Established in 1988, Hartalega Holdings Berhad is a leading nitrile glove manufacturer that produces over 44 billion pieces of gloves a year. Hartalega exports its gloves to more than 70 countries. The company had a good run in 2021 and 2022 as customers scrambled to buy gloves during the COVID-19 pandemic. Post-pandemic, the glove maker is facing issues ranging from glove oversupply to stiff competition from mainland Chinese players.

Being the pioneer in introducing lightweight nitrile gloves to the market, a move that spurred the transition from natural rubber to nitrile gloves, can Hartalega successfully navigate the challenges of the current difficult environment?

Here are 10 things I learned from the 2023 Hartalega AGM.

1. Revenue decreased 69.5% year-on-year to RM2.4 billion in 2023 because of lower sales volume, significantly lower average selling prices (ASPs) of gloves as well as higher energy and labour costs. Glove customers overpurchased during the pandemic and are still having excess inventories. Softer glove demand has sent the glove ASPs spiraling down.

2. The company sank into the red in 2023 with a net loss attributable to shareholders of RM235.1 million compared to its record-high net profit of RM3.2 billion in 2022. In addition, a one-off full impairment charge amounting to RM347 million was incurred in 2023 to decommission its less efficient and less cost-effective Bestari Jaya facilities by March 2024. Its production lines can only produce between 33,000 and 45,000 pieces of gloves per hour which is subpar compared to the industry. Excluding the impairment, it recorded a net profit attributable to shareholders of RM111.9 million in 2023. As a result, the company did not pay a dividend to shareholders for the first time since its listing. The management will strive to maintain a dividend policy of a 60% payout ratio once the company returns to the black.

3. In Q1 2024, the glove manufacturer continued to be affected by subdued glove demand as its revenue reduced 48.0% year-on-year to RM440.0 million. It posted a net loss attributable to shareholders of RM52.5 million compared to a net profit of RM88.3 million in the previous corresponding quarter.

Severance payment to retrenched employees totalling RM47 million was also incurred in Q1 2024. More than half of Bestari Jaya employees will find new roles at the Next Generation Integrated Glove Manufacturing Complex (NGC) plants. Monetary, relocation, and outplacement support will be given to existing and retrenched employees. The production capacity decommissioned at Bestari Jaya will be replaced by the more efficient NGC 1.5 in Sepang in the future. The existing land where Bestari Jaya facilities are located will be sold.

Hartalega’s present production capacity ranges from 40% to 50%, surpassing the Malaysian industry average of 30% to 40%, while lagging behind Chinese players who operate at 70% to 80%. It is anticipated that Hartalega’s production capacity will soon increase to a range of 50% to 55%.

4. China is the largest consumer of coal globally. The Chinese glove players benefit from cheap coal and have a low energy cost base.According to CEO Kuan Mun Leong, their production costs are about 8% lower than that of Malaysian players. Energy costs typically make up about 20% of Hartalega’s costs.

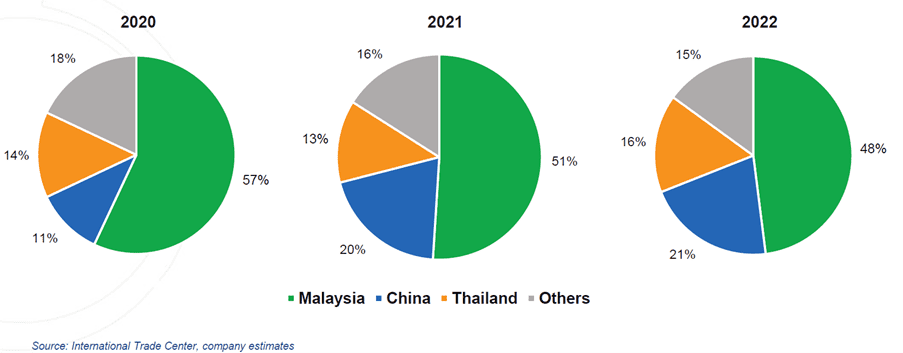

In recent years, Chinese glove manufacturers have been steadily gaining market share at the expense of Malaysian counterparts, who rely on comparatively costly natural gas for their operations. However, it’s important to consider that market share data for 2022 might be skewed due to excess inventories held by glove customers in developed countries.

A shareholder proposed to the management the idea of increasing electricity production through biomass utilization, given the abundant availability of palm oil in Malaysia. The company currently operates a biomass energy plant powered by empty oil palm fruit bunches. However, the founder mentioned that sourcing an adequate supply of these fruit bunches within the country has proven to be a challenging task.

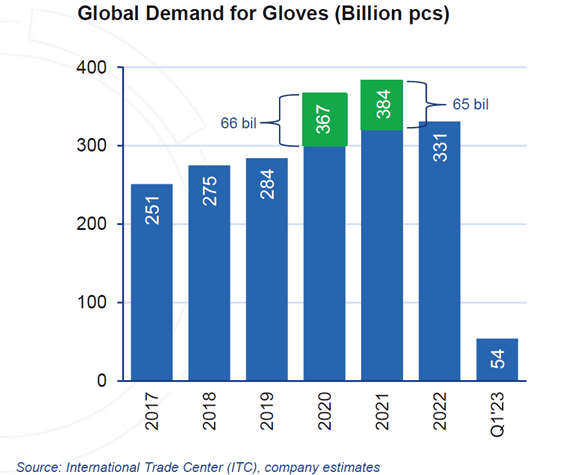

5. Malaysian glove producers including Hartalega are expected to fully recover by 2024 and 2025. According to management estimates, customers from developed nations have accumulated an excess of 131 billion gloves (illustrated by the green bars below), which are set to expire in 2024 and 2025. It’s expected that a supply-demand balance will be restored, as gloves remain an essential commodity. Historically, the global glove demand has exhibited a compounded annual growth rate averaging between 6% and 8% over the past two decades prior to the pandemic.

The CEO also mentioned that Malaysian glove manufacturers are poised to recapture some market share from their Chinese counterparts, as buyers seek to diversify their sources of gloves due to geopolitical tensions and concerns about human rights compliance. Concurrently, some Chinese players have deferred their expansion plans, and a few newer entrants have exited the glove industry. As the market rebounds, Malaysian manufacturers are expected to make a swifter recovery. On the other hand, Chinese manufacturers stand to benefit from their cost-efficiency and may potentially engage in a competitive price battle to maintain or gain additional market share. The current situation remains dynamic and uncertain, echoing the management’s description during several instances at the AGM.

6. Hartalega’s gloves are typically priced at an average of US$20 per thousand pieces, whereas Chinese competitors offer theirs at roughly 15% lower prices. The average selling prices (ASPs) of gloves have been on a decline since mid-2021, reaching their current low point. While there has been a slight uptick in ASPs since the beginning of 2023, the short to medium-term outlook suggests that prices may remain at their current level or even lower until at least March 2024. The management’s response appears somewhat uncertain, reflecting the influence of factors beyond Hartalega’s control, such as its competitors’ expansion plans and capacity adjustments. Hopefully, the situation will become clearer by 2025. As of June 2023, Hartalega maintains a net cash position of RM1.5 billion and remains financially robust, capable of withstanding unforeseen challenges.

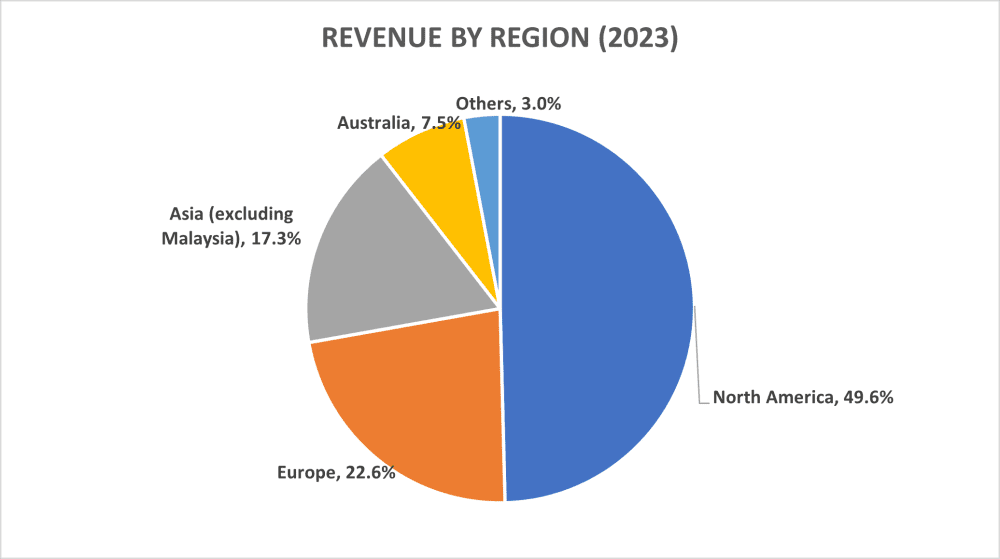

7. The revenue generated from Asia saw growth, rising from 13.5% in 2022 to 17.3% in 2023. However, it’s important to note that these figures might not accurately reflect the actual situation, as the balance between glove supply and demand has not yet stabilized. Over the long term, it is anticipated that glove demand in this region will continue to increase. This growth can be attributed to heightened awareness of hygiene, low per-capita glove usage, and the current modest baseline of glove consumption. In comparison, glove consumption per capita is 10 pieces in Asia and 150 pieces in developed countries.

8. A number of shareholders brought up the topic of diversifying the company’s business, including potentially expanding into upstream nitrile raw material production and glove formers. Personally, I had concerns about this potentially spreading the company too thin. Fortunately, it seems that the management is remaining focused on their core competency, which is glove manufacturing.

9. Apart from its role as an original equipment manufacturer, Hartalega aims to expand its presence in developed markets by increasing the sales of its proprietary glove brands, such as anti-microbial and Colloidal Oatmeal System (COATS®) gloves. This strategic move is driven by the prospect of higher margins and average selling prices (ASPs) in these markets, achieved through heightened brand awareness among end-users. One of Hartalega’s in-house brands, GloveOn, holds a dominant position in Australia, commanding a 40% market share in government hospitals.

Furthermore, the company is actively pursuing certification from the U.S. Food and Drug Administration for its anti-microbial gloves, despite their initial launch back in 2018. These specialty gloves did not receive significant attention during the early stages of the COVID-19 pandemic, as the market was primarily focused on procuring standard gloves rather than specialized variants.

10. The company is set to allocate approximately RM70 million for investments in upcoming years, targeting initiatives aimed at enhancing productivity and efficiency. These efforts are expected to yield annual savings of RM40 million in both 2023 and 2024. Hartalega’s competitive advantage lies in its internally developed technology and exclusive partnerships with technology providers, giving the company an edge over its industry counterparts. For example, Hartalega’s automated packing system handles nearly all of its gloves (99%) with no need for human intervention.

The fifth perspective

Hartalega’s success over the past few decades has been attributed to its prudent management and its proprietary in-house technology, which has allowed the company to achieve economies of scale in glove production. It’s evident that the founder takes great pride in the company’s achievements.

However, the post-pandemic landscape has brought changes to the competitive environment. It’s challenging to pinpoint precisely when glove customers will fully resume their purchases. Nonetheless, the glove market traditionally rebounds after each epidemic or pandemic, albeit with an adjustment period. As the founder noted, while the company’s leadership position may be challenged, it will remain relevant in the industry. Hartalega remains a resilient and stable company, but its competitive advantage has slightly diminished as competitors catch up in terms of technology.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »