Suntec REIT’s portfolio comprises prime retail and office properties in Singapore and the Australian cities of Sydney, Melbourne, and Adelaide. In Singapore, some of Suntec REIT’s well-known properties include Suntec City, One Raffles Quay, and Marina Bay Financial Centre (MBFC) Towers 1 and 2.

Looking at Suntec REIT’s geographic segments, Suntec REIT derived 84% of its net property income (NPI) from its Singapore properties in FY2019, while the rest was derived from its Australian properties. Suntec REIT’S largest property by NPI contribution was Suntec City, which contributed 51% of Suntec REIT’s NPI in FY2019.

Sector wise, Suntec REIT derived 68% of its NPI from its office properties while 28% was derived from its retail properties. The remaining 4% of its NPI was derived from its convention business segment.

Source: Suntec REIT 2020 AGM presentation slides

Suntec REIT’s retail malls appear to have been badly affected by the lockdown measures imposed due to COVID-19. Further, work-from-home arrangements in view of the lockdown has led firms to relook the need for a physical office, casting uncertainties for the future of Suntec REIT’s office spaces.

I tuned in to Suntec REIT’s AGM to find out how the management viewed these outcomes which may not bode well for Suntec REIT’s future. So here are 10 things I learned from Suntec REIT’s 2020 AGM:

1. Suntec REIT’s gross revenue increased 0.9% y-o-y to S$366.7 million in FY2019. The increase in gross revenue was mainly due to the stronger retail and office performances of Suntec City and the initial contribution of Suntec REIT’s newly acquired Australian property, 55 Currie Street. The increase was partially offset by lower revenue from Suntec Convention (higher number of corporate events were offset by fewer major convention events in FY2019) and from 177 Pacific Highway (due to a weakened Australian dollar against the Singapore dollar).

2. Suntec REIT’s NPI decreased by 2.0% y-o-y to S$236.2 million in FY2019. The decrease was due to the sinking fund contribution for Suntec City Office’s upgrading works, lower convention income, and a weakened Australian dollar. If we exclude the sinking fund contribution of S$19.3 million, NPI for FY2019 would be 1.3% higher y-o-y. The sinking fund contribution has no impact on the REIT’s distributable income.

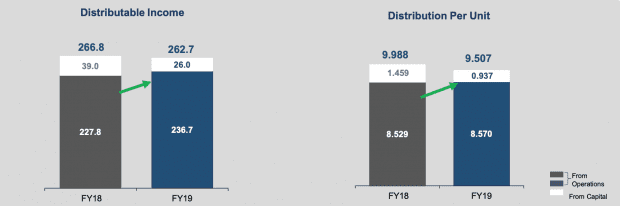

3. Suntec REIT’s distributable income and distribution per unit (DPU) decreased by 1.5% and 4.8% y-o-y respectively in FY2019. Although distributable income from operations increased by 3.9% y-o-y in FY2019 with higher contributions from Suntec City, Southgate Complex, MBFC Tower 1 and 2, and 55 Currie Street, this was offset by lower contributions from 177 Pacific Highway and One Raffles Quay, and a lower capital distribution.

Suntec REIT’s DPU decreased disproportionately (4.8%) compared to its distributable income (1.5%) due to an enlarged unit base.

Source: Suntec REIT 2020 AGM presentation slides

4. Suntec REIT completed a A$148.3 million acquisition of 55 Currie Street, a freehold Grade A office building at the heart of Adelaide’s Central Business District (CBD), in September 2019. This marks Suntec REIT’s first foray into the Adelaide market. The building has a 91.7% committed occupancy rate whose key tenants include the Commonwealth government and South Australian government.

The acquisition of the property is expected to be DPU-accretive for the REIT. The property also has a 27-month rent guarantee on vacant spaces with an annual rental escalation of 3.50% to 3.75%.

5. Suntec REIT also completed a A$295.0 million acquisition of 21 Harris Street, a freehold Grade A office building located 2 kilometres west of Sydney’s CBD, in April 2020. It has a 66.2% committed occupancy and is anchored by Publicis Groupe, a French multinational advertising and public relations company, and one of the largest marketing and communications companies in the world by revenue. The acquisition of the property is expected to be DPU-accretive for the REIT.

Although it has a rather low committed occupancy rate, the property also has a three-year rent guarantee on vacant spaces with an annual rental escalation of 3.0% to 4.0%. Suntec REIT CEO Chong Kee Hiong sees ‘no problem’ filling up the vacant spaces in the property in a strong Sydney market.

6. Suntec REIT has an Australian premium-grade office building at Olderfleet, 477 Collins Street that will start contributing income to the REIT in the second half of 2020. The property has a 93.7% pre-committed occupancy rate whose key tenants include Deloitte, Lander & Rogers and Norton Rose Fulbright. The acquisition is also expected to be DPU-accretive and has a five-year rent guarantee on vacant spaces with an annual rental escalation of 3.5% to 4.0%.

7. Suntec REIT’s Singapore and Australia properties’ occupancy rates have done reasonably well in FY2019. All of Suntec REIT Singapore office properties — Suntec City Office, One Raffles Quay, MBFC Towers 1 and 2, and 9 Penang Road — have high occupancy rates of at least 96%. Their overall Singapore occupancy rate is 99.1%, above the overall CBD occupancy rate of 95.9%. In particular, Suntec City Office has achieved a 100% committed occupancy rate, achieving seven consecutive quarters of positive rental reversions.

Source: Suntec REIT 2020 AGM presentation slides

Suntec REIT’s retail properties — Suntec City Mall and Marina Bay Link Mall — have an overall occupancy rate of 99.5%, higher than the market occupancy of 98.2%.

Source: Suntec REIT’s 2020 AGM presentation slides

Suntec City mall’s footfall and tenant sales per square foot also recorded increases of 3.9% and 0.7% respectively in FY2019. If we were to exclude the opening of Superpark at the end of 2018 in Suntec City (which skewed the tenant mix) in the calculation of tenant sales, tenant sales per square foot has in fact increased by 3.2% y-o-y.

And Suntec REIT’s Australia office properties have an overall occupancy rate of 97.8%, higher than the nationwide CBD occupancy rate of 91.7%.

Source: Suntec REIT’s 2020 AGM presentation slides

8. The CEO shared that COVID-19’s impact on the REIT’s Singapore office portfolio remains uncertain. The uptake of Suntec REIT’s office properties might be impacted as companies find that working-from-home arrangement is an option post-pandemic. As office workers spent less time in the physical office, Suntec REIT might explore the implementation of co-working and flexible workspaces to cater to the growing need for these spaces.

The CEO shared that Suntec REIT’s rental revenue will remain robust with i) the completion of 52% of FY2020 lease renewals for the Singapore office portfolio and ii) strong rental reversions due to limited office supply as the circuit breaker delayed the construction of new office spaces. He views that office portfolio occupancy will remain healthy, within the market range of 95%.

The CEO also shared that 43% of the space vacated by UBS has been pre-committed in One Raffles Quay and Suntec City Office. But due to the pandemic, it will take a longer time for Suntec REIT to backfill the remaining space.

9. The CEO shared that Suntec City Mall faces strong headwinds for the remainder of 2020. Due to lockdown measures taken to reduce the spread of COVID-19, the mall experienced a significant drop in shopper traffic. However, as Singapore enters Phase 2 where lockdown measures are eased, the CEO expects a gradual recovery in shopper traffic from Q3 2020 onwards. Weak tourist arrivals to Singapore will not have as significant an impact on Suntec City mall since the mall’s primary catchment is predominantly made up of office workers and locals.

Although Suntec REIT achieved a double-digit positive rental reversion in Q1 2020, rental reversion for remaining quarters is likely to be negative due to weaker market demand. The CEO expects its overall mall occupancy rate to trend closer to the nationwide average of low 90s due to the non-renewal of some leases.

The CEO thinks that Suntec City mall will see shopper traffic gradually increase to pre-pandemic levels of more than 4 million visitors a month due to its strategic location and superior transport connectivity.

10. The outlook for Suntec REIT’s Australian properties is mixed. With new retail and office supply in 2020 together with weaker economic activity, these will affect occupancy rates at Suntec REIT’s retail and office properties in Sydney and Melbourne. Overall, Australia’s retail sector will continue to face challenges with weak consumer spending and COVID-19 restrictions.

The office properties are expected to remain resilient with strong occupancy rates, long weighted average lease expiries, and minimal lease expiries in 2020. On a same-store basis, retail income is expected to decrease slightly in 2020 due to rent assistance for qualifying SME tenants. However, overall income is expected to increase over 2019 with contributions from 21 Harris Street and 477 Collins Street.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »