A stock catalyst is a revelation or event that causes the price of stocks to move. Such events break the stock price momentum and allow investors to unlock value that the market has previously failed to realize.

In this two-part series, we will be highlighting four stocks that are positively affected by near-term catalysts.

1. Neratel – Phenomenal Gain from Divestment

Divestment Windfall for Shareholders

NeraTel announced the sale of their Point of Sale (POS) payment business for a consideration of $88.0 million to Paris-based Ingenico Group. The $88 million offer represents a 31.3x FY15 P/E valuation and accounts for 35 percent of Neratel’s market cap. While this deal is still subjected to shareholders’ approval, majority shareholder Asia Systems Ltd, which is owned by the Northstar Group, has already executed an irrevocable undertaking to vote in favour of the proposed transaction.

The deal is estimated to give Neratel a gain of $71.5 million. The larger estimated gain will likely translate to an enormous S$0.16/share special dividend. The management has indicated its intention to pay out a significant portion of this gain to its shareholders. Market consensus expects at least 17 cents/share to be paid to shareholders as dividends from this sale alone. This is on top of the regular dividends of four cents/share, which represents a massive yield of about 29.9 percent.

This sale represents a great opportunity for Neratel shareholders to unlock value. At the same time, it will allow the company to streamline its business activities. Neratel’s capex requirements and depreciation expenses would also likely decline after the sale of the business. This would be a positive for the company.

Focus On Neratel’s Core

Moving forward, NeraTel’s management is confident that given time, its remaining network solutions business will grow to fill the earnings gap left by the POS business. .

On the orderbook front, Neratel managed to continue delivering strong order wins and secured approximately $70.2 million in 1Q16. This represents a 21.9 percent year-on-year increase. Neratel’s current order backlog value exceeds 2015’s revenue as a whole. This implies that the current orderbook is worth more than $180 million, which should provide solid revenue visibility over the next year.

The disposal of the POS payment business will also enable management to focus their efforts on NeraTel’s core network solutions business.

2. CapitaLand Commercial Trust – CapitaGreen Deal Reasonable and DPU Accretive

CapitaLand Commercial Trust (CCT) has exercised its call on its remaining 60 percent interest in CapitaGreen. CapitaGreen is currently held by MSO Trust, which in turn is jointly owned by CapitaLand (50 percent interest), CCT (40 percent) and Mitsubishi Estate Asia (10 percent). Upon completion of the acquisition (around Nov 16), CCT would hold 100 percent of CapitaGreen through the MSO Trust.

CapitaGreen is a Grade A premium office with net liquid assets of c.703,000 square feet. It is located on the site of former Market Street Car Park, in the heart of Singapore’s central business district (CBD).

Key Conditions for the Deal

Two key conditions have to be met in order for CCT to exercise the call: (i) the market valuation must be equal to or above the hurdle price of $1,585.5 million (based on actual costs incurred since development in 2011 less net income received and compounded at 6.3 percent p.a.); and (ii) subject to Unitholders’ approval.

Acquiring At a Reasonable Price

Factoring in the remaining 57-year land tenure, the agreed market value of CapitaGreen is $1,600.5 million. This translates to $2,276 per square foot and an implied cap rate of 4.15 percent, which is comparable to other Grade A buildings in CCT’s portfolio.

The management cited that it is a good time to acquire the asset as it expects CapitaGreen’s capital value to appreciate further. The acquisition will be an accretive acquisition which will provide a 1.5 percent FY17 distribution per unit (DPU) uplift, taking into account that the acquisition would be funded by bank borrowings, at an average cost of three percent. CCT’s gearing ratio is expected to remain healthy, increasing to c.38 percent upon acquisition from c.30 percent as at 31 Mar 2016.

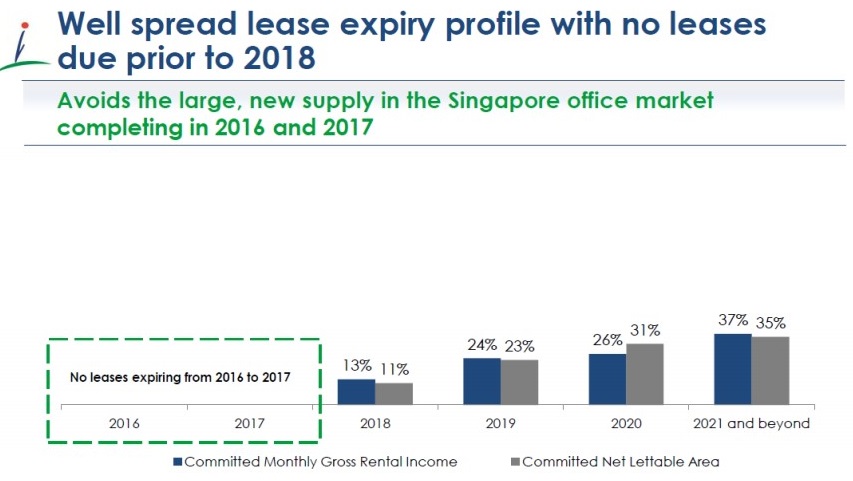

Source: CapitaLand Commercial Trust

In view of the challenging leasing environment for the next two years, CapitaGreen’s lease expiry profile is favourable as it does not have any exposure to lease expiry till 2018. Therefore, it minimises rental downside for CCT’s portfolio.

Read more: 15 things I learned from NeraTel’s FY2015 AGM