Keppel DC REIT (KDC REIT) is a pure-play data centre REIT listed on the Singapore Exchange. The REIT invests in a diversified portfolio of income-producing real estate assets which are used primarily for data centre purposes.

KDC REIT’s portfolio comprises 15 data centres — with a total attributable lettable area of 1.1 million square feet — strategically located in key data centre hubs in 10 cities across eight countries in Asia-Pacific and Europe. As at 31 December 2018, the portfolio was valued at approximately S$2.0 billion.

No matter how advanced civilization becomes, we can’t escape the need for physical real estate. The more we rely on technology to run our lives, the more data centres we need to store and compute our information.

In the Keppel DC REIT 2018 annual report, according to BroadGroup Consulting:

‘The cloud infrastructure market is estimated to have grown by over 40% globally in 2018 and is expected to continue expanding at a compound annual growth rate of more than 25% over the next five years.’

It’s clear that the cloud infrastructure market is growing rapidly. I attended the Keppel DC REIT AGM to find out about the dynamics of the industry and whether the REIT is positioned to take advantage of this growing digital transformation trend.

Here are 10 things I learned from the 2019 Keppel DC REIT AGM:

1. Gross revenue increased 26.2% year-on-year to S$175.5 million in 2018 and net property income grew 26.0% to S$157.7 million. This was primarily due to the acquisitions of KDC SGP 5 in Singapore and maincubes Data Centre in Germany, and full-year contributions from KDC DUB 1 in Ireland and KDC SGP 3 in Singapore.

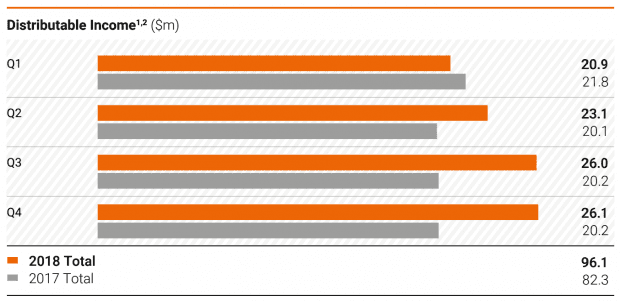

2. Distributable income increased 16.7% year-on-year to S$96.1 million while distribution per unit (DPU) increased 2.8% to 7.32 cents. Excluding the one-off capital distribution of 0.15 cents per unit in relation to Keppel DC SGP 3 recorded in 1Q 2017, DPU increased 5.0% from 6.97 cents in 2017 to 7.32 cents in 2018.

3. As at 31 December 2018, KDC REIT has a gearing ratio of 30.8%; 1.3 percentage points lower than the previous year. This was mainly due to the S$303.1 million raised via private placement in May 2018 to partially fund the acquisition of Keppel DC SGP 5. The REIT has an average cost of debt of 1.9% per annum and an interest rate coverage ratio of 11.4 times. Approximately 86% of the REIT’s borrowings have been substantially locked-in through floating-to-fixed interest rate swaps.

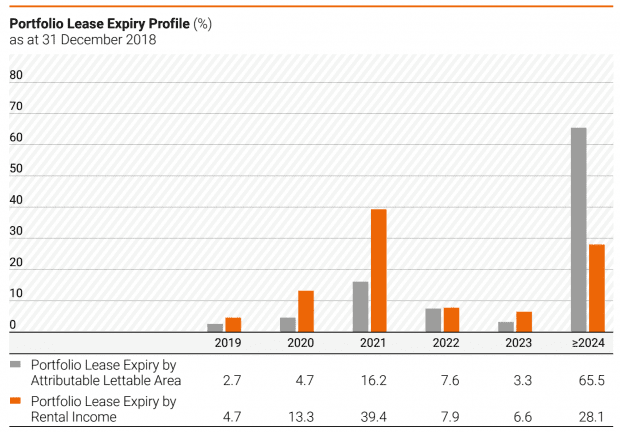

4. As of 31 December 2018, KDC REIT has a portfolio occupancy rate of 93.1%. Of the 15 assets in Keppel DC REIT’s portfolio, 10 of them are fully leased. The portfolio has an average weighted lease expiry of 8.3 years and less than 5% of leases (by attributable lettable area) are due for expiry in 2019 and 2020.

5. KDC REIT is expanding its Australian presence with the addition of Intellicentre 3 East Data Centre (IC3 East DC). The data centre, which is expected to be completed in 2020, will be built on vacant land within Intellicentre 2 Data Centre’s site. 6. A unitholder asked how data sovereignty laws would affect KDC REIT. CEO Chua Hsien Yang said that the regulation requires sensitive information such as the profile of citizens to be kept onshore. The rest can be kept offshore.

6. A unitholder asked why there are no Tier 4 data centres in Singapore and the difference from a Tier 3 data centre. The CEO explained that a Tier 4 data centre is hard to achieve because it requires a dual-power source – a second power grid – which Singapore doesn’t have. A Tier 3 data centre has N+1 redundancy, while a Tier 4 data centre has 2N+1 redundancy.

7. A unitholder asked why Basic Bay Data Centre in Malaysia had a low occupancy rate of 63.1%. The CEO said that the data centre was originally under a master lease agreement until the client decided to end the lease for one floor at the centre. As of now, leasing activity has slowed in Malaysia due to the change in government. However, the asset only makes up less than 2% of the REIT’s entire portfolio, so it wouldn’t have a large impact on results.

8. A unitholder asked if the management ever considered building instead of acquiring data centres. The CEO explained that REITs are usually formed to hold assets that already generate a stable and sustainable rental income. It’s rare for a REIT to develop new properties which comes with development risks, leasing risks, and early operation risks. A lot of testing has to be done before a data centre is operationally stable. Once a REIT takes on a developer role, its risk profile changes and returns will be affected in the short term. Instead, KDC REIT relies on its sponsor, Keppel Telecommunications & Transportation, which has an Alpha Data Centre Fund to first develop and stabilize a data centre before selling it to the REIT.

9. A unitholder wanted to know more about the competitive landscape of the industry. The CEO said that a lot of people can build a data centre but are not able to attract clients. A data centre houses mission critical infrastructure for many companies; if you don’t have a proven operational track record, not many companies will come to you. He added that there are data centres in Singapore that have 0% occupancy rates despite slashing their prices by 30%. So, the barrier to entry is very high. Although KDC REIT technically only listed four years ago, Keppel T&T has nearly 20 years of experience developing and operating data centres since the early 2000s.

10. A unitholder wanted to know KDC REIT’s top tenants and whether the REIT has a customer concentration risk. The CEO said that he is not allowed to disclose the information of their clients. They are institutions – corporations and governments – that want to keep their data operations a secret to avoid any potential physical or cyber-attacks. He added that many of their clients are large blue-chip companies that have a low risk of default and are, in fact, more afraid of the REIT defaulting! Therefore, they usually diversify their data storage among a few players in the industry.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »