Operating commercially in Malaysia since 1912, Nestlé (Malaysia) Berhad celebrated 110 years in the country in 2022. The food and beverage manufacturer owns a wide variety of well-established household brands ranging from MILO and MAGGI to NESCAFÉ and KIT KAT. As a consumer staple stock that permeates almost every aspect of Malaysian lives with its brands, Nestlé Malaysia continued to deliver a solid set of financial results in 2022.

Here are seven things I learned from the 2023 Nestlé Malaysia AGM and EGM.

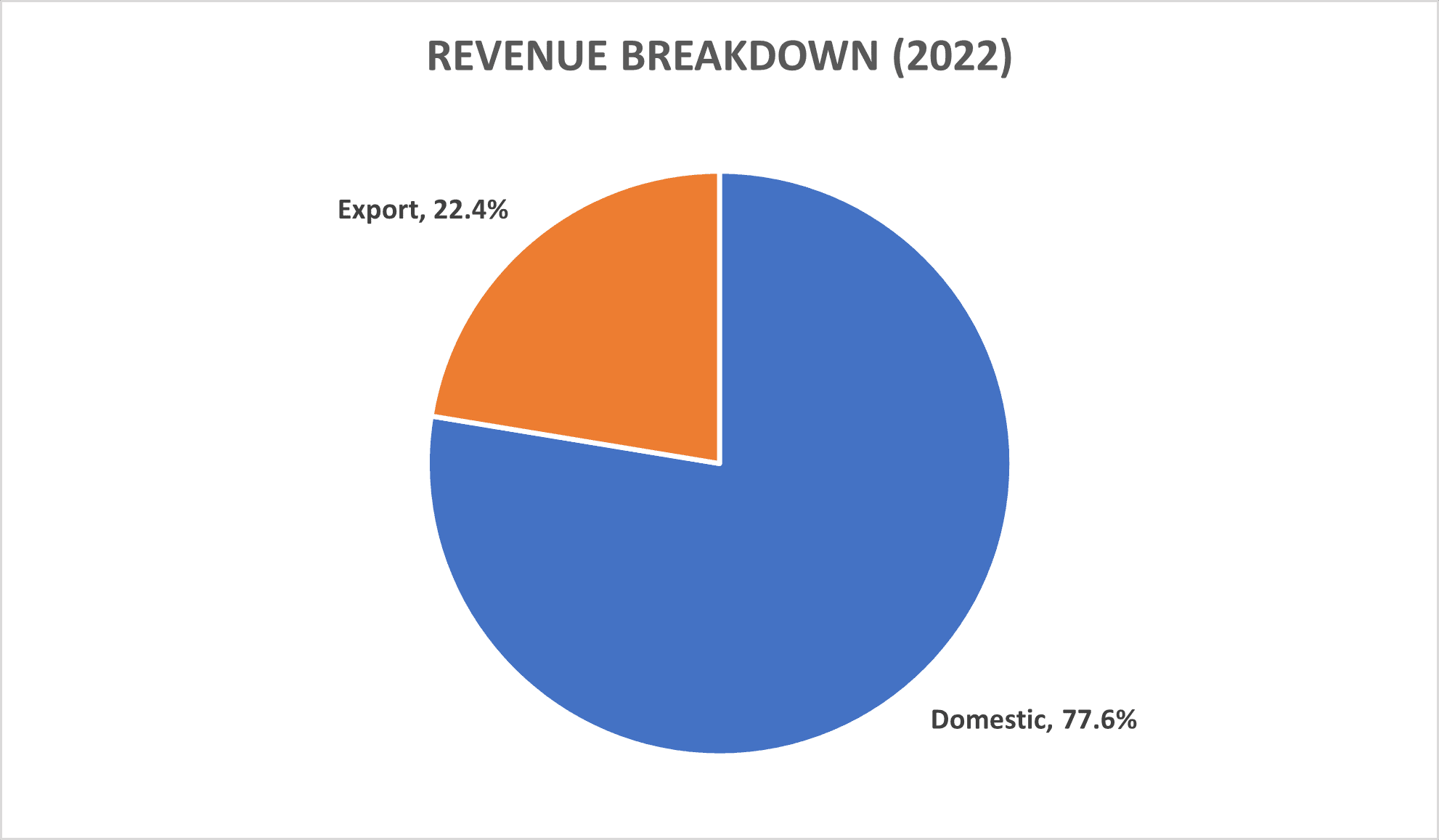

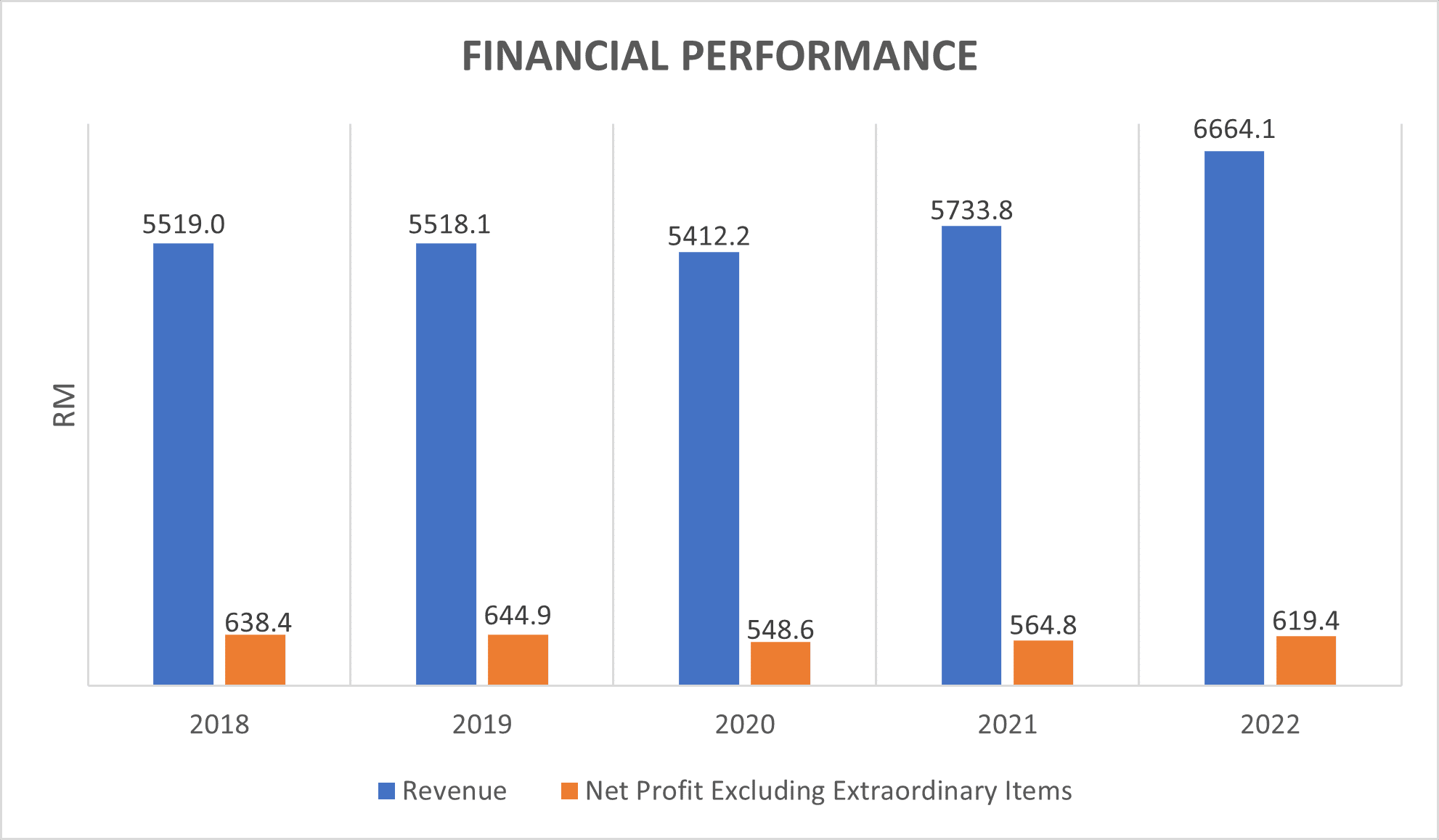

1. Revenue increased 16.2% year-on-year to RM6.7 billion in 2022, due to 12.9% and 29.3% growth in its domestic and the export business respectively. Nestlé Malaysia also recently increased their product pricing, although there will not be any price hikes for the rest of 2023.

Net profit excluding extraordinary items increased 9.7% year-on-year to RM619.4 million, but was offset by high commodity prices, unfavourable foreign exchange, and the one-off prosperity tax.

2. Although revenue stood at a five-year high in 2022, net profit excluding extraordinary items and dividend per share have not rebounded to pre-pandemic levels. This is due to the points mentioned above and further compounded by geopolitical tensions, supply chain disruptions, and the inflationary environment.

Dividend per share improved 8.3% from RM2.42 in 2021 to RM2.62 in 2022. About one-fifth of the company’s revenue in 2022 mainly came from exporting to Nestlé companies in Singapore and the U.S as well as approximately 50 other countries.

| Year | 2018 | 2019 | 2020 | 2021 | 2022 |

| Dividend per share | RM2.80 | RM2.80 | RM2.32 | RM2.42 | RM2.62 |

3. The CEO shared that Harvest Gourmet was the leader in the plant-based space in 2022. The brand started off on a solid footing and is poised to benefit from consumers who seek meatless alternatives. In my opinion, this segment is still in a nascent phase and there is not much hype about plant-based food in Malaysia. Investors should not bank on this solely to invest in the company.

4. A shareholder highlighted that the company’s total loans and borrowings doubled from RM345.7 million in 2021 to RM786.9 million in 2022. CFO Syed Saiful Islam explained that additional debt was drawn down to shore up the company’s inventory amid supply chain disruptions and for capital expenditure. The company has set aside RM1 billion as capital expenditure over the next few years to capture opportunities in Malaysia and Asia. The debt level is expected to drop in 2023.

5. In 2022, Nestlé Malaysia demonstrated its commitment to the Malaysian market by investing RM312.2 million in capital expenditure and further establishing its presence. While many global companies were grappling with downsizing, layoffs, and hiring freezes, Nestlé Malaysia took a different approach by expanding its Batu Tiga MAGGI and Chembong Ice Cream factories. This strategic move not only reinforced its foothold in Malaysia but also showcased the company’s dedication to growth and investment in the region.

6. Nestlé Malaysia commands the largest market share among fast-moving consumer goods companies as well as food and beverage players in Malaysia. Based on the CEO’s response to a shareholder’s question, it appears highly unlikely that Nestlé Malaysia will adopt a strategy of price cuts in order to gain a larger market share compared to its competitors. Implementing price cuts for the purpose of gaining market share is not conducive to the long-term interests of shareholders. As a market leader, Nestlé Malaysia does not position itself as a low-cost producer.

7. The company will spend RM165.0 million using internal funds to acquire Wyeth Nutrition (Malaysia) Sdn. Bhd. from Wyeth (Hong Kong) Holding Company Limited. The latter is a wholly-owned subsidiary of Nestlé SA.Wyeth Malaysia trades and distributes nutritional products that are targeted for young children, pregnant and lactating mothers, as well as the elderly. Brands carried by this company include S-26, ASCENDA, PROMAMA and ENERCAL PLUS.

Wyeth Malaysia is a player in the fast-growing premium infant milk segment that is complementary and synergistic to Nestlé Malaysia existing mainstream portfolio. The acquisition will boost Nestlé Malaysia’s market share in the infant milk category from 10.0% to 19.5% in Malaysia (trailing leader Dutch Lady Malaysia at 23%). The transaction is also expected to be accretive to Nestlé Malaysia’s earnings per share — from 265 sen to 271 sen pro forma.

Considering the compound annual growth rate of Wyeth Malaysia at 6.1% between 2018 and 2022, the valuation of 9.7 times earnings is considered favorable and reasonable. Executive director Tengku Ida Adura Tengku Ismail responded to Minority Shareholder Watch Group that it would take Nestlé Malaysia 10 years to recover this initial investment amount based on Wyeth Malaysia’ 2022 net profit. The recovery period should be shorter as Wyeth Malaysia’s business continues to grow.

The fifth perspective

Nestlé Malaysia is expected to experience a more favorable year in 2023, primarily due to a decline in commodity prices. Although consumers’ spending power may still be impacted by the prevailing inflationary environment and rising interest rates, the company’s out-of-home sector, encompassing restaurants and hotels, is steadily recovering. Furthermore, the in-home consumption of Nestlé Malaysia’s products remains strong. The company remains a solid dividend stock for income investors.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »