Mapletree Pan Asia Commercial Trust (MPACT) was formed following the merger of Mapletree Commercial Trust (MCT) and Mapletree North Asia Commercial Trust (MNACT) in 2022. MPACT operates as a REIT that owns a portfolio of 18 commercial properties across Singapore, Hong Kong, China, Japan, and South Korea. As of 31 March 2023, MPACT is among the top 10 REITs in Asia by market capitalisation at S$9,431 million, with a total property portfolio valued of S$16,576 million.

I was curious about MPACT’s post-merger performance and the management outlook to overcome the current uncertain macroeconomic environment. To learn more, I attended its annual general meeting.

Here are the eight things that I learned from the 2023 Mapletree Pan Asia Commercial Trust AGM.

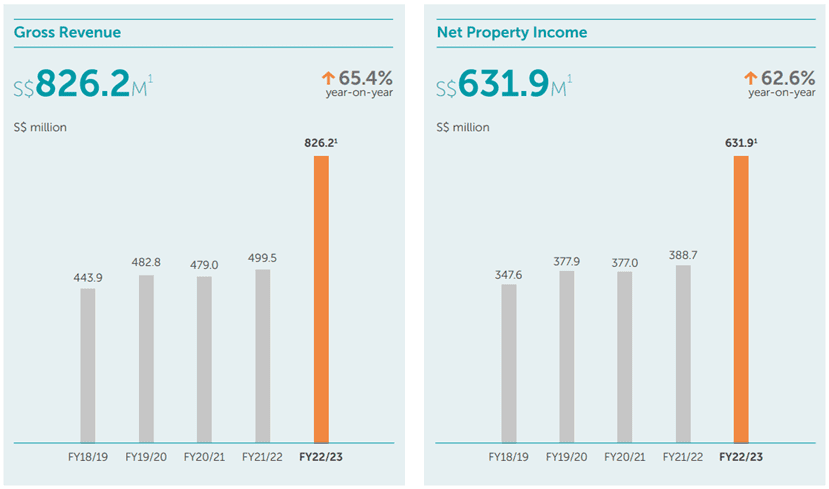

1. Gross revenue grew 65.4% year-on-year (y-o-y) to S$826.2 million and net property income (NPI) increased 62.6% y-o-y to S$631.9 million in FY22/23. This outstanding growth was primarily driven by the contribution from properties acquired through the merger, as well as higher revenues from MPACT’s core assets – VivoCity and Mapletree Business City (MBC).

VivoCity and MBC generated a combined S$445.8 in gross revenue and S$345.9 million in NPI in FY22/23, up 11.5% and 11.3% y-o-y respectively. This growth in revenues attributed to its core assets helped to reduce the impact of increases in utility and financing expenses.

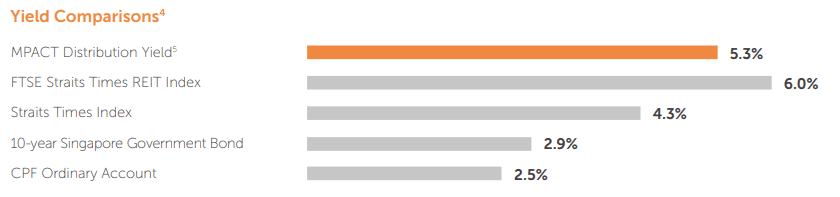

2. Distributable income grew 40.6% y-o-y to S$445.6 million and distribution per unit (DPU) grew 6.1% y-o-y to 9.61 cents. As of 31 March 2023, MPACT’s yield is 5.3%, behind the FTSE Straits Times REIT index of 6.0%.

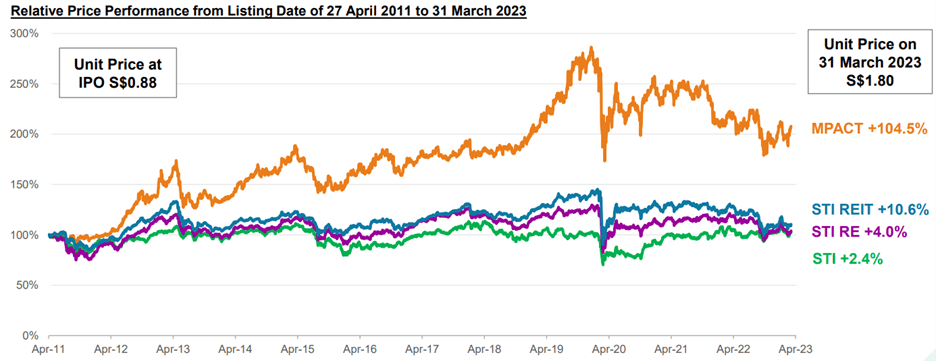

However, since its listing, unitholders would have enjoyed a capital appreciation of 104.5% and total distribution of 112.1%, amounting to a total return of 216.7%.

To get the latest yield for MPACT and other Singapore REITs, you can check out Singapore REIT data.

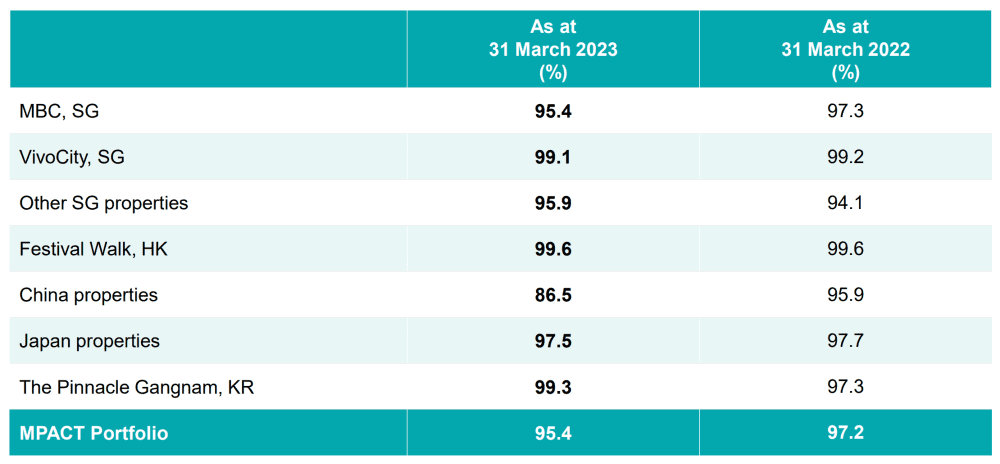

3. MPACT’s overall portfolio occupancy decreased from 97.2% in 2022 to 95.4% in 2023. Refer below for the detailed breakdown.

The decline in overall occupancy levels were primarily due to MPACT’s China properties that decreased 9.4 percentage points. Despite China’s reopening in 2023, COVID-19 outbreaks following the lifting of restrictions, weaker domestic demand, and a delay in leasing activities all contributed to the mediocre performance. That said, China’s stimulus policies such as interest rate cuts should support leasing activities moving forward.

4. MPACT’s gearing ratio is at 40.9% as of 31 March 2023, up 7.4 percentage points from a year ago. Total debt outstanding increased by 130.3% to S$6,940.8 million, with 75.5% of borrowings hedged at fixed rates. The weighted average cost of debt is 2.68% and the average term to maturity is 3.0 years.

The management stated that the gearing ratio will remain around the 40% range. Despite unitholders’ worries of the high gearing ratio and risks involved, CEO Sharon Lim reassured that it is at a comfortable range and has a healthy margin to the regulatory limit of 50%. Currently, MPACT does not experience any issues gathering loans from banks and remains in a highly liquid position.

5. In light of the current high interest rate environment, a unitholder was curious about MPACT’s cost of debt for all five markets it operates in. Janica Tan, CFO of MPACT, shared that the REIT recently issued S$150 million in senior green notes at 4.25% for seven years. As for borrowings from banks, unitholders can expect wider margins. While MPACT’s rating has improved after its merger, the overall hikes in interest rates have resulted in a 10 to 20 basis point increase in its cost of debt.

6. A unitholder asked about MPACT’s plans to acquire quality Singapore-based assets to achieve greater DPU growth. Samual Tsien, Chairman of MPACT, mentioned that the opportunities are limited in Singapore. While MPACT will constantly look out for possible acquisitions, the current focus remains on expansion beyond the local market.

One example is China. As a huge market, its long-term prospects remain compelling. China’s continued commitment to rebalance the economy by growing domestic demand through stimulus policies and capabilities can be expected to benefit long-term sustainability. For now, unitholders can expect MPACT’s future growth to be derived from markets outside of Singapore.

7. Following the previous question, another unitholder asked about MPACT’s plans to acquire big properties (that are similar to its core assets – VivoCity, MBC, Festival Walk) in other markets amidst the current high inflationary environment. Lim emphasised that MPACT’s focus remains on office or office-like assets. Currently, the management will refrain from acquiring retail properties as retail management is human intensive and requires in-depth skill and ground knowledge. That said, if the retail property is part of an office development, MPACT will take it into consideration.

In terms of geographical focus, MPACT will remain in the five key markets that it has a foothold in. The management acknowledges the considerable risk involved when venturing into a new market and discourages such action just for a single asset.

The fifth perspective

Since its listing, MPACT’s performance has outperformed the broader market index and grown significantly. MPACT’s China exposure poses key challenges that have been consistent for all REITs with allocation in that geography. However, because of China’s prospects and large market influence, it remains as an attractive long-term play. That said, in the current high interest rate environment, investors should expect a slowdown in acquisition activities which will serve as temporary headwinds for the REIT.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »