Mapletree Logistics Trust (MLT) is Singapore’s first Asia Pacific-focused logistics real estate investment trust with a portfolio of 141 properties in Singapore, Hong Kong, Japan, China, Australia, South Korea, Malaysia and Vietnam. As of 31 March 2019, MLT’s portfolio was valued at S$8.0 billion.

To me, warehouses used to be a regular commodity. However, the rise of e-commerce has given certain logistic properties a competitive advantage over others – especially those in prime locations near logistic hubs that can expedite same-day delivery to customers.

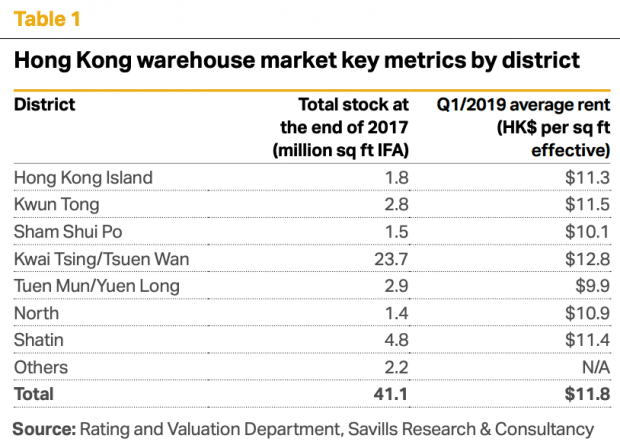

Over the past two decades, Hong Kong has seen a migration of warehouses towards the northwest New Territories, from Hong Kong Island and Kwun Tong to the Kwai Tsing/Tsuen Wan district which are close to cargo terminals and the Hong Kong International Airport. This is a concentration of smart modern warehouses, built to enable automation, to increase the efficiency of the supply chain.

Logistics properties of this type can also be found in Singapore and Japan where land is scarce and has limited redevelopment opportunities.

Due to the growing e-commerce industry, a high demand and low supply for modern warehouses means tenants are easy to find or replace. And when driven by strong domestic consumption, rental income from these e-commerce players tend to be more resilient in an economic downturn. As it is, MLT stands to benefit from the e-commerce wave as its portfolio of prime logistics properties provides a stream of stable and predictable income for the REIT.

Here are 10 things I learned from the 2019 Mapletree Logistics Trust AGM:

1. Gross revenue grew 15.0% year-on-year to S$454.3 million and net property income grew 16.7% y-o-y to S$389.5 million. This was driven by higher rentals from the portfolio of properties; the acquisition of eight logistics properties in Singapore, Australia, South Korea and Vietnam for S$964.4 million, and a 50% interest in 11 Grade A logistic properties in China for S$575.3 million; the redevelopment of Mapletree Pioneer Logistics Hub in Singapore and Mapletree Ouluo Logistics Park Phase 1 in China; and full-year revenue contribution from Mapletree Logistics Hub Tsing Yi and the remaining 38% interest in Shatin No. 3 in China which were acquired last year.

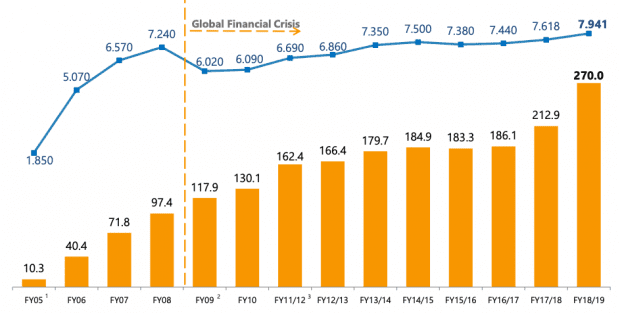

2. Distributable income increased 26.8% y-o-y to S$270.0 million while distribution per unit (DPU) rose 4.2% y-o-y to 7.941 cents. The amount includes a divestment gain of S$11.1 million from the divestment of 531 Bukit Batok Street 23, 7 Tai Seng Drive, 4 Toh Tuck Link, Zama Centre, and Shiroishi Centre. DPU growth was much slower due to the issuance of 564.2 million shares, mostly through two private placements, to fund new acquisitions.

3. Gearing ratio remain unchanged at 37.7%. Average debt to maturity is 4.1 years and 84.0% of debt is at fixed interest rates.

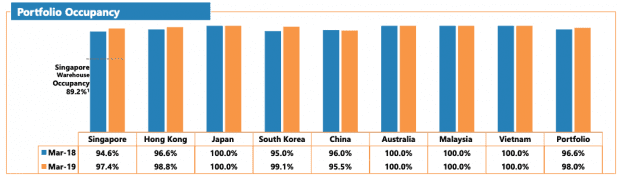

4. Portfolio occupancy rate went up from 96.6% in 2018 to 98.0% in 2019. Domestic consumption is driving the demand of logistics properties. Most of the new tenants are e-commerce related businesses: retailers, third-party logistics providers, and parcel delivery companies.

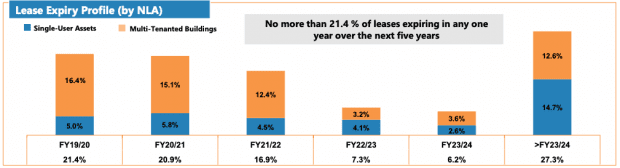

5. Weighted average lease expiry (WALE) is 3.8 years. MLT’s top ten tenants made up 29.3% of total gross revenue. No more than 21.4% of the leases expire in any year over the next five years.

6. Weighted average land lease is 43.8 years, while 22.7% of the land lease will expire in 31 to 40 years, with the bulk of it coming from Singapore.

7. A unitholder asked how the U.S.-China trade war is affecting MLT’s business in China. CEO Ng Kiat said that tenants have become more cautious and realistic in their expansion plans. This is an advantage for MLT to attract businesses with longer-term strategies. Warehouses will continue to benefit from the urbanisation of China which continues to grow, albeit at slower pace. As a result of the trade war, a lot of Chinese companies like Alibaba are also exploring alternative logistics centers in Southeast Asia; there’s an increase in take-up for properties in Vietnam and Malaysia. Because of this, MLT has been able rent out double the space in the same amount of time – including two million square feet of warehouse space in Malaysia within a year.

8. A unitholder wanted to know why JD.com cancelled its lease with MLT and if there were any issues with the warehouse properties. The CEO responded saying that there are no issues with regards to the properties. E-commerce players in China have a tendency to over-expand and utilise short-term strategies to test the marketplace. After JD.com returned half of the total warehouse space, MLT has been able build it up to 65% occupancy and is in negotiations with other tenants which would bring it up to 85% occupancy. For prime warehouse locations like this, MLT is normally able find replacements in less than twelve months.

9. A unitholder inquired why joint ventures in China were taking a loan of S$174 million from MLT. CFO Ivan Lim said that the loans — which are denominated in renminbi — create a natural hedge for MLT. He added that the offshore renminbi currency, CNH, moves closely with the onshore currency, CNY, so it wouldn’t impact net asset values. MLT also charges an interest on the loan to joint ventures.

10. A unitholder wanted to know more about the nature of MLT’s business in Japan. The CEO said that most of MLT’s properties are located in the Greater Tokyo Ring Road area which are within proximity to customers. There is no more land in this area for redevelopment. Japanese are cooking less as they age and looking to these warehouses to supply fresh, chilled, and cooked food. MLT is also converting these warehouses to do last mile deliveries — the final stop before goods reach convenience stores and supermarkets. MLT’s Japanese portfolio is very stable and occupancy rates are always close to 100%. Tenants tend to be very sticky once they have settled in with their workforce in place. Their tenants are also starting to be open to positive rental reversions every three years, whereas they used to remain flat at the end of every five-year lease.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

Hi,

WHat is your take on the long term prospect since it has several properties in HK?

Hi Chris,

In the long run, MLT will continue to benefit from the growth of e-commerce. Physical assets are required to move goods from the manufacturers to the consumers. And the demand for well-located warehouses, especially in Hong Kong, still outstrips supply so I still remain optimistic on the outlook of this REIT.

MLT’s properties in Hong Kong are protected by leases in the short run. If the situation in Hong Kong persists, they might experience volatility in their rental income. It’s not something I’m worried about. E-commerce players are quite resilient and the probability of that happening is quite low.