Whether you’re a fan or critic of the CPF, we all have to admit that it is a fact of life in Singapore. So why not make the most of it and maximise your CPF savings for your retirement?

While the limitation of your CPF savings is that you can only withdraw it when you reach 55 years of age, the upside is that you’re putting your money in a effectively risk-free AAA-rated investment that pays you 4% returns annually. You’d be hard-pressed to find anything like that elsewhere in the markets.

So if you’re the kind that doesn’t mind saving your money in CPF till you’re 55, then here are four ways to maximise and grow your CPF savings for retirement:

1. Transfer from Ordinary to Special Account

The CPF Ordinary Account (OA) pays you 2.5% interest annually, while your CPF Special Account (SA) pays you 4%. (CPF actually pays you extra 1% interest for the first $60,000 in your combined OA and SA balances, but we’ll exclude that here for ease of calculation.)

Knowing this, you can transfer the money in your OA to your SA to earn the extra interest. While the extra 1.5% may not seem like much, it makes a big difference when compounded over time.

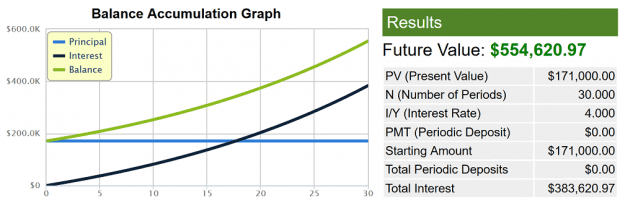

For example, let’s assume you can fund the Full Retirement Sum ($171,000 as of 2018) you’re allowed to transfer to your SA. When compounded over 30 years at 4% per annum, this comes up to $554,620.97.

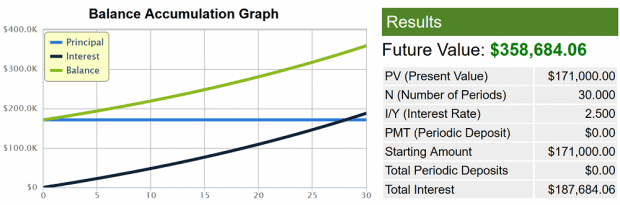

In comparison, if you left that amount in your CPF OA that earns 2.5% interest, you’d end up with $358,684.06 – nearly two hundred thousand dollars less.

So it makes sense to park your money in the SA to earn the higher interest, but what’s the catch? The catch is that you can only transfer money from your OA to SA, and not vice versa; it is a one-way trip.

So if you need the money in your OA to fund the purchase of a home in the near future, then you might want to put off doing this. But if your housing needs are comfortably taken care of, then transferring money to your SA will go a long way toward your retirement — which brings us to our next point…

2. Pay your mortgage in cash

Besides using the CPF OA to fund the 20% down-payment for a home, many Singaporeans also use it to service their monthly mortgage. But if you can afford to, there are several advantages to paying your mortgage in cash.

One advantage is that you can treat the money in your OA as an emergency fund (assuming you don’t transfer all your funds to the SA). If you end up never using the money, it will compound at 2.5% interest and buffer your retirement fund.

But if something does go wrong, you can stop servicing your mortgage with cash and switch to using your OA. This means you won’t have to worry about losing your home in the event of emergencies such as a sudden retrenchment.

The main benefit of paying your mortgage in cash though, is that it’ll allow your money to compound much further when it’s left untouched to grow in your CPF, especially in the SA.

3. Top up your Special Account

If you haven’t yet hit the Full Retirement Sum in your SA and you’d rather not transfer the money from your OA, you can still choose to contribute to your SA by making a voluntary cash top-up. Effectively, you’re using your SA like a bank savings account — albeit one that pays you 4% interest and can only withdraw from at age 55.

You also get a tax relief equivalent to your top-up amount, up to $8,000 per calendar year.

Another good tip is to make your top-up at the beginning of the year — if you top up in January each year instead of December, you’ll earn 20% more interest over 10 years.

4. Top up MediSave Account first

Now if you plan on making voluntarily cash top-ups to your SA, I’d suggest contributing to your MediSave Account (MA) first. Your MA also earns the same 4% annual interest as the SA, but with the added flexibility of being able to use it for medical care and hospitalisation expenses.

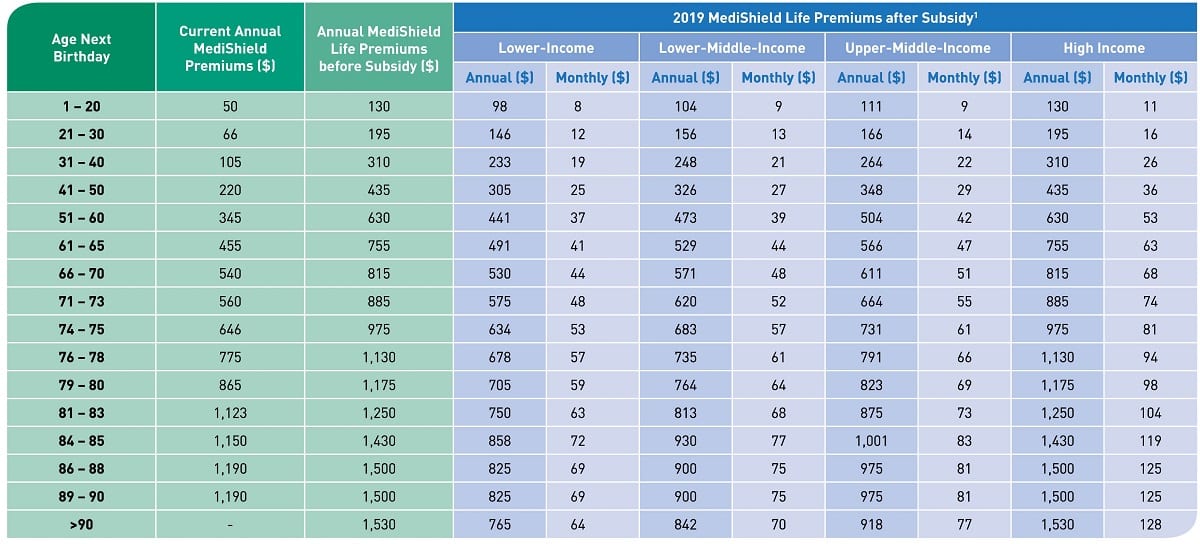

Currently, you can contribute up to the Basic Healthcare Sum of $66,000 (as of 2022). This will earn you an annual interest of $2,640 — which you can use towards paying your MediShield Life annual premiums.

As you can see, your annual interest covers even the most expensive premium for MediShield Life. (Though I doubt anyone reading this is over 90.) In essence, adequately funding your MA entitles you to ‘free’ health insurance in Singapore.

Voluntary contributions to your MA also allows you to claim a tax relief – all the more reason to make a contribution if you’re already planning to do so.

The fifth perspective

So these are the four simple things you can do right now to maximise and grow your CPF savings for retirement. As good as it sounds, remember that you always need to evaluate your personal financial situation before making any decision.

For example, voluntarily topping up your SA may be a great idea if you have excess cash that you won’t need until you’re 55, but may not work if you’re tight on finances right now and need the money for more pressing things. Just like any other financial instrument, the CPF can be a great tool to help you achieve your retirement goals if you use it right.

CPF For Retirement FAQ

Should I aim for ERS? Is it better than FRS?

This answer depends solely on the individual and their financial circumstances. It is true that reaching the Enhanced Retirement Sum (ERS) can give you a higher monthly payout from age 65. However, we prefer aiming for just the Full Retirement Sum (FRS) and keeping any excess in liquid cash, as this provides greater control over the money—i.e., the flexibility to invest in potentially better instruments such as property or stocks. After all, it is impossible to predict how long we will live and whether we will fully benefit from the ERS.

Can I withdraw my money from the OA after 55?

Yes, you have the option to withdraw all the money in your CPF Ordinary Account (OA) after age 55. Alternatively, you can keep it inside CPF to continue earning 2.5% interest (compounded), which is much higher than what most banks offer.

I read that the new CPF change says that “interest earned is not yours.” What does that mean?

It simply means that when a CPF member passes away, the interest earned on CPF LIFE premiums is not included in the amount paid out to beneficiaries. Instead, it goes back into the public pool.

So what happens to the money in my RA if I pass away before the full amount is used?

The money is still yours to pass down. Any remaining balance, after deducting what has already been paid out, will be distributed according to your will or CPF nomination. Only the interest earned during the payout phase is returned to the public pool.

Isn’t that unfair if the interest earned is not given back to us?

This is a complex issue. If you live longer than the amount set aside for the FRS/ERS, you will still continue receiving payouts. Where does this money come from? This is part of the fundamental concept behind annuity schemes, which are designed to provide regular lifetime payouts. Most importantly, any remaining principal balance will still be returned and passed down to the beneficiaries you choose.

Okay…then what’s the breakeven point for CPF Life?

Assuming you start your CPF payouts at age 65, the breakeven point (based on the 2024 FRS) is about 20–21 years. This means that if you live beyond age 85, you are essentially receiving more than what you set aside, while continuing to enjoy the same monthly payout. So stay healthy, stay happy, and try to keep fit.

What if I delay my CPF Life payout until 70? Does the interest belong to me?

You will continue earning interest until your CPF LIFE payouts begin, and that interest is yours to keep. This is also one reason you may receive a higher monthly payout. However, once payouts start, any interest earned will go back into the public pool.

Should I use my OA for properties or transfer it to my SA?

This question really depends on your individual goals and financial approach. If you plan to buy two properties, you may not want to transfer your OA to SA immediately. Instead, you can contribute to your SA and reach the FRS through cash top-ups at the end of the year. This way, you work towards meeting the FRS for guaranteed passive income after age 65, while keeping funds in your OA for property purchases.

Alternatively, you can prioritize reaching the FRS by transferring your OA to SA and letting it compound at 4%. This also removes the need to keep chasing the increasing FRS each year.

Since goals and financial circumstances vary, it ultimately comes down to personal preference.

Can I continue to invest under the CPF Investment Schemes beyond age 55?

After setting aside your FRS in your RA, you can still use your OA to invest in stocks under the CPF Investment Scheme (CPFIS). However, if you are eligible to withdraw funds from your OA, it may be more beneficial to invest using cash instead.

Do note that there is a quarterly service fee (about $2) for investing through CPFIS, whereas investing with cash does not incur this fee. So if you were to ask me, I would simply withdraw the money as cash and invest outside the CPFIS.

Hi, thanks for the great FAQ write-up. They are very useful.

May I ask if you can provide the breakeven for ERS (to complement the FSR breakeven analysis above).

Thanks!

Hi CY, you cannot contribute to the Enhanced Retirement Sum (ERS) before age 55, so the calculation is not applicable. You can only top up to the ERS after 55 in your CPF Retirement Account.