Top Glove is the world’s largest glove manufacturer. Founded in 1991, the company has grown from a single production line and 100 employees to 812 production lines and 15,000 employees.

Top Glove was recently removed from the FTSE Bursa Malaysia KLCI in December 2022 as it lost 92% of its market capitalisation. The glove manufacturer was one of the few companies to benefit from the pandemic. But post-pandemic, its share price has fallen from an all-time high at RM9.60 in October 2020 to RM0.86 in January 2023. Is Top Glove still a viable investment today following its crash? I attend its recent annual general meeting to learn more about the company’s plans moving forward.

Here are the 10 things I learned from the 2023 Top Glove’s AGM.

1. FY2022 revenue and net profit fell 66% and 97% year-on-year to RM6 billion and RM226 million respectively as sales volume and the average selling prices (ASPs) of gloves dropped 25% and 59% respectively over the same period. The net profit in FY2022 is less than pre-pandemic levels. Top Glove also recorded a net loss of RM168 million in Q1 FY2023 compared to a net profit of RM186 million in the previous corresponding quarter due to a 48% drop in sales volume as glove demand continues to soften.

2. Glove demand and supply are undergoing a ‘normalisation’ phase. This is due to existing customers still depleting excessive stock purchased during the pandemic. Customers are also adopting a wait-and-see approach in anticipation of a further drop in ASPs. The current glove ASPs for both nitrile and latex gloves are in the range of U$17 to US$22 per 1,000 pieces. Chairman Tan Sri Dr Lim Wee-Chai said that this is near the bottom level for the past 30 years. The glove oversupply issue will also ease as glove manufacturers lower their existing factory utilisation rates, decommission inefficient factories, and/or exit the industry altogether.

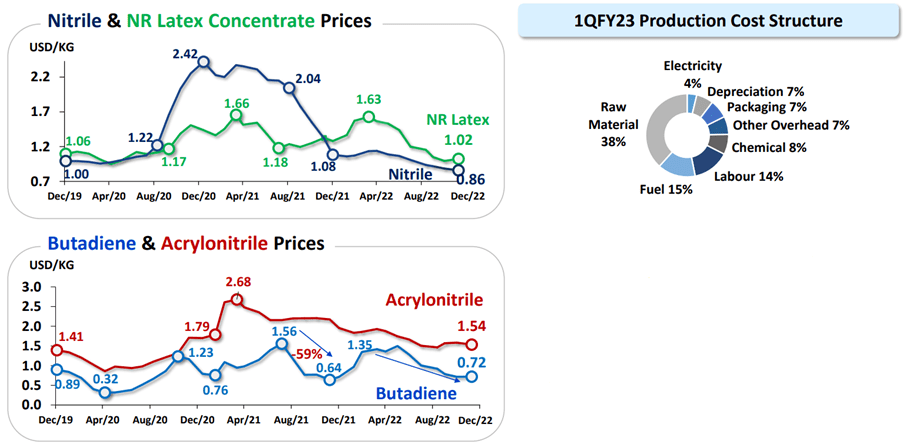

3. The glove industry is heavily affected by external factors (demand and supply) more than internal ones (production costs). Raw material price for nitrile and latex have been falling since Q3 2022.

However, global disruptions have caused natural gas tariffs to increase by 60% in FY2022, and the tariffs are expected to increase further by about 15% this year. Inflation has also raised cost of packaging materials and chemicals. Malaysian glovemakers are also impacted by the implementation of the RM1,500 minimum wage policy as of May 2022. Top Glove’s production costs were also made worse by its low factory utilisation rate of 30%.

4. Considering the oversupply in the market, the management decided to cease further capacity expansion at least until December 2023. Top Glove’s maximum capacity remains at 100 billion pieces annually. The company is also rationalising costs by temporarily shutting down 14 factories due to their low utilization rate which will help reduce maintenance CAPEX. Top Glove has also decommissioned some old and inefficient production lines.

5. Top Glove suffered a RM229 million impairment in inventory in FY2022, as the purchase cost was substantially higher than the fair market price. Moving forward, the management believes that ASPs are currently stable, and the company is unlikely to record significant impairment or write down of inventory in the upcoming quarters.

6. The industry will remain challenging in the short term, but optimistic in the long term. Top Glove will continue to see low demand from customers as they deplete their existing stock in the next two quarter. In the long run, the fundamentals are intact and demand for disposable gloves, especially in the medical field, will remain strong.

7. Top Glove’s dividend per share adjusted lower by 98% from FY2021 to FY2022. In fact, this is lower than the dividend per share in FY2019. The dividend payout ratio also fell below their policy rate of 50%, although the management reiterated that they would continue to aim for a 50% payout ratio in upcoming financial years.

| FY2019 | FY2020 | FY2021 | FY2022 | |

|---|---|---|---|---|

| Dividend per share | 2.5 sen | 11.8 sen | 65.1 sen | 1.2 sen |

| Dividend payout ratio | 53% | 55% | 68% | 43% |

8. Minority Shareholder Watch Group (MSWG) pointed out that Top Glove raised the ASPs of gloves by 5% in October 2022 despite fierce competition from competitors in China. Lim replied that the move was necessary to signal to its customers that indefinite downward revision of ASPs is not sustainable and glove manufacturers have to eventually pass on cost increases.

9. MSWG highlighted that Top Glove was in a weaker cash position compared to peers like Hartalega and Kossan Rubber in terms of cash and debt positions. Managing director Lim Cheong Guan reassured shareholders that the situation will only be temporary.

| Cash and cash equivalents | Debt | |

|---|---|---|

| Top Glove (Nov 2022) | RM742 million | RM1.6 billion (including perpetual sukuk) |

| Hartalega (Sep 2022) | RM2.0 billion | RM210 million |

| Kossan Rubber (Sep 2022) | RM2.0 billion | RM129 million |

The company will navigate the situation via several initiatives to conserve cash and improve operational efficiency including the deferment of capacity expansion plans. The management will also consider disposing of idle land not suitable for the company’s expansion. Bank facilities are also readily available.

10. MSWG noted that Top Glove spent RM1.4 billion to buy back approximately 200 million shares at an average price of RM7.11 per share in 2020 and 2021. In comparison, the management would just need RM164 million instead to purchase the same number of shares in January 2023 as the company’s share price nosedived to RM0.82. The RM1.2 billion difference can partly explain the cash situation Top Glove is in compared to its peers.

Prior to the pandemic, Top Glove’s average total annual dividend payout between 2017 and 2019 was RM197 million. The cash used for the buybacks could have been used to reward shareholders with a handsome dividend for seven years! Unfortunately, when the company’s share price was hovering near its peak, Lim once thought the share buyback was ‘a good recommendation’.

The chairman however, admitted its mistake: ‘In business, there will also be decisions made which do not generate the desired result, such as the aforementioned share buyback. We acknowledge and have learned from this; and will move forward strongly to continue creating positive stakeholder value.’

The fifth perspective

Top Glove commands of 26% of the world’s glove market share which gives them an advantage as a price maker within the industry due to their economies of scale. Glove manufacturers who have strong foundations will survive the current headwinds and rebound when the industry recovers.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »