United Overseas Bank (UOB) is a leading bank in Asia with a global network of more than 500 branches and offices in 19 countries and territories in Asia Pacific, Europe and North America. The bank provides a wide range of financial services globally through three core business segments: group retail, group wholesale banking and global markets.

Here are seven things I learned from the 2019 UOB Bank AGM:

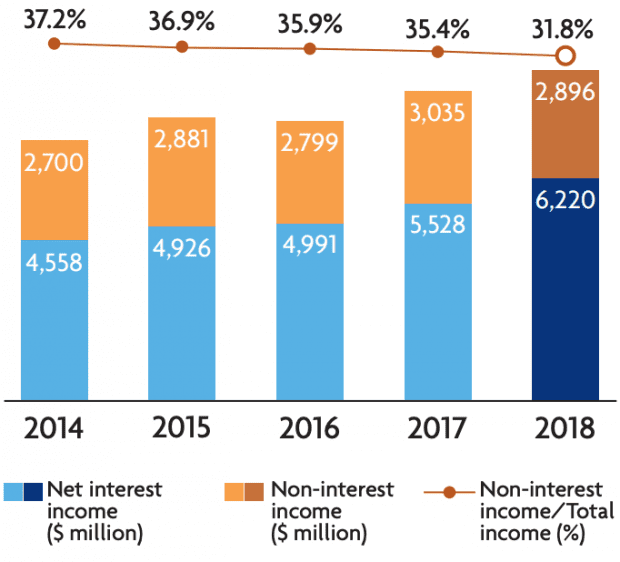

1. UOB’s total income rose 6% year-on-year to S$9.12 billion in 2018. The growth was driven by a 13% increase in net interest income — in line with the rising interest rate environment — and a 5% increase in net fee and commission income, driven by the strong performance in loan-related, credit card, trade-related and fund management fees.

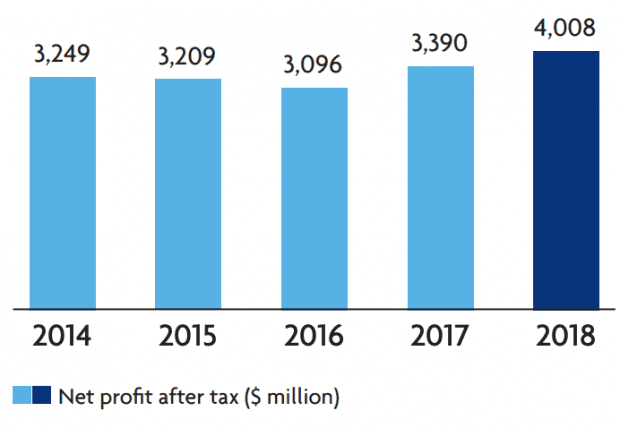

2. Net profit after tax increased 18% year-on-year to $4.01billion. Cost-to-income ratio rose marginally to 43.9% as UOB continues to invest in talent and technology to improve digitalisation, product capabilities, and customer experience. As a result, total expenses increased 7% to $4.00 billion.

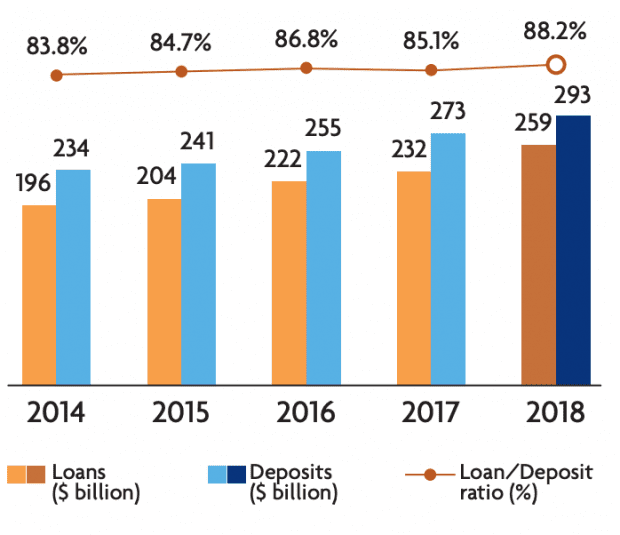

3. Loans-to-deposit ratio increased 3.1 percentage points to 88.2% in 2018. This was contributed by the 11% increase in gross loans to S$259 billion, which outpaced the 7% growth in deposits to S$293 billion.

4. Non-performing loan ratio improved from 1.8% in 2017 to 1.6% in 2018. Coverage for non-performing assets remained stable at 87%, or 202% after taking collateral into account. A shareholder wanted to know if UOB had any loan exposure to Hyflux to which CEO Wee Ee Cheong replied, ‘we hardly have any exposure to Hyflux.’

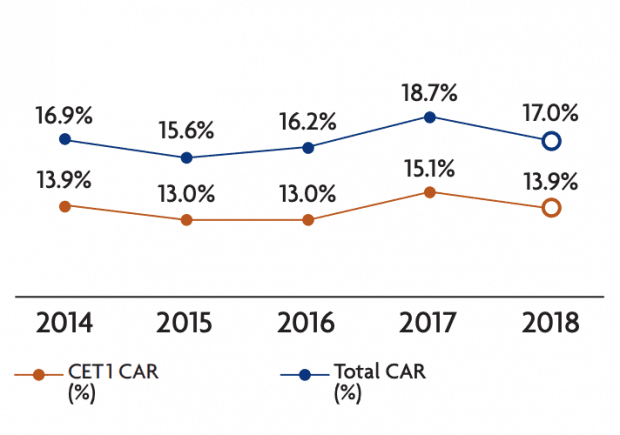

5. As at 31 December 2018, UOB has a Common Equity Tier 1 CAR of 13.9%. Its leverage ratio of 7.6% is more than double the regulatory minimum requirement. The bank looks well-capitalized to navigate macro-uncertainties ahead, protecting depositors and shareholders against unexpected losses. UOB has an ‘Aa1’ credit rating from Moody’s and a ‘AA-’ credit rating from both Fitch and Standard and Poor’s.

6. A shareholder highlighted that UOB remains an Asia-centric bank and asked if the management ever considered expanding to the West. The CEO said that he admired the shareholder’s aspirations and would like UOB to be global bank as well. However, size is not everything and there are also many big banks out there that have failed. Instead, UOB needs to focus on what its good at. The bank has been in Malaysia for over 60 years and has a 5% market share. It’s been in Thailand for 16 years, competing with eight incumbents, and has a 3% market share. He believes that there is still so much more room for UOB to grow in Asia

7. A shareholder, representing a group of investors, was concerned about sustainability, wanted to know if it was appropriate for UOB to continue financing coal power infrastructure given the air pollution and risk of climate change. Chairman Wong Kan Seng stated that UOB takes responsible financing seriously before passing the question on to one of the managers on the floor. The manager shared that as of January 2018, UOB hasn’t financed any new coal-fired powerplants and is pivoting its focus towards financing renewable energy projects including solar, geothermal, and mini-hydroelectric generation facilities.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »