CapitaLand Mall Trust (CMT) is the first REIT to be listed on the SGX in July 2002. It is also the largest retail REIT by market capitalisation in Singapore (as at 31 December 2019). All of CMT’s 15 shopping malls are located in the suburban areas and downtown core of Singapore. CMT also owns a 11% interest in CapitaLand Retail China Trust, a pure play Chinese retail REIT.

Due to movement restrictions imposed in light of COVID-19, retail malls in Singapore have been hit hard by the reduction in shopper traffic. As an almost pure play Singapore retail REIT, I wanted to find out how COVID-19 has affected CMT’s business and how CMT plans to meet the challenges posed by the pandemic.

Hence, I tuned in to CMT’s 2020 virtual AGM and here are seven things I learned at its 2020 AGM:

1. CMT’s distributable income and distribution per unit (DPU) increased by 7.5% and 4.1% y-o-y to S$441.5 million and 11.97 cents respectively in FY2019. The increase in distributable income was mainly due to the new contribution of Funan (which reopened on 28 June 2019) and the 100% contribution of Westgate (after CMT acquired the balance 70.00% interest on 1 November 2018). However, CMT’s DPU increased by only 4.1% due to CMT’s enlarged unit base.

2. CMT’s annual shopper traffic increased by 1.4% y-o-y, but tenant sales per square foot decreased by 1.4%. The increase in annual shopper traffic was driven mainly by CMT’s suburban malls. The decrease in tenant sales per square foot was due to the underperformance of some tenant sectors like home furnishing and electronics.

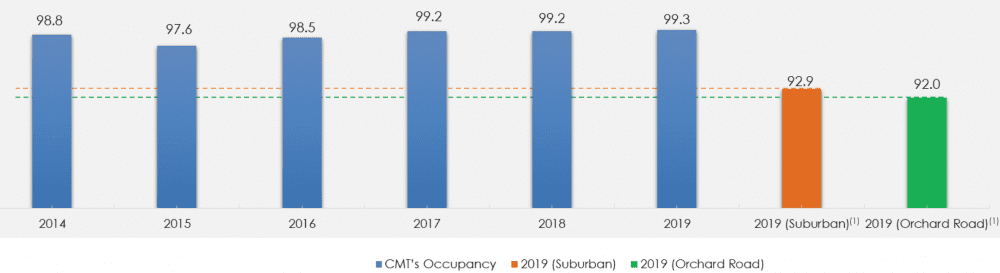

CMT’s overall occupancy rate has consistently remained higher than the islandwide occupancy rate in both the Orchard Road and suburban areas throughout the years.

Source: CapitaLand Mall Trust 2020 AGM presentation slides

However, CMT’s rental reversion remained rather subdued with only a 0.8% increase in FY2019.

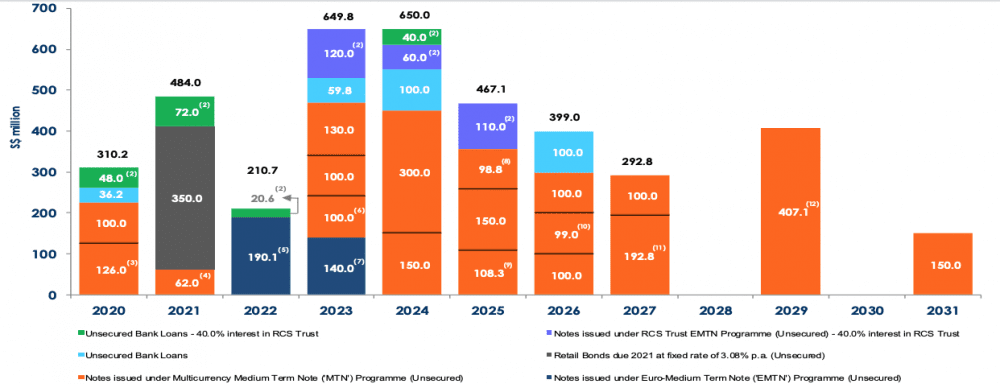

3. CMT has a gearing ratio of 33.3% which is well below the regulatory limit of 50%. However, CMT’s interest coverage ratio stands at an uneasy 4.6. As a rule of thumb, I personally prefer REITs with an interest coverage ratio of at least 5.0 (although the MAS minimum is 2.5). CMT’s debt maturity profile is well spread out with no more than 17% of its debt, as of 31 March 2020, expiring in a single financial year.

Source: CMT’s 2020 AGM presentation slides

4. Funan’s reopening and Lot One’s ongoing asset enhancement initiative (AEI) reflect the proactive upgrading of CMT’s properties. Funan, previously an IT-focused mall, reopened in mid-2019 as an integrated development comprising retail, office, and co-living components after three years of redevelopment. After the redevelopment, Funan’s net lettable area increased by 78%. Consequently, the market valuation for Funan increased by 111%. As at 31 March 2020, Funan’s overall occupancy rate was 99.3%.

Lot One’s cinema will be upgraded, and its four big halls will be reformatted into eight smaller halls on Levels 5 and 6. Lot One’s library will also be expanded to deepen community engagement. Lot One’s AEI will be progressively completed from 2H 2020, subject to the easing of restrictions on the resources required for the AEI.

5. CMT’s outlook remains highly uncertain as the COVID-19 situation remains fluid. Retail headwinds are expected in FY2020 as demand for retail space softens, but they would be mitigated by limited new retail supply in the next five years CMT’s operations. As Singapore enters Phase Two of re-opening, a large majority of tenants have resumed operations. However, shopper traffic and tenant sales are expected to remain muted amidst economic uncertainty, low tourist numbers, and the safe distancing measures in place. This means that CMT’s rental reversion and occupancy will remain subdued due to cautious retailer sentiment.

6. The CEO shared CMT’s near-term strategy to manage its cash flow and support its tenants deal with the adverse business impact due to COVID-19. In April and May 2020, 100% rental rebates were granted for almost all retail tenants, inclusive of the value of property tax rebates. Turnover rent was also waived. Additional rental relief was also provided in June to qualifying SME tenants in accordance with the COVID-19 Bill.

To manage operating expenses to conserve cash, CMT will be deferring AEIs and development works except for ongoing works at Lot One. CMT also has bank facilities to finance CMT’s operations for FY2020-21. REITs are also afforded greater flexibility to manage loan and cash flow obligations. For example, there will be no automatic enforcement by banks on landlords with loan covenant breaches due to the temporary constraints imposed by the COVID-19 Bill. The distribution payout timeline will also be extended to 31 December 2021 for distributable income earned in FY2020.

7. To strengthen stakeholder engagement post-circuit breaker, CMT launched new digital platforms to drive sales. CMT launched two new offline-to-online platforms on 1 June to drive sales during the Phase One re-opening and beyond:

- eCapitaMall is an ecommerce platform that allows shoppers to browse merchandise online and purchase items offline and vice versa.

- Capita3Eats is Singapore’s first mall-operated food ordering platform offers three ways to fulfill food orders – delivery, takeaway or dine-in.

These two initiatives help enable retailers to reach more consumers and increase online business opportunities.

The fifth perspective

CMT’s share price has recovered about 32% from its April low to $2.01 as at 21 July 2020. Based on this and its FY2019 DPU of 11.97 cents, CMT’s dividend yield is at 6.0%. However, do note that CMT is likely to face downward pressure on rents this year which would impact distributions; CMT’s Q1 2020 dropped 70.5% y-o-y to 0.85 cents.

Expect the retail sector to remain uncertain in the near term for CMT and retail REITs in general. But over the long term, high-quality REITs like CMT are likely to emerge from the pandemic and do fine in a post-COVID world.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »