Singapore Exchange (SGX) held its annual general meeting just last Thursday. As one of Singapore’s beloved blue-chip stocks and with a virtual monopoly on Singapore securities and derivatives trading (more exchange licenses in Singapore are unlikely to be granted anytime soon), SGX’s position is enviable.

Despite that, concerns have sprung up regarding SGX’s ability to grow for the long term. SGX discontinued its MSCI equity index futures and options contracts (except for those under MSCI Singapore) when its licence agreements expired in February 2021, thus ending its 23-year partnership with the American finance company.

And to heat things up, Hong Kong Exchange inked a deal with MSCI to launch derivatives for Asia and Emerging Markets. To marketplace operators like SGX, trading activity and its associated necessities (trade clearance and settlements, etc.) are its lifeblood.

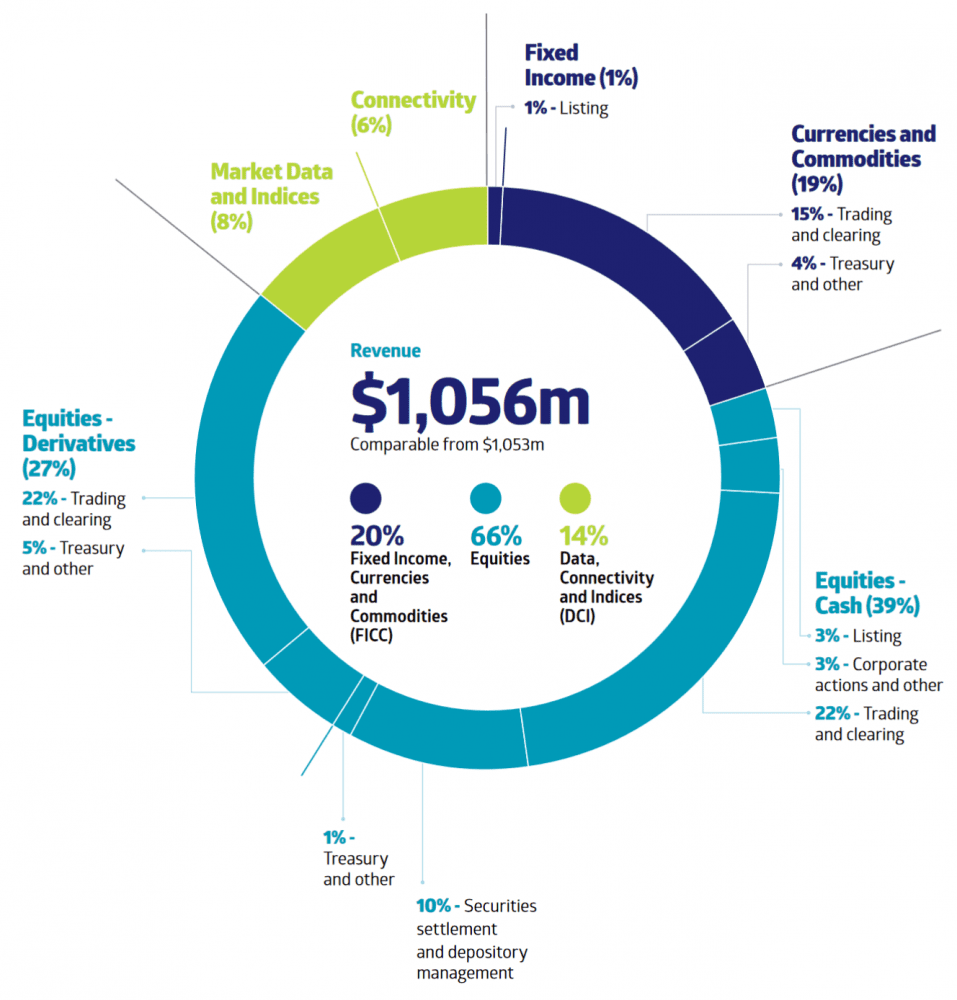

SGX’s own annual report shows this:

Six months has passed since the ending the MSCI deal. So, it’s always interesting to hear what updates have been announced and how management is aiming to expand the business in light of global challengers (i.e., other exchanges across the world).

Here are eight things I learned from the 2021 SGX AGM.

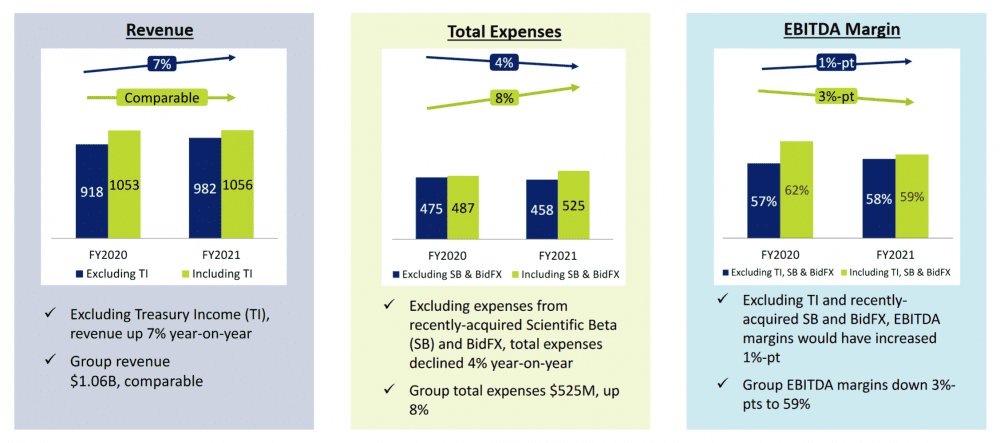

1. FY2021 performance in line with management expectations. Excluding the impact of Treasury income and expense growth from acquisitions, SGX’s core underlying business saw 7% revenue year-on-year growth and further expense declines.

I wouldn’t look at margins dropping as a warning sign either. CFO Ng Yao Loong made it clear that while the acquisitions have lower margins — and hence lowered overall margins for SGX — the acquired business have higher growth synergies. As SGX digests the acquisition, it should see margins go back up slowly over time.

Treasury income is the interest spread that SGX makes between global market interest rates, and cash deposited by investors to trade. Naturally, if interest rates lower, so does SGX’s income, and vice versa.

2. Healthy coverage ratio allows for future growth aspects. While this wasn’t specifically mentioned by the management team, we can look at their past actions to understand why a good coverage ratio and liquidity is required – future acquisitions.

SGX’s core competency is operating as a financial services business specifically tailored for market exchange operations. Anything that they can expand into requiring such services or better utilizing their cost base of carrying on such business will add value to the operating base. The recent acquisition of MaxxTrader further confirms this.

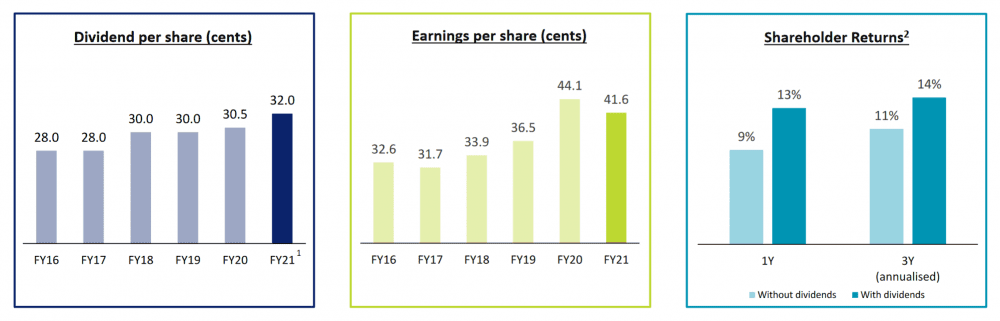

3. SGX has increased dividends twice over the last five years, returning over S$3 billion over 10 years. Singapore listed companies differ from U.S. ones mainly in the form of capital returns. The mechanics of capital returns sound complex but, in reality, are not. Capital is returned either through share buybacks (enhancing each shareholder’s slice of the profit pie), inherent share price gains from reinvestments in the business (management must ensure cashflows have high incremental returns on capital in the first place), or through dividends (mainly for slower growing business or more mature businesses).

In this regard, I’m happy to see SGX increasing dividends slowly and having returned so much money over the past decade. This ensures that even if the share price has been relatively flat, extra income has been returned to shareholders, and best of all, it’s tax free. That the dividend can grow over time is an added bonus.

4. Proposed final quarterly dividend of 8 cents per share, bringing total dividends for FY2021 to 32 cents, an increase of 5% from FY2020.

It’s nice to see dividends being increased as stated earlier, but I would urge long-term shareholders to also keep an eagle eye on whether operating income — from which dividends is derived — is also rising at the same pace. If dividend growth exceeds income growth, we can expect some cushion from expense cutting, but not much and not for the long term. SGX has done well here; earnings per share has at least remained relatively stable and operating income has grown about 50% since 2009.

5. MaxxTrader is SGX’s attempt to gain a further foothold in the US$6.6 trillion-dollar global forex trading market. I’m not tied up with forex market updates so I can’t say for certain whether this is a good acquisition or not. But from a strategic perspective, this makes sense. If you’re in SGX’s position, there must be a cost base – the cost of running as an exchange, overhead, legal and compliance fees, clearing fees, etc. The issue here isn’t scale – SGX can clearly serve more consumers and earn more money over time. The issue here is which markets SGX has access to in order to utilize its base better.

Think of it like operating an online store. Clearly there are costs involved, network provider costs, logistics backend costs, accounting costs, etc. Let’s say you have $10K per month in operating expenses. The first $10K of revenue might go towards paying operating expenses, but the next $10K drops to income and cash flow because you don’t have that much in operating expenses to grow (this isn’t a clear apples-to-apples comparison, but I hope you get the point).

SGX has a similar issue. It needs to utilize its cost base of functioning as a clearing and settlements business/exchange operator/financial services business to better bolster the bottom line.

6. A shareholder asked whether SGX can compete effectively on product offerings. I found this comment interesting. As mentioned before, SGX is a platform and network effect business. Not a simple product-to-product business. CEO Loh Boon Chye also noted an interesting dynamic, stating that a product with great liquidity allows the network effect to grow since other products gain increased access to trading. I think this seems underappreciated.

7. An investor asked what is the expected internal rate of return for acquisitions such as Scientific Beta and BidFX? There was some hemming and hawing, but CFO Ng Yao Loong stated that SGX aims to grow revenue at more than 10% and has also stated that Scientific Beta and BidFX are operating cash flow positive and have a higher rate of return than their cost of capital. While the acquisitions have slightly lower margins, both businesses are faster growing.

Also noted by him was that both acquisitions are performing according to expectations pre-acquisitions. There’s not a lot to take home from that statement since I doubt any executives out there would state an acquisition isn’t performing as they had hoped. My best guess is investors must wait and see if the contribution to net income is really as good as it’s expected to be.

8. Will SGX be launching a cryptocurrency exchange platform in view of the asset’s emergence? SGX CEO: ‘Many views have been expressed about cryptocurrency. The asset has probably established itself as a trading instrument, but I’m not quite sure it’s an asset class yet. But it could be a trading instrument that stays around for a while. As such, crypto listing might be something that SGX will consider in the future. However, of more use is the underlying distributed ledger technologies. SGX has joint ventures and investments that will be powered by blockchain technology.’

The fifth perspective

SGX operates essentially as a financial services business. Its future performance will depend on the marketplaces it can access and the volume of trades and liquidity it can serve. Growth is slow but dividends are steady and rising. Investors need to keep an eagle eye on which new markets SGX enters and how much it spends on acquisitions, and ultimately whether or not these acquisitions make long-term financial sense.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »