Mapletree Commercial Trust (MCT) is a Singapore-focused REIT that invests in a diversified portfolio of income-producing real estate used primarily for office or retail. As at 31 March 2021, MCT’s portfolio comprised five properties in Singapore.

During the 2021 AGM, CFO Janice Tan presented MCT’s FY20/21 financial highlights while CEO Sharon Lim covered the key operational highlights. Here are eight things I learned from MCT’s 2021 AGM.

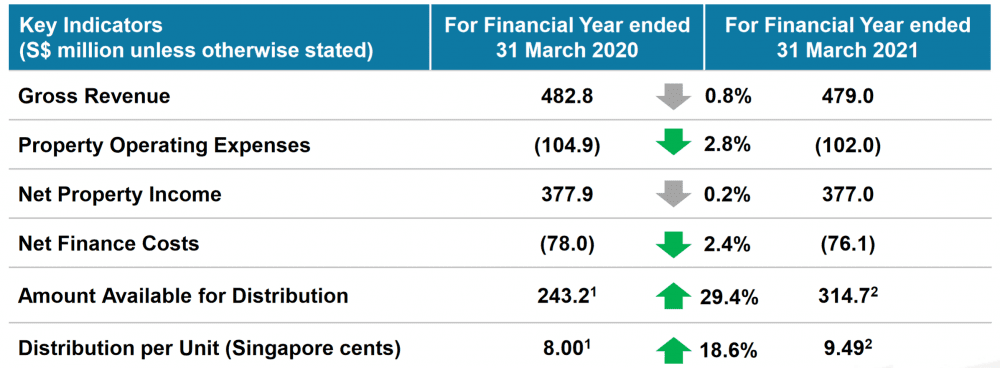

1. MCT posted gross revenue of S$479.0 million, down 0.8% year-on-year while net property income (NPI) was S$377 million, down 0.2% year-on-year. This was due to the impact of COVID-19 and rental rebates of more than S$70 million to help eligible retail tenants, although MBC II’s (acquired in November 2019) first full-year contribution helped to cushion the impact.

The amount available for distribution was S$314.7 million, up 29.4% year-on-year, while distribution per unit (DPU) was 9.49 cents, up 18.6%. The CFO shared that S$43.7 million of distribution was retained in 4Q 19/20 in order to boost MCT’s liquidity in a highly volatile environment to maintain prudence. Since then, MCT has released S$28 million of the retained cash in FY20/21. Excluding the release of S$28 million in retained cash, the DPU for FY20/21 would have been 8.65 cents.

2. Value of investment properties was S$8.7 billion, 2% lower compared to last year as a reduction in market rents and growth brought about by COVID-19 lowered property valuations. However, Tan said that this was offset by compression in capitalisation rates for MBC 1, MBC 11, and MLHF due to market transactions.

3. Total debt rose marginally to S$3.03 billion. Tan said that 70.7% of debt was fixed rate debt which provides MCT reasonable certainty on its interest expenses. MCT’s gearing ratio remained healthy at 33.9% with a sizable debt headroom of S$2.8 billion based on the statutory gearing limit of 50%.

Interest coverage ratio was 4.4 while average term to maturity of debt remained at 4.2 years. Moody also reaffirmed MCT’s BAA1 rating and upgraded the outlook from negative to stable in May 2021.

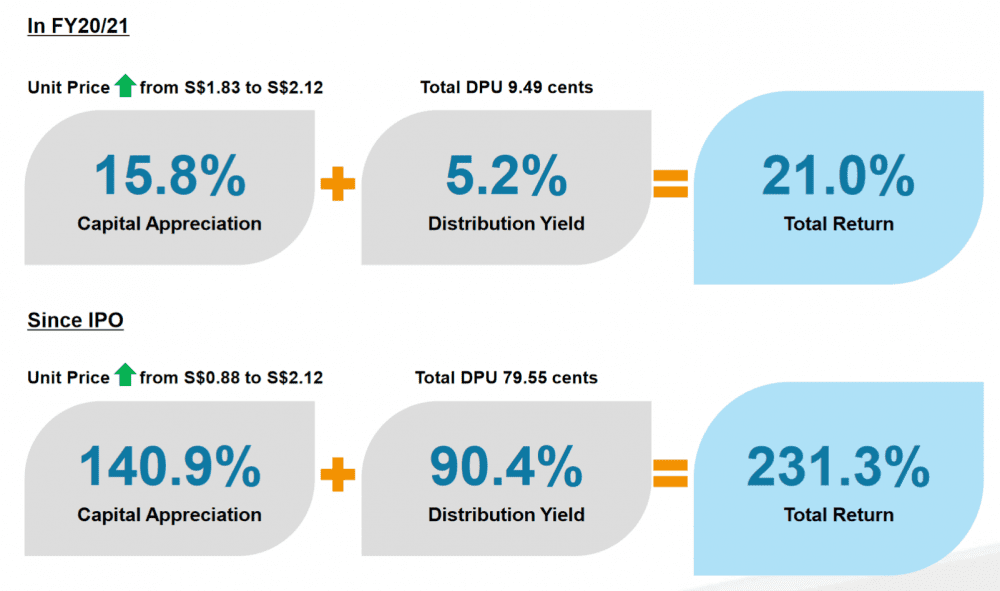

4. Since MCT’s listing 10 years ago, gross revenue and NPI have grown at compounded annual growth rates of over 10% and 12% respectively. Despite a global backdrop of economic dislocation and volatility in the stock market, MCT’s share price has constantly out-performed indices. Based on a closing price of S$2.21 as at 31 March 2021, MCT generated 21% of total returns to unitholders in FY20/21.

For those who invested since IPO, they would have made more than 230% of total returns, made up of 140% in capital appreciation and over 90% in distribution.

Tan added that this year’s distribution total of S$314.7 million and DPU of 9.49 cents translates to a compounded annual growth rate of 13% and 6% respectively.

5. Largely anchored by MBC II, office and business parks assets recorded S$309 million of gross revenue and S$251 million of NPI, up 13% and 14% respectively from a year ago. Mapletree Anson also contributed higher earnings in FY20/21 due to higher occupancy and step-up rents. In order to maintain steady income, CEO Sharon Lim said that MCT placed priority on occupancy and early engagement with tenants who were recalibrating space requirements in view of work-from-home initiatives.

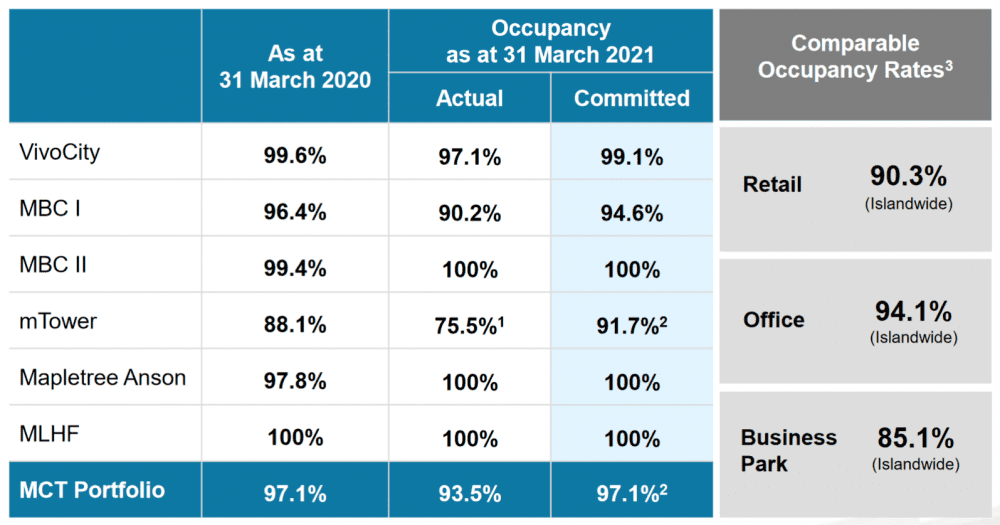

As at 31 March 2021, MCT’s overall portfolio occupancy commitment was 97.1%. MBC II, Mapletree Anson, and MLHF were 100% committed, and MBC I was committed at 94.6%. This compares well against industry benchmarks for retail (90% occupancy rate), office (94%), and business parks (85%) in Singapore.

On mTower, Lim said that the property’s committed occupancy was 79.7% as a result of a mutual agreement to terminate a lease ahead of its commencement. She revealed that MCT will receive pre-term compensation of 16 months, and that marketing and backfilling of the space is in progress. Portfolio average of lease expiry remains well balanced at 2.4 years.

6. VivoCity’s revenue and NPI was down 19.5% and 20.8% year-on-year respectively. This was due to the impact from COVID-19 and rental rebates granted to eligible tenants. In 4Q 20/21, tenant sales grew 5.2% year-on-year and compared well against previous quarters. This was due to shopper traffic and sales showing progressive recovery that corresponded with the phased easing of health and safety measures.

During the year, VivoCity secured the expansion of existing tenant, Adidas, which launched two flagship stalls. Lim shared that this is part of a longstanding trend of retail consolidation, where retailers consolidate their retail footprint by focusing on better-performing stores. VivoCity also undertook asset enhancements that include the reconfiguration of Best Denki’s space on Level 2, and the revitalisation of the Level 1 F&B cluster with a fresh mix of dining concepts.

7. Unitholders wanted to know if there were any plans to reduce reliance on VivoCity as it currently accounts for 33% of total NPI. Does MCT have any acquisitions in the pipeline or any plans to make acquisitions overseas?

The management responded that VivoCity made up close to two-thirds of the portfolio before the acquisition of MBC I in 2016. However, MCT has since enhanced its portfolio diversification with the acquisitions of MBC I and II.

MCT currently has six right-of-first-refusal assets from sponsor Mapletree Investments and will evaluate the opportunities when the sponsor is ready to divest. MCT remains focused on Singapore as it believes its existing assets have strong potential for growth.

8. Unitholders also wanted to know the outlook for the retail, office, and business park sectors. According to CBRE, the recovery of the retail market is expected to be prolonged. As borders continue to be closed, the retail market will be largely supported by domestic spending. Moving forward, landlords are expected to curate their tenant mix and recalibrate their malls’ positioning, while leasing activities have gained traction with new openings of mostly F&B concepts in 2021.

The office market is still facing some pressure in the first half of 2021 and showing signs of improvement in the second half. Tenants from the technology, information and communications, financial, and insurance sectors will continue to drive leasing activities. Global uncertainties are likely to continue into 2021 and lead to delayed business openings or expansions.

The business park space continues to show resilience underpinned by stable occupancy and healthy fundamentals, Notwithstanding the impact of COVID-19, indicators have shown that the manufacturing sector is on a sustained growth trajectory, driven by biomedical and electronic services. Leasing demand continues to be led by high value-added industries such as technology, biomedical, pharmaceutical, and advanced manufacturing.

The fifth perspective

Over the last year, MCT’s portfolio has demonstrated resilience and is expected to continue to provide stable cash flows from a well-diversified portfolio. The acquisition of MBC II has boosted and added diversification to income streams.

Prudent capital management and financial flexibility has also enabled MCT to release S$28 million to unitholders which resulted in higher DPU amidst the pandemic. MCT has also continued to strengthen its assets by active tenant remixing and asset enhancement initiatives; MCT properties continue to appeal to reputable tenants.

Full recovery will be dependent on the pace of vaccination and the gradual reopening of the Singapore economy as the COVID-19 situation remains fluid. MCT remains confident that it will overcome the current headwinds, given its firm fundamentals, long-term strength, and portfolio of best-in-class assets.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »