Listed in Singapore, Frasers Logistics & Commercial Trust (FLCT) owns 107 properties across five developed markets: Australia, Germany, Singapore, the United Kingdom, and the Netherlands. FLCT primarily owns freehold logistics and industrial properties, alongside commercial properties situated within central business districts, business parks, and suburban areas. It is one of the top 10 largest REITs in Singapore.

Here are seven things I learned from the 2024 FLCT annual general meeting.

1. Revenue and adjusted net property income decreased 6.5% and 9.0% respectively to S$420.8 million and S$311.4 million respectively in FY2023 as the Australian dollar weakened against the Singapore dollar. Further, certain commercial assets in the United Kingdom and Australia recorded lower average occupancies. FLCT was also hit by higher energy and utility expenses as well as higher finance costs because of increasing interest rates and additional borrowings drawn down to finance capital expenditure and fund-through developments.

Likewise, distribution per unit (DPU) declined 7.6% year-on-year from 7.62 cents in FY2022 to 7.04 cents in FY2023.

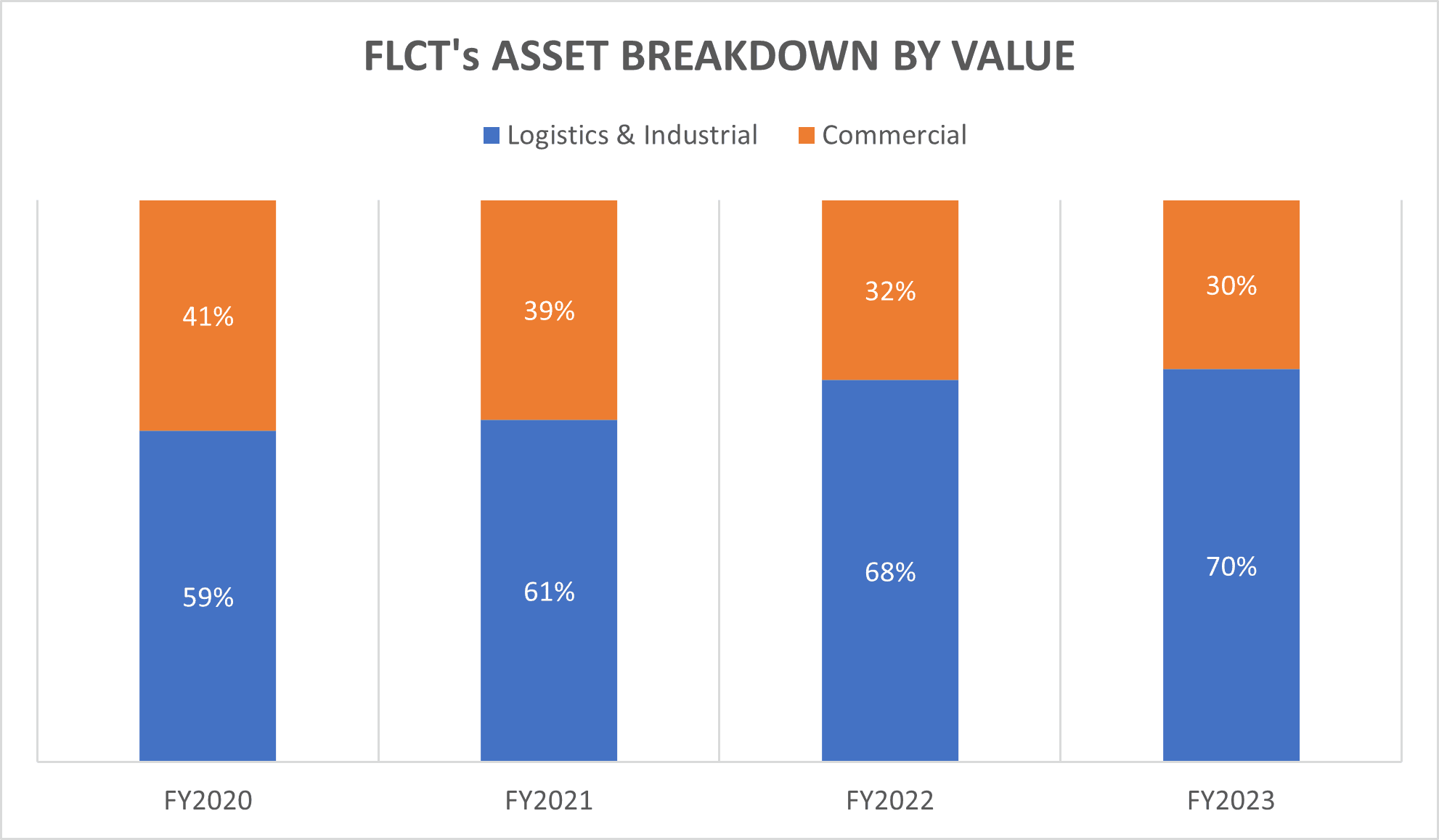

2. Its logistics and industrial assets are FLCT’s prime assets and make up of 69.6% of its portfolio. These assets have been fully occupied for four consecutive years and have a longer weighted average lease expiry (WALE) than commercial assets. CEO Anthea Lee stated that FLCT’s portfolio allocation to high-quality logistics and industrial properties will rise from its current 70% to 85% in the long term.

| Portfolio | Logistics and Industrial | Commercial | Overall |

| Number of properties | 99 | 8 | 107 |

| Portfolio value* | S$4.5 billion | S$2.0 billion | S$6.4 billion |

| Occupancy | 100.0% | 89.9% | 96.0% |

| WALE | 5.1 years | 3.1 years | 4.3 years |

3. FLCT can acquire logistics and industrial assets from FLCT’s sponsor, Frasers Property, or through off-market third-party transactions in its existing markets. The management is also exploring Japan where there is a good spread between the country’s capitalisation rate and low borrowing costs. The CEO added that they will explore leasehold assets in Singapore with reasonably long leases because of the tax transparency advantages in the country. Additionally, data centres are also under consideration as they fall under the category of industrial assets. It’s noteworthy that Lee was formerly the CEO of Keppel DC REIT, which owns data centres in Asia-Pacific and Europe.

New acquisitions will be financed through debt rather than equity. As of FY2023, FLCT’s gearing ratio was at 30.2%, indicating that a debt headroom of S$1.1 billion before reaching the 40.0% threshold. More than three quarters of our borrowings are secured at fixed interest rates.

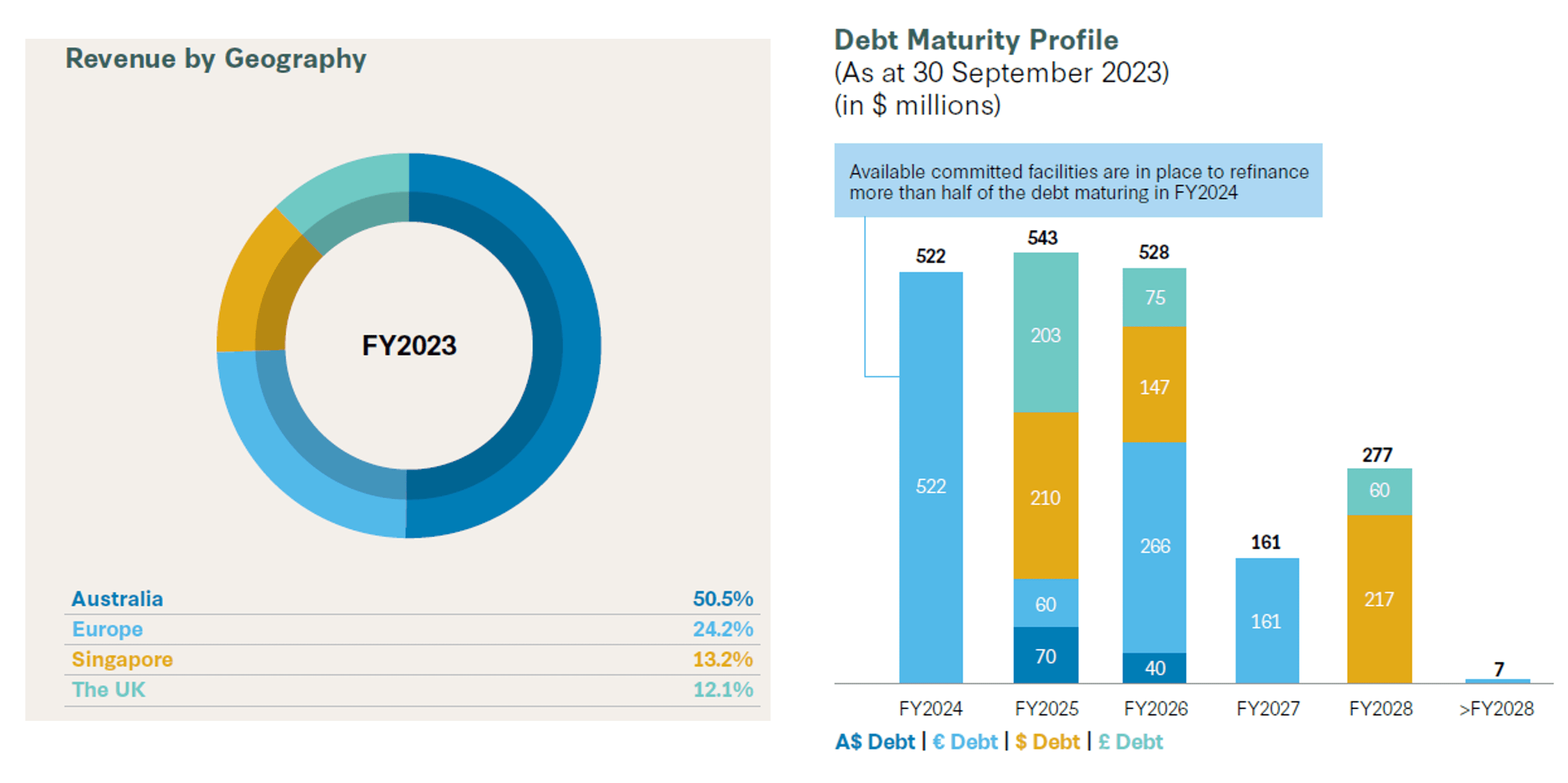

4. A unitholder pointed out that debt denominated in Australian dollars made up of 5.4% of total debt although assets from Australia contributed to 50.5% of the REIT’s revenue. Lee explained that the discrepancy occurred after the management used a substantial part of the proceeds from the divestment of Cross Street Exchange to pare down its debt denominated in Australian dollars since it bore the highest interest rate at that time. The remaining proceeds of the divestment mentioned were used to fund the acquisitions in the United Kingdom and Australia and distributed to unitholders capital gains.

The CEO explained that borrowings will be structured to match revenue contributions in their respective currencies to establish a natural hedge over time. The rebalancing will be done through acquisitions and divestments without affecting the DPU.

5. A unitholder was concerned about the 10.0% year-on-year decline in FLCT’s NAV from S$1.30 in FY2022 to S$1.17 in FY2023. He was also worried about the REIT’s planned increased exposure in the logistics and industrial assets in the United Kingdom and Australia, particularly considering the decreased assessed values of specific commercial properties in these countries from their original acquisition prices. CFO Tricia Yeo explained that the decrease in property values can be attributed to increasing interest rates in both countries, along with declining occupancy rates and expanding capitalization rates. Fundamentally, rental growth and optimising occupancy rates is key to maintaining asset valuations over the long term.

6. A unitholder observed that loans amounting to S$522.8 million are set to expire in FY2024 (second half). Yeo replied that the debt will likely be refinanced at higher interest rates with existing loan facilities in place. The expiring loans were initially secured four to five years ago at lower interest rates. As a result, there is a potential for FLCT’s total cost of borrowings to increase from 2.2% in FY2023 to slightly below 3% in FY2024.

7. In FY2023, positive rental reversions stood at 7.8% and were primarily contributed by the strong performance of assets in Australia. The CEO highlighted that industrial assets require large tracts of land but do not generate a lot of jobs comparatively. As a result, governments generally do not allocate large amounts of land for logistics assets which created the current pent-up demand until supply catches up.

The fifth perspective

Logistics assets will continue to maintain their relevance as companies aim to bolster the resilience of their supply chains and bring them onshore in response to geopolitical tensions. Companies are also seeking to establish logistics facilities closer to their customer bases to enhance cost efficiency and better manage potential supply chain disruptions. Furthermore, the growing e-commerce industry is expected to drive an increase in warehouse transactions.

Meanwhile, interest rates are stabilising and could potentially come down in 2024. The contributions from FLCT’s acquisitions in FY2023 and Q1 FY2024 will also be reflected in the coming years. FLCT’s foreign exchange risk could persist due to the weakening of the Australian dollar against the Singapore dollar given that the majority of FLCT’s assets are in Australia.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »