Singapore Press Holdings (SPH) is Singapore’s oldest newspaper and media organization that holds a monopoly in the country. In our current era, technological disruption is inevitable: SPH’s most recent nine-month financial results further prove the challenges the company is facing when they reported an 8.4% decrease in revenue and a 31.9% decrease in profit.

Investors can expect SPH to continue to face disruption in its industry moving forward. The good news is SPH noticed the trend years ago and made the move to diversify its business early. However, I personally think the speed of disruption was faster than expected and has caught SPH off guard.

In this article, I want to talk about Singapore Press Holdings’ challenges in the years ahead and its implications on the company:

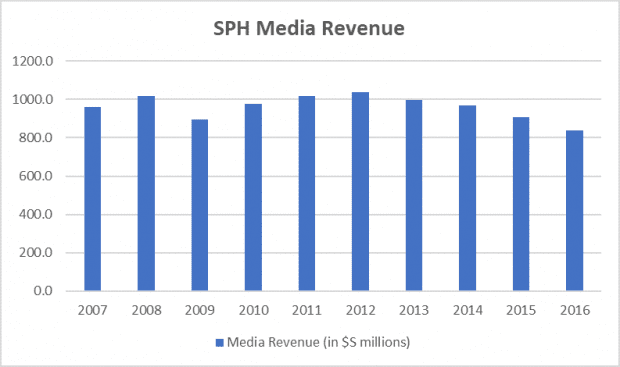

1. SPH’s media revenue is decreasing

Media business segment revenue decreased from a high of S$1,036.4 million in 2012 to S$839 million in 2016. SPH’s latest nine-month financial results shows that media revenue has again decreased by 12.3%. In recent years, the rise of digital advertising has negatively impacted SPH’s newspaper advertising business. I expect this trend to grow and affect its business moving forward.

I am not trying to be pessimistic here but allow me to share my point of view. If you want to advertise in the newspapers, a small black and white advertisement in the corner of one page can cost you about S$2,000-S$3,000. Needless to say, a half or full-page advertisement will set you back a substantial five-figure sum.

Next, people who read the newspaper can come from all walks of life who may not necessarily be your ideal target market. This means you’re probably wasting a large amount of money on showing your advertisement to consumers who have no interest in what you have to offer.

Compare this to digital advertising giants like Facebook. Since its founding in 2004, Facebook is now the world’s largest social network with over two billion monthly active users globally. The huge numbers alone don’t mean much; what’s more important is that Facebook allows advertisers to specifically target consumers based on their age, demographic, location, interests, likes, and behaviour. This means companies can spend less money by only targeting their advertisements to the consumers they want. Based on this alone, it makes business sense for companies to shift their advertising budget away from traditional media like newspapers to digital media like Facebook.

2. SPH is diversifying its business

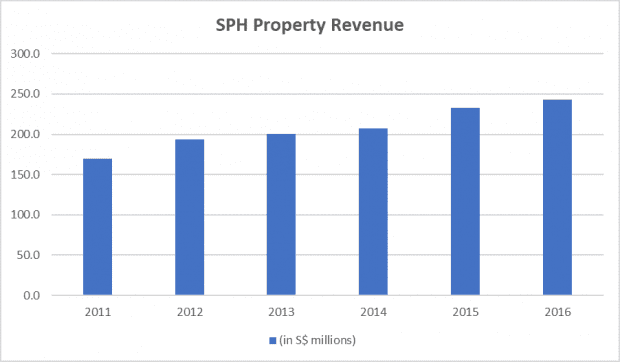

SPH is aware of the disruption it faces and has diversified into property, nursing homes, investments, and e-commerce. Out of all this, I believe property has been its most successful venture so far.

SPH has been receiving good rental income from properties like Paragon, Clementi Mall (through its stake in SPH REIT), and Seletar Mall. In 2016, SPH’s total profit before tax comprised 46.2% from its property segment and 45.2% from its media segment, even though the revenue contribution from the property and media segments were 21.5% and 74.0% respectively. Based on the direction SPH is moving, I will not be surprised if it becomes a pure property and investment player one day.

3. Dividend per share is decreasing

| (in S$ millions) | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|---|---|---|---|

| Recurring earnings | 427.1 | 501.7 | 497.0 | 539.1 | 409.0 | 410.2 | 369.3 | 349.0 | 353.5 | 305.2 |

| Dividends | 418.6 | 434.2 | 403.1 | 435.8 | 388.3 | 388.7 | 649.1 | 341.0 | 324.6 | 291.9 |

| Dividend payout ratio (%) | 98.0 | 86.5 | 81.1 | 80.8 | 94.9 | 94.8 | 175.8 | 97.7 | 91.8 | 95.6 |

SPH dividend payout ratio based on recurring earnings.

Dividend has decreased from S$418.6 million in 2007 to S$291.9 million in 2016. From my past visits to Singapore Press Holdings’ AGMs, I understand that SPH will pay a dividend based on its recurring earnings. If you look at the table above, SPH’s recurring earnings have decreased from S$427.1 million in 2007 to S$305.2 million in 2016.

SPH’s latest nine-month results report that profit decreased by 31.9%. Therefore, there is a high probability that the dividend will decrease again. Based on this trend, SPH may no longer be a good dividend stock as downward pressure on its recurring earnings is expected to continue since 45.2% of its PBT still comes from the ailing media segment. If I were to invest in SPH as a dividend play, I would wait until its property segment contributes a larger percentage of total profit to buffer any downside.

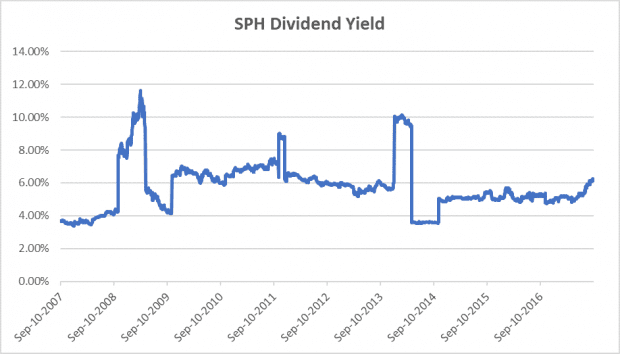

4. Looking for a sustainable dividend

The chart above shows the 10-year dividend yield of SPH. With SPH’s share price at S$2.57 (as at 12 September 2017) and its FY2016 dividend per share at 18 cents, this reflects a dividend yield of 7.0%.

New investors will probably note the attractive yield as it much higher than our bank interest rates. However, we know that SPH’s earnings are expected to fall further which means its dividend will probably fall as well. Hence, this 7.0% yield may be an illusion.

Every investment is a good one — as long as you pay for it at the right price.

We all know that SPH’s media segment is facing disruption, so now we need to paint the worst-case scenario where we exclude any profit from the media segment entirely. SPH’s property segment, however, is growing nicely and its FY2016 profit before tax is S$179.4 million. If we take this amount and multiply it with SPH’s lowest dividend payout ratio of 80%, we get a dividend per share of 8.9 cents. Based on this conservative figure, you will get a dividend yield of 3.5% (based on SPH’s share price as at 12 September 2017).

At that yield, I would think twice about investing in SPH since its media segment will most probably continue to face headwinds and continue to pull SPH’s earnings and share price. Therefore, you should demand a higher yield based on the worst-case scenario to buffer against any potential price drops. Remember, investing is about protecting your downside as much as growth.

Dear Mr Victor Chng, How I wish you post this article on SPH months before the fallout. I bought two thousand shares way above $3 thinking it pays a stable dividend and even after collecting a few dividend payout, the capital loss is going to swell down the road, against a lower dividend payout down the road. I bet institutions are also unloading their holdings after reading your article. Bad luck.

Thanks Wah Siew. I don’t think my article will move or influence how the institutions view SPH.

On a separate note, before you invest in any company for dividends, you should always ask yourself if the dividend is sustainable in the long run. If it is and you are able to buy at a good valuation, most times you would have protected your downside and the upside will take care of itself.

Sir,

Your analysis is precise and void of emotion unlike so called experts and Advisors here and in the US especially.

I’m wondering if you offer a service where you access companies either in Singapore and Malaysia or ASEAN or Asia and make recommendations to clients continuously for a subscribed fee annually whereby an investor can pick and choose to invest on these recommendations at their own risk. This would be a mutually beneficial arrangement for investors who have no time to do such productive research and are willing pay for such impartial advice while still maintaining the prerogative whether or not to invest.

I have no interest to attend , participate or listen to any talks webinars etc. I have been receiving your emails on your attendances to Agms etc and your report on companies and find them significantly more informative than the thrash being churned out daily by the Writers and experts in CNBC and the bank Analysts and hedge fund managers with their vested interests in the Dow, Nasdaq and S& P ” CASINO ”

Thank you for your time.

https://fifthperson.com/memberships/

Hi Wah Siew,

A contributing factor in the recent price movements would also be that CIMB had just issued a report downgrading their target price for SPH to $2.38.

http://research.sginvestors.io/2017/09/singapore-press-holdings-sph-cimb-research-2017-09-08.html

Regardless, Victor’s summary is very helpful.

The new ceo famous of selling assets do you think he will sell/privatize it ? at rumoured $2.50 ?

Hi Chan,

I don’t think the new CEO will privatise or sell the assets at this moment.

Hi victor, I have been reading your articles.

what do you think is a good entry price /PE ratio / PB ratio for SPH to protect our downside.

Thanks

Hi Bernard,

As mentioned in my article, you can look at the sustainable dividend and make sure you demand a higher yield as one part of SPH’s business is declining.

Hi Victor, can you please ask your team to stop writing about Malaysian stocks? Malaysia may have good company but the problem is their RM. In the long run, we will be losing money.

Please write up on HK/SG stocks.

This post from back in May might also be of interest.

Finally SPH has a new CEO

http://limdershing.blogspot.sg/2017/05/finally-sph-has-new-ceo.html