Mapletree Commercial Trust (MCT) owns a mix of retail and commercial properties in Singapore. As of 31 March 2019, MCT’s portfolio of five properties – VivoCity, Mapletree Business City I, PSA Building, Mapletree Anson, and Bank of America Merrill Lynch HarbourFront – is valued at S$7.0 billion.

MCT has been one of the better-performing REITs in Singapore since its IPO in 2011. I decided to attend its latest annual general meeting and get an update on the REIT’s latest performance and developments.

Here are 12 things I learned from the 2019 Mapletree Commercial Trust AGM:

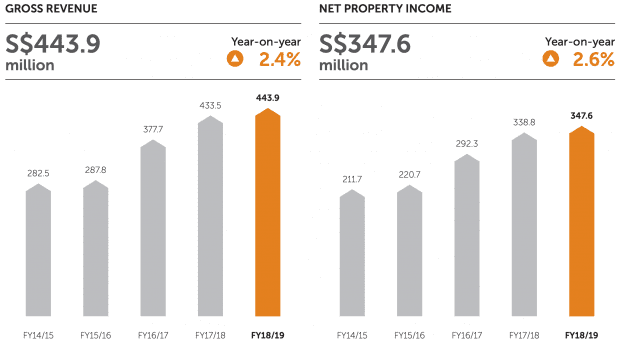

1. Gross revenue grew 2.4% year-on-year to S$443.9 million and net property income grew 2.6% y-o-y to S$347.6 million. This was driven by higher rental income across the portfolio except for Mapletree Anson due to a decline in occupancy rate recorded there.

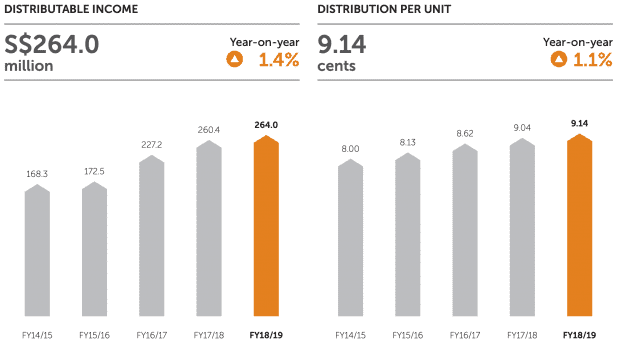

2. Distributable income rose 1.4% y-o-y to S$264.0 million while distribution per unit (DPU) rose 1.1% to 9.14 cents. The lagging DPU performance was attributed to the issuance of 9.5 million new units at a price range between $1.5519 and $1.6840 for manager compensation.

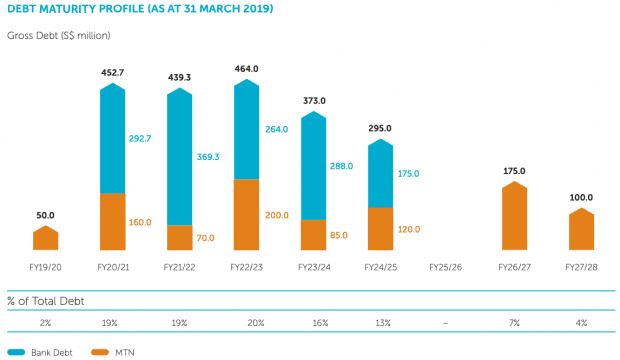

3. Gearing ratio decreased from 34.5% in 2018 to 33.1% in 2019 based on the upward revaluation of MCT’s properties. Average cost of debt increased slightly to 2.97% due to a higher floating rate and a higher proportion of fixed interest loans at 85%. Overall debt to maturity is at 3.6 years with no more than 20% of debt due for refinancing in the next few years.

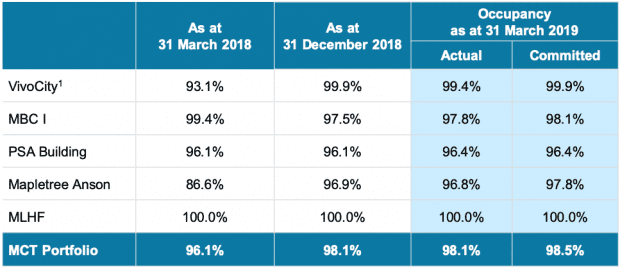

4. Occupancy rate across the portfolio went up from 93.1% in 2018 to 98.5% in 2019. VivoCity’s occupancy rate increased due to the completion of an asset enhancement initiative (AEI) which added a public library on Level 3 and 10 new lifestyle/athleisure brands on Basement 1. The expansion increased the mall’s net lettable area by 24,000 square feet. Mapletree Anson’s occupancy rate increased from 86.6% last year to 97.8% due a changeover in tenants.

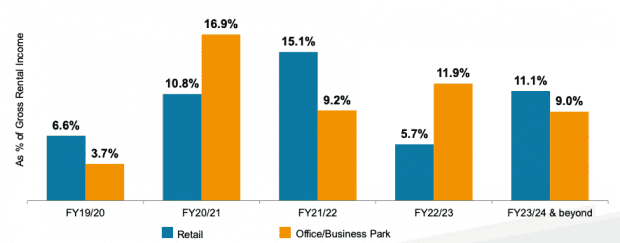

5. Weighted average lease expiry is 2.9 years. The largest portion of leases — 27.7% of the portfolio — will be expiring in 2020. MCT’s top 10 tenants make up 25.5% of gross rental income.

6. A unitholder highlighted that the base fee paid to the management has been increasing as the REIT’s properties appreciate in value. He wondered if the management would pay unitholders back if the value of the properties were to depreciate during a recession. Chairman Tsang Yam Pui disagreed with the concept of the management ‘paying back’ when the value of properties decline. The management’s base fee moves in tandem with the value of properties and will lower accordingly when the value comes down.

7. Tagging on the question of compensation, another unitholder asked if it was necessary for MCT to have so many directors on the board and if it were better to ‘right-size’ the number of directors to minimize cost. The chairman replied that it was intended for the board to have a high number of independent directors (seven out of 12 directors are independent) to protect the best interests of unitholders.

8. A unitholder wanted to know if there was more room for MCT to do a major AEI like adding an extra floor to an existing property, or if it has reached a ‘saturation point’. CEO Sharon Lim said that it’s a continuous exercise to look for ways to increase the use of a property. Adding a new floor would mean an increase in gross floor area (GFA) which is regulated by the Urban Redevelopment Authority (URA). MCT was able to increase the GFA of VivoCity due to the bonus GFA granted by the URA due to the addition of the public library. But it is unlikely that the management would add a whole extra floor to VivoCity as it is already capped by the limits of its GFA. On the other hand, the management has increased the net lettable area within the mall since 2015 to improve the yield of the property.

9. A unitholder suggested that the management should take advantage of MCT’s high unit price now to raise funds while waiting for the right opportunity to come along. The CEO explained that raising funds without an acquisition on hand is very dilutive and MCT is unlikely to do so.

10. Another unitholder added the last time MCT did a preferential offering was three years ago to acquire Mapletree Business City I. He asked if the management would consider taking advantage of the premium valuation of MCT’s unit price to acquire Mapletree Business City II? The chairman said that MCT has the right of first refusal to the property, but it is the sponsor’s decision to choose whether it wants to divest the asset. The CEO – who’s in favor of acquiring MBC II – added that factors need to be aligned for the deal to be made. These include a motivated seller, whether the property is a good fit for the portfolio, and a supportive capital market to raise funds for a potential acquisition.

11. A unitholder asked why there was a difference in cap rates between offices and business parks. The CEO explained that MBC I is made up of three buildings: Block 10, Block 20, and Block 30. Block 10 consists purely of offices which can be leased to any tenant. Blocks 20 and 30 are business parks that are mostly reserved for non-client-facing tech companies. Due to the constraints in the types of tenants that can come in, the independent valuers ascribed a higher cap rate for the business parks. Generally, there are no differences between the buildings, only the underlying titles and usage of them.

12. Lastly, a unitholder enquired whether MCT would consider offering a scrip dividend scheme. The CEO said that MCT had done it before but eventually decided to suspend the program due to the low take-up rate. The high administrative costs also do not justify it.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »