Singapore Press Holdings (SPH) is a media organisation with operations in print, digital, radio and outdoor media. It also has businesses in property, purpose-built student accommodation, and aged care.

SPH has seen a steady fall in its share price over the last five years due to the digital disruption in the media industry. From January 2016 to date, SPH’s share price has fallen by around 70% as print circulation of its newspapers and magazines has steadily declined. How will SPH survive in the coming years?

Here are seven things I learned from the 2020 SPH AGM.

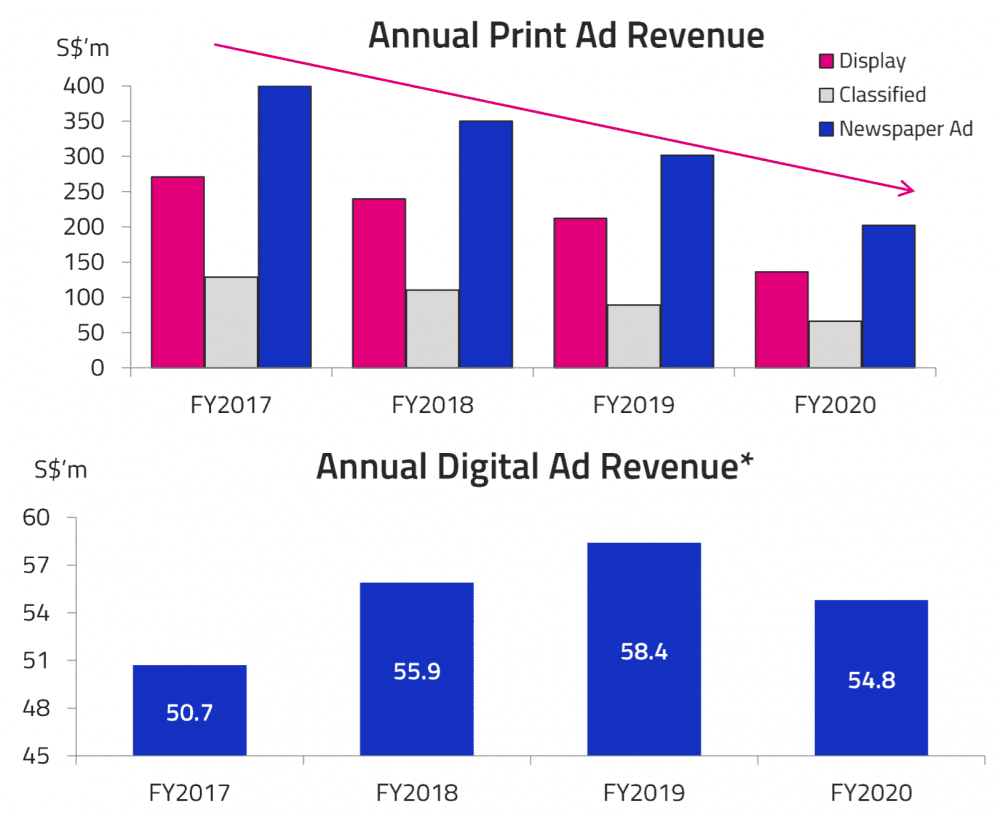

1. Operating revenue fell 9.8% year-on-year to S$865.7 million in FY2020. This was mainly due to a drop in media revenue as advertisers cut back on advertising spending due to the pandemic. SPH continued to see a steady decline in print circulation and advertising, traditionally the company’s largest revenue and profit drivers.

Despite the challenging year, SPH recorded an operating profit of S$110.2 million in FY2020. However, it made a net loss attributable to shareholders of S$83.8 million due to a $232.0 million non-cash decline in valuation of SPH’s property portfolio because of the pandemic.

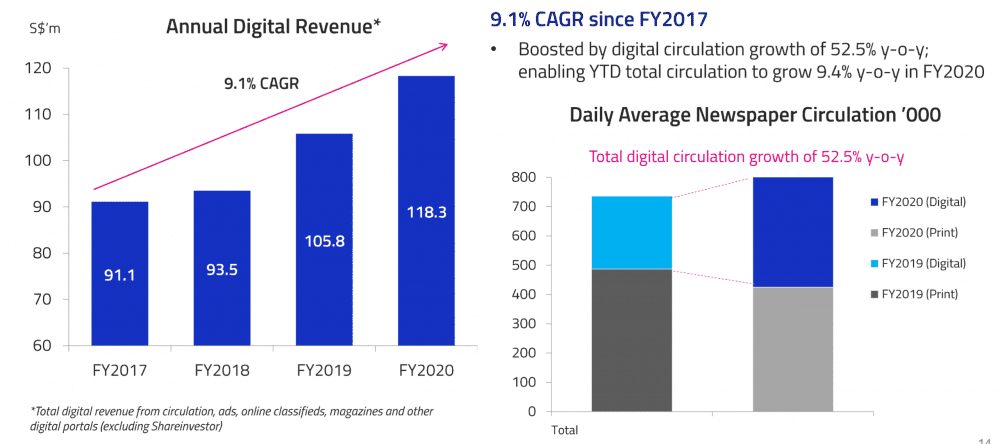

2. SPH’s digital circulation now exceeds its print circulation. Daily average print circulation copies declined 20.0% year-on-year, while daily average digital circulation copies grew 52.5%.

Since FY2017, SPH’s digital revenue has grown at a CAGR of 9.1%. But despite the growth in digital revenue, it has not been able to stem the decline in print revenue.

3. SPH owns a 65% stake in SPH REIT which owns five shopping malls in Singapore and Australia. Retail was one of the hardest hit sectors during the pandemic and SPH REIT was not spared. FY2020 net property income remained flat at S$181.6 million and distribution per unit fell 51.4% to 2.72 cents as the management cut distributions in order to conserve cash.

On a brighter note, sales have picked up for SPH’s condominium project, Woodleigh Residences, after the lifting of the Circuit Breaker in Singapore. The project has sold approximately 60% of its units at an average price of S$1,908 per square foot.

4. SPH is a sizable owner-operator of purpose-built student accommodation (PBSA) with 28 properties housing 7,723 beds in the UK and Germany. Despite the pandemic, PBSA net operating income increased by 29.0% year-on-year in FY2020. However, the COVID-19 situation in the UK is a concern which would reduce demand as international students choose to stay away from the country.

SPH is open to spinning off its PBSA business as a separate REIT listing but gave no further details.

5. Aged Care revenue increased 93.6% year-on-year, boosted by the sale of personal protective equipment by subsidiary Life Medic during the pandemic. SPH currently owns five aged-care facilities in Singapore and recently acquired five more assets in Japan for S$65.8 million in February 2020. The management believes this segment is a growth opportunity due to the greying population, especially in Japan.

Four COVID-19 cases were detected at one of the Singapore aged-care facilities in May, but all have since fully recovered. Business operations were stable for the Singapore and Japan assets as they are on master leases with credible operators who continue to pay rent in full and on time.

6. As a founding member of M1, SPH currently owns a 16.1% stake the Singapore telecommunications company. M1 was awarded the joint rights to operate the upcoming 5G network in Singapore with StarHub, and recently launched its 5G service to customers in September.

SPH also leverages on M1’s mobile platform to offer special promotions to subscribers of The Business Times News Tablet. The subscription is bundled with a Samsung Android tablet that is preloaded with the ‘SPHtab’ app that gives readers access to the latest Business Times e-papers.

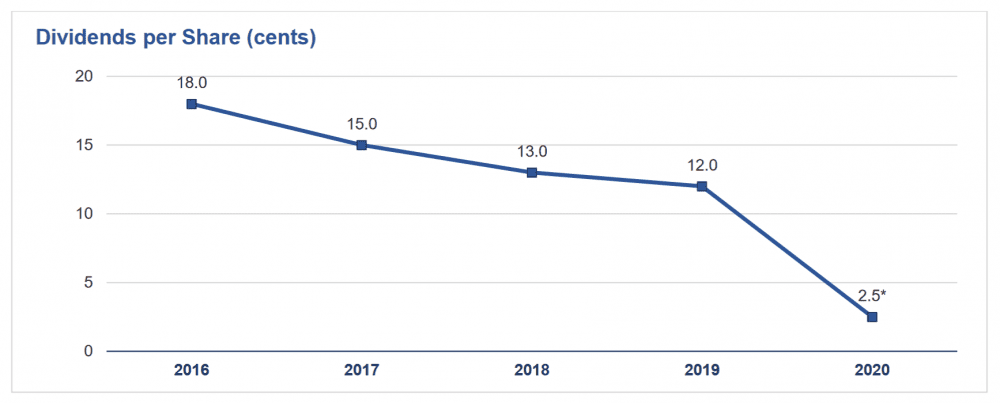

7. Dividend per share was drastically cut to 2.5 cents in FY2020 from 12.0 cents the year before. SPH’s dividend has steadily fallen since 2016 as its media business continues to struggle in the digital age. As SPH’s net profit continues to fall, its dividend will follow suit.

The fifth perspective

In the age of the Internet where consumers have access to global sources of news and information, SPH must now compete with international newspapers like The New York Times, The Wall Street Journal, and The Guardian. Although SPH retains specialised coverage on local news, it may not be enough to sustain its media business.

For investors who want partial exposure to SPH’s property business, they can consider an investment in SPH REIT instead which owns SPH’s retail properties.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »

I started following SPH about 15 years ago. It seems that their management can’t get anything right. In almost everything that they do they are an also-ran. The print media business is in retreat everywhere and traditional broadcast media appears to be following a similar path. When we look at companies that are successful over the long term there is usually something that they really excel at, and at one point SPH had a virtual monopoly in the highly profitable traditional newspaper business here in Singapore. That really ended when people started reading the news on their smartphones and tablet computers. SPH wisely diversified away from newspapers a long time ago, and property was one thing they had good go at. Mobile phones (M1) seems like a distraction from their core business.

SPH 16% share in M1 doesn’t look like a good fit with their core expertise, and they’re just re-selling capacity on other people’s network infrastructure (i.e. SingTel). Would anybody else be interested in doing this given the small size of the market? I’ve heard people making jokes about how clueless M1’s management is.

A few years ago I’d just read one of Warren Buffett’s unauthorized biographies, and I remember that Buffet had bought The Washington Post and several other big city newspapers because they were natural monopolies with great moats. I thought SPH should be the same, and I discussed it with a very wealthy local here in Singapore. The old man groaned and remarked how SPH had been a dud investment for him (remember this was 2005), he thought the management was clueless then. Fast forward to today and the SPH share price has gone from about S$4.50 back then, down to S$1.17 today. What’s more when you check the standard measures for financial health etc, it fails miserably. Some value pundits that SPH is trading at only about 21% of intrinsic value, but to me it just looks like a value trap. I do not own, and have never owned SPH shares – probably because of the advice that old bloke gave me.

Good sharing, Jonathan. You owe that wealthy bloke lunch!