 2019. Going forward, AEIs of Singapore hotels are expected to be smaller in scale. Current AEIs in the pipeline include refurbishment of some rooms at three of its hotels — Grand Copthorne, Studio M and Copthorne Kings. These refurbishments will be done in stages to minimise disruption to guests.

7. A shareholder asked if management had any development plans for CDLHT’s Angsana Velavaru resort in the Maldives given its lacklustre performance. Acknowledging that the resort had posted subpar performance, the CEO replied that renovation works expected to start within next few months. CDLHT will refurbish all 79 of the resort’s beachfront villas and improve a number of its public facilities. Management expects these enhancements to stem the decline in RevPAR.

8. After a string of overseas acquisitions, the same shareholder asked if the management is considering any Singapore acquisitions. While management team is mindful that CDLHT is a Singapore-centric REIT, Singapore hotels have not been appealing over the past few years. Firstly, CDLHT’s management team expected weakness in the Singapore market — something that has played out over the last four years. In addition, there were very few reasonably priced hotels up for sale. Going forward, CDLHT will continue looking for overseas acquisition targets should there continue to be a dearth of local opportunities. However, the CEO is confident that the company will purchase Singapore assets at some point in the future.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »