Banks have always been a favourite among retail investors in Singapore. But with an uncertain global trade outlook and interest rate environment, bank stocks have been trading sideways since the beginning of the year. Hence, I decided to go OCBC Bank’s annual general meeting to gain some insights.

Here are seven things I learned from the 2019 OCBC Bank AGM:

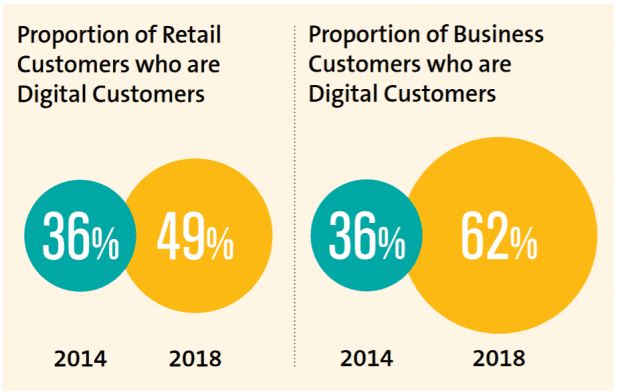

1. The purpose of digital transformation is to improve the bank’s customer experience by providing better, faster, and cheaper services. The proportion of retail customers who transact through digital channels has increased over the last five years, from 36% in 2014 to 49% in 2018. Likewise, for business customers, the proportion has increased from 36% to 62% over the same period. Digital retail customers generate two times more revenue than non-digital customers. OCBC defines digital customers as those who have used Internet/mobile banking at least once in the last three months, while other banks define it based on one year.

Source: OCBC 2018 annual report

2. OCBC’s non-performing loan (NPL) ratio is at 1.5%. Group CEO Samuel Tsien explained to shareholders that 60% of NPL are related to the oil and gas sector. The bank classifies a loan as non-performing when the customer requests for a rescheduling or restructuring of the loan. In other words, OCBC doesn’t define an NPL according to when a customer fails to service the loan, which is a more conservative approach. The CEO add that about 45% of NPLs are still ‘performing’ because they are not yet overdue, and he is not overly concerned with the ratio.

3. A shareholder asked about the share buybacks that OCBC executed in recent years. The management explained that share buybacks are solely for the company’s employee share option scheme. The CEO also emphasized that OCBC does not use share buyback as a tool to influence its share price.

4. A good way to monitor the performance of OCBC’s wealth management business is to track its assets under management (AUM). This business comprises OCBC’s premier and private banking, and the Bank of Singapore. A higher AUM equals higher management fees; AUM grew by 6.4% to S$200.38 billion in 2018 and gross wealth management fees grew 4.8% to S$958 million.

Source: OCBC 2018 annual report

5. OCBC subsidiary, Wing Hang Bank, performed well in 2018 with profits up 15%. Wing Hang mainly focuses on its domestic markets in Hong Kong and China. OCBC acquired the bank in 2014 and subsequently introduced additional products and services to Wing Hang’s client base. My take from the management is that they are optimistic that Wing Hang will continue to perform well.

6. A shareholder asked the management about its dividend policy and whether the dividend would be increased. The management said that they have to consider the long-term sustainability of the dividend before deciding to raise it. They also need to balance between paying a dividend and capital retention so that they’re able to capitalise on opportunities when they arise.

7. DBS and UOB outsources its insurance business to third-party insurance companies, while OCBC owns its insurance business through Great Eastern. The management explained that insurance forms part of the bank’s wealth offerings and the bank is able to make use of data analytics to anticipate the insurance needs of their customers which third-party providers are unable to provide. As a result of this synergy between OCBC and Great Eastern, the bank’s penetration in the bancassurance market has been very good compared to its competitors.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »