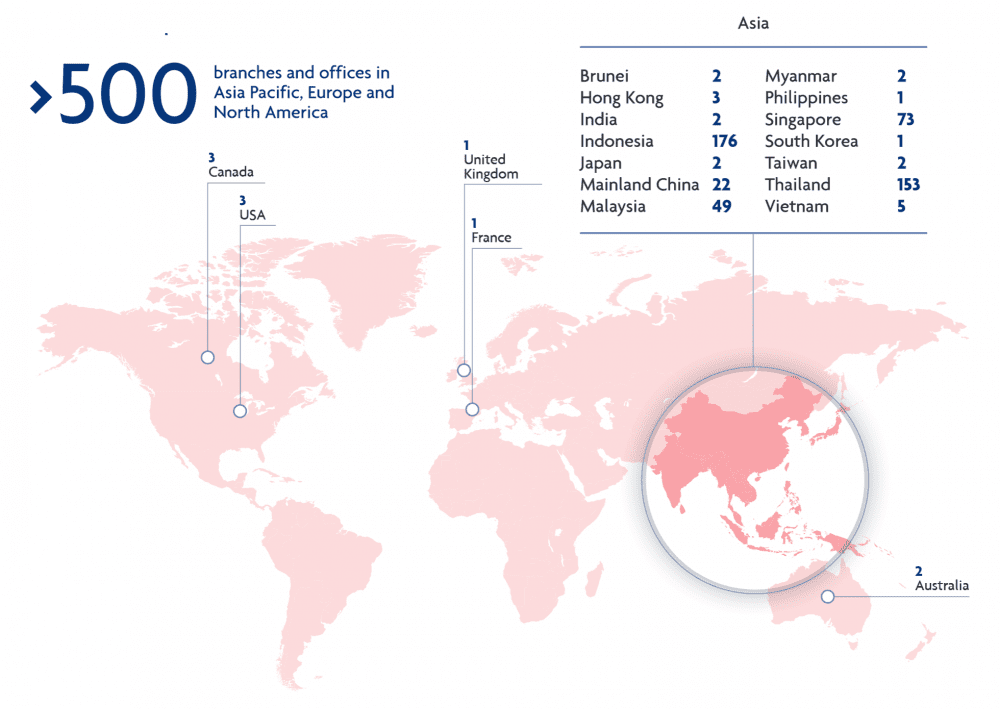

United Overseas Bank (UOB) is a leading bank in Asia with a global network of over 500 branches and offices in 19 countries and territories in Asia-Pacific, Europe, and North America. As of 31 December 2021, UOB has total assets of S$432 billion. In terms of total assets, the bank is the third largest in Southeast Asia. UOB has a market capitalisation of S$44.0 billion as of 31 May 2021.

UOB currently offers commercial and corporate banking services, personal services, private banking, and asset management services, as well as corporate finance, venture capital, investment, and insurance.

I attended UOB’s 2021 AGM to learn more about how the pandemic impacted UOB’s performance and its future expansion plans. Here are the seven things I learned from the 2021 UOB AGM.

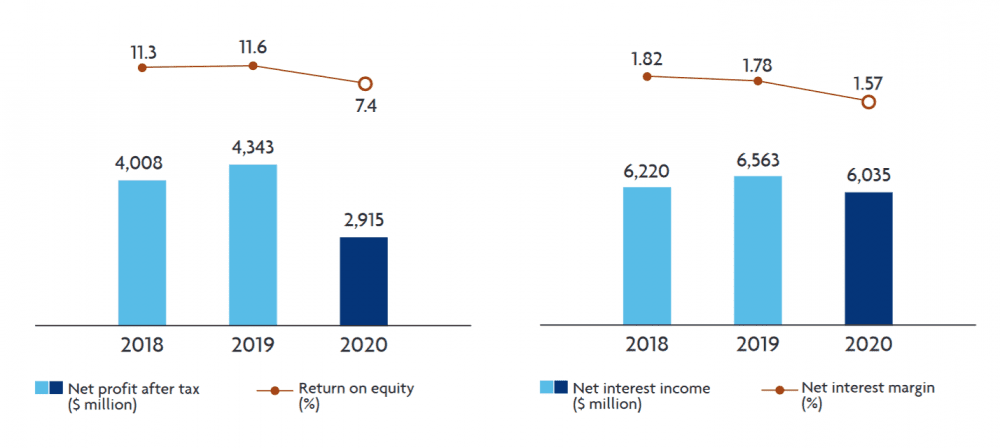

1. Net profit after tax fell 33% year-on-year to S$2.9 billion in FY2020 from S$4.3 billion in FY2019. This was caused by the economic contraction a year ago amid the global pandemic with lower margins from benchmark rate cuts and reduced customer activities.

Despite the challenges, UOB’s total capital adequacy ratio remained robust at 18.4%, well above the MAS minimum requirement of 10%. CEO Wee Ee Cheong added that an additional S$900 million in pre-emptive credit was set aside in 2020 to strengthen the bank’s balance sheet.

2. Net interest income fell 8% year-on-year to S$6.0 billion in FY2020 from S$6.6 billion in FY2019. Net interest margin fell 21 basis points to 1.57%. As policymakers across regional markets reduced interest rates in 2020 to support the economy and market liquidity, net interest income and margin naturally fell as well.

3. On the bright side, assets under management for the Wealth Management segment increased 6% year-on-year to S$134 billion in FY2020. Wealth Management fees increased by 11% year-on-year despite a challenging macro environment as customers continued to place their trust with the bank.

4. According to the management, UOB has the most extensive regional network in Southeast Asia among Singapore banks. The management said the bank’s integrated regional platform enables UOB to provide customers a seamless experience, faster time to market, and more robust risk management and operational efficiency. UOB’s connectivity with Greater China enables it to help businesses seize fast-growing cross-border opportunities.

5. In response to a shareholder question why UOB’s share price was recently lagging behind DBS’s, the management reminded shareholders to keep a long-term perspective. UOB continues to invest in the right capabilities and technology to drive transformation and strengthen its regional presence. Southeast Asia is a region with mid- to long-term growth potential, underpinned by opportunities in growing connectivity and rising affluence.

6. UOB added in their responses to shareholders that the bank is at the forefront of adopting digital banking strategies for small and medium-sized enterprises (SMEs). UOB continues to invest in technology capabilities from AI, data analytics, robotic process automation, and cloud computing to ensure that banking with UOB is seamless, simpler, and more secure for its customers. Some SME banking initiatives include:

- Launching FinLab Online, a digital learning platform which helps SMEs and start-ups to develop digitalisation strategies and business operating solutions

- helping retail SMEs access digital solutions through UOB’s partner, Synagie, to access multiple online e-commerce platforms in ASEAN

- collaborating with F&B digital solutions providers to help F&B SMEs in Singapore and Malaysia expand their client reach through online storefronts

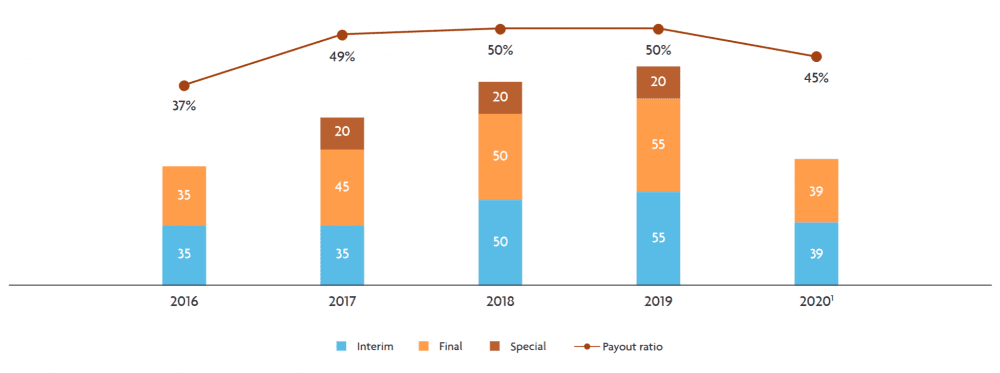

7. UOB declared a total dividend per share of 78 cents for FY2020, down from S$1.30 the year before. The drop in dividend is in line with the MAS recommendation that local banks cap their FY2020 dividends at 60% of that for FY2019. Based on UOB’s share price of S$26.10 (as of 3 June 2021), its dividend yield is 3.0%. The CEO said UOB is waiting for further guidance by MAS this year on whether the dividend cap would be relaxed.

The fifth perspective

UOB has delivered steady growth in earnings and dividends over the years, except for 2020 due to COVID-19. Early shoots of recovery can be seen in 2021 as the pandemic eases and economies around the world recover.

The MAS is expected to update on the cap on dividends by July 2021. Assuming the cap is removed and dividends eventually return to FY2019 levels, UOB’s prospective dividend yield is 5.0% at its current share price. (Note: UOB has a special dividend in seven out of the last 10 years.) Income investors who don’t mind waiting for UOB to recover may want to consider having a look at the bank right now.

Watch our roundtable: Are Singapore Banks Still Undervalued in 2021?

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »