CapitaLand Retail China Trust (CRCT) is a pure-play retail REIT with its properties located entirely in China spread over nine cities. It derives about 95% of its net property income (NPI) from its properties located in Tier 1 and 2 Chinese cities.

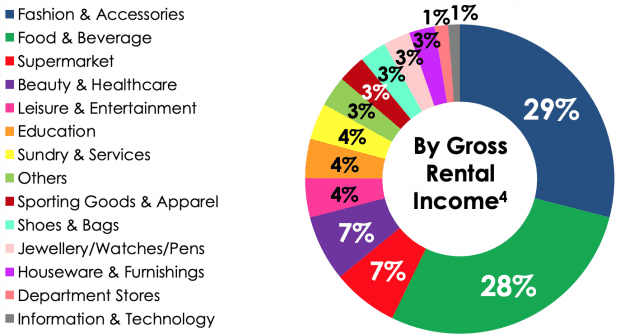

CRCT also has a well-diversified tenant base across more than 14 trade sectors (figures correct as of 31 March 2020):

Source: CapitaLand Retail China Trust 2020 AGM presentation slides

CRCT’s shareholders are naturally concerned about the REIT’s outlook given that the COVID-19 pandemic originated in Wuhan, China before spreading throughout the country. This sent the entire country into lockdown and ghost towns emerged.

However, as restrictions are being gradually lifted in China, I was interested to see if CRCT has recovered as well and how they are dealing with the slowdown in retail traffic. Having attended the AGM, I am personally quite bullish about CRCT’s medium-term prospects and believe they are well-placed to tide through this crisis.

So here are five things I learned from CRCT’s 2020 AGM:

1. CRCT’s gross revenue and NPI increased by 10.1% y-o-y to RMB1.2 billion and 15.5% y-o-y to RMB835.0 million respectively in FY2019. The increase was mainly due to stronger property performance and strong rental growth of the core multi-tenanted malls and new contributions from CapitaMall Xuefu, CapitaMall Yuhuating and CapitaMall Aidemengdun, which were acquired on 30 August 2019.

2. CRCT’s finances are quite prudently managed. CRCT’s gearing ratio stands at a healthy 36.7%. Though relatively high compared to other SGX-listed retail REITs, this is well-below the regulatory gearing ratio limit of 50%. This gives CRCT sufficient debt headroom (S$1.2 billion) to acquire properties and conduct asset enhancement initiatives to grow the REIT.

In line with its hedging policy, CRCT hedges about 80% of its total debt on fixed rates. This ensures CRCT’s debt amount does not balloon in case interest rates rise. However, as we foresee a low interest rate environment over the next few years due to COVID-19, I’m not sure if CRCT has ‘over-hedged’ its debt .

CRCT also has a well-distributed debt maturity profile with about 12-21% of its debt maturing each financial year from 2020 to 2025. Taking advantage of low interest rates, CRCT refinanced S$150 million (or 64%) of its loans maturing in 2020 that will now be due in 2026.

3. CRCT can potentially benefit from the stimulus packages rolled out by the Chinese government. In China’s annual political event ‘Two Sessions’ in May 2020, Chinese premier Li Keqiang announced a fiscal stimulus package of around RMB3.6 trillion (US$506 billion) to lead China’s economy recovery following the COVID-19 pandemic. Tax cut are also expected to lower business tax burden by 2.5 trillion yuan. The pro-business, pro-consumption stimulus together with the issuance of digital coupons to encourage consumption would probably see the improvement of CRCT’s retail performance.

4. CRCT’s malls are gradually recovering following the easing of COVID-19 restriction measures in China. CRCT CEO Tan Tze Wooi mentioned that all of CRCT’s malls have reopened from 2 April 2020 and that its malls have reverted to normal operating hours, barring regulatory requirements.

Ninety-four percent of CRCT’s stores have resumed operations — the remaining 6% of stores that belong to the education, entertainment and leisure sectors remained closed as mandated by the government.

As seen from the charts below, CRCT malls’ shopper traffic and tenant sales have gradually picked up since travel restrictions have eased in China in February. As at May 2020, shopper traffic and tenant sales at CRCT’s malls have yet to return to pre-pandemic levels.

Source: CapitaLand Retail China Trust 2020 AGM presentation slides

5. CRCT is leveraging on digital capabilities to attract more retailers to its platform. CapitaStar is CRCT’s e-commerce platform with more than 1,100 Chinese retailers onboard the platform, with another 3,000 retailers in the pipeline. Digital platforms would allow the collection and analysis of consumer data through data analytics, allowing CapitaStar to provide more targeted suggestions to its consumers. Through CapitaStar, CRCT can also ride on the secular trend towards e-commerce in China, which has accelerated due to the COVID-19 pandemic.

The fifth perspective

From its pre-pandemic high of S$1.69, CRCT’s share price has partly recovered to S$1.28 (as at 12 July 2020). Based on its share price, its dividend yield currently stands at 7.73%. While the yield is attractive, investors must keep abreast with the COVID-19 situation in China and its impact on the retail sector there.

As long as CRCT is able to keep its malls open and see a gradual improvement in shopper traffic to pre-pandemic levels, CRCT’s NPI and DPU is likely to remain sustainable in the near term.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »