While there has been much discussion on the background of the Astrea IV bond issuance and the Class A-1 bonds available for the retail public, less discussion is available on the structural safeguards built into the bond issuance in general.

Flipping through the Astrea IV prospectus, we note that there are five key structural safeguards:

- Reserves accounts;

- Sponsor sharing;

- Maximum loan-to-value ratio;

- Liquidity facility; and

- Capital call facility

In order to have a better understanding as to how these safeguards can secure investors’ interests, let us take a deeper look at each safeguard and what they mean.

1. Reserves accounts

The reserves accounts are specially earmarked accounts which are meant to accumulate cash specifically for the purposes of redeeming the Class A-1 and Class A-2 bonds on 14 June 2023.

Explanation: Think of the reserves account as a specially designated cash account that will accumulate cash from the proceeds of the private equity funds distributed to Astrea IV. This specially designated cash account is there specifically to redeem the bonds from bondholders when the bond matures.

Where does the cash for the reserves account come from?

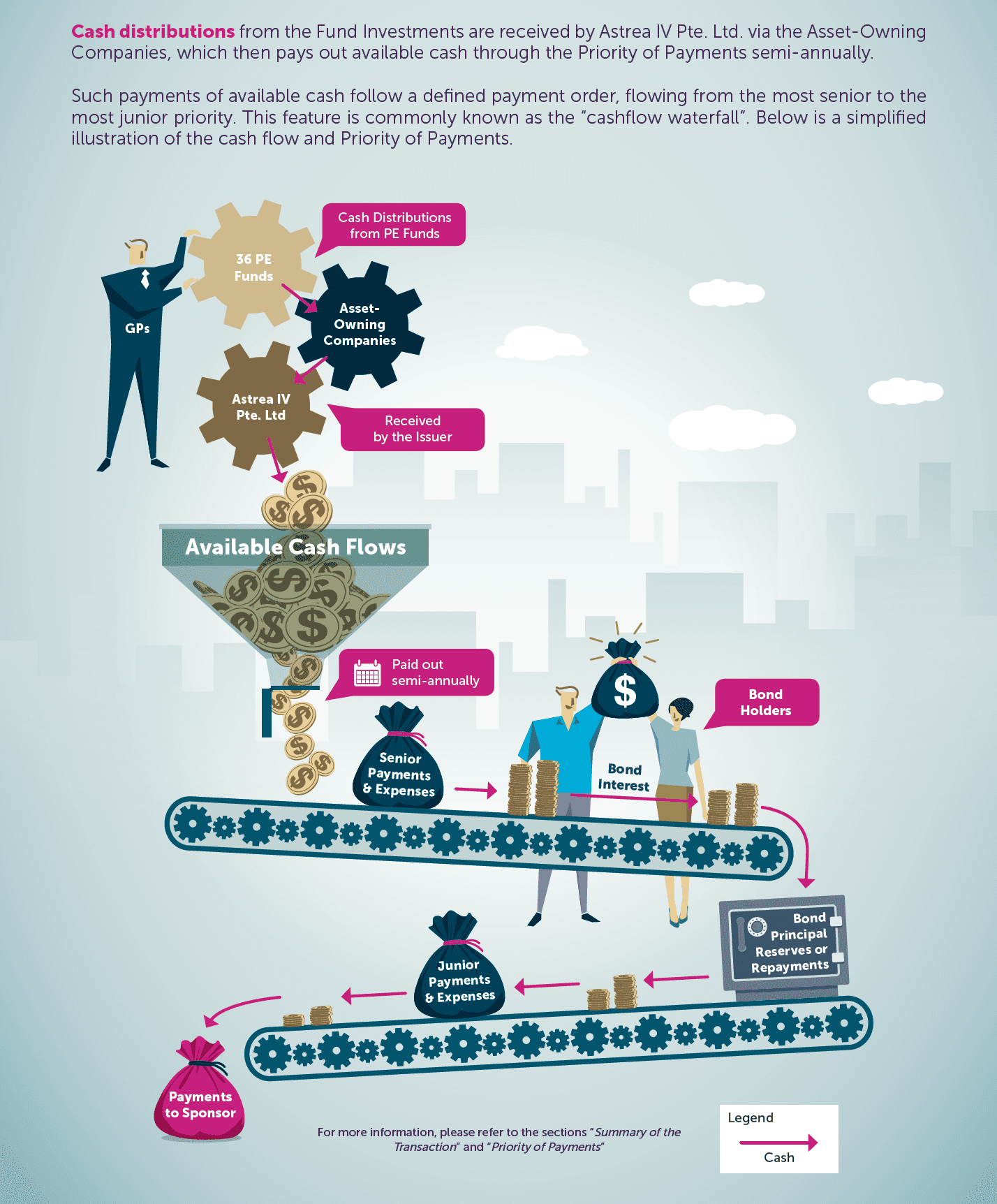

When the underlying assets of Astrea IV provides returns, usually in the form of cash distribution from the private equity (PE) funds, Astrea IV would have to redistribute these returns according to the Priority of Payment as stipulated in the prospectus.

After the payments for taxes, expenses and operations, the returns will be used to pay off the interest payment for the bonds and also to deposit some cash into the reserves account. The sum of money accumulated in the reserves account will be used to redeem the relevant bonds when they mature.

Explanation: When Astrea IV receives money from the distribution of proceeds from the private equity funds, the cash is distributed according to a ‘cashflow waterfall’. In simple terms, it just means that the cash is distributed according to different priorities as dictated by the offer document.

For example, if you were to sell your house which is still under mortgage, the bank would first collect the money owed to it and any interest still owed before you receive the remaining amount from the sale.

In this case, the interest payment for the bonds and the cash deposited in the reserves account rank near the top when any cash distributions from the private equity funds are made to Astrea IV.

2. Sponsor sharing

The sponsor sharing feature is a new feature which was not available for the Astrea III bonds issued earlier. The feature accelerates the amount deposited into the reserves account if a performance threshold is met.

If the performance threshold of US$313 million (constituting 50% of Astrea IV’s equity) is returned to the sponsor, 50% of the subsequent cash flows available to the sponsor will be diverted to the reserves account to allow an accelerated build-up of capital in the reserves account for bond redemption.

Explanation: This means that after certain KPIs are met, the sponsor will divert more cash from fund distributions to the reserves account to ensure a much higher likelihood that the bondholders are paid off at redemption.

3. Maximum loan-to-value ratio

The Astrea IV bonds have a maximum loan-to-value ratio of 50%. If the loan-to-value ratio exceeds 50%, the collateral cash flows would have to be diverted towards the reserves account until the pre-determined reserves account cap is met.

If the reserves account cap is met but the loan-to-value ratio still exceeds 50%, the remaining cash flows will be diverted to the redemption of the outstanding principal amount of the Class B bonds, until the loan-to-value ratio is brought below 50%.

Explanation: This feature ensures that the bonds issue do not become over-leveraged. In the event that it does (e.g. from a write-down of private equity funds from poor performance), certain transactions will occur such as the redemption of the Class B bonds.

The ensuing cash flow will be paid to the reserves account to ensure that retail bondholders are paid back.

4. Liquidity facility

Astrea IV has a liquidity facility in place with DBS. The liquidity facility allows Astrea IV to call on funds to pay off certain expenses (including coupon payments) in the event of a cash shortfall. This ensures that investors will be able to obtain their coupon payments even if the illiquid nature of the underlying private equity portfolio does not yield free cash flows.

Explanation: A liquidity facility is simply a line of credit that Astrea IV can tap on to pay investors in case there is a time lag in distribution of cash from the private equity funds.

Exits from private equity investments are inherently unpredictable as they depend on exiting via IPOs or selling to an external buyer. It is the same issue as selling a property – it really depends on market conditions. The lumpiness of these cash flows is mitigated as Astrea IV can simply borrow the money from DBS in the short run to pay the interest due on its bonds.

5. Capital call facility

Apart from the liquidity facility, Astrea IV also has a capital call facility in place. The capital call facility allows Astrea IV to draw down on the facility to pay for capital calls from the underlying funds if there is a shortfall in Astrea IV’s available funds. This ensures that there will be no penalties or missed opportunities for Astrea IV should there be a capital call from the underlying funds.

Explanation: Astrea IV still has capital commitments that are unfulfilled. The way that a private equity fund works is that cash is only “called for” when an investment opportunity surfaces.

In layman terms, think of it as joining a group of buyers to buy property. The money from each buyer is only required to be paid when a property is found. Until then, you do not have to put up the cash.

The same analogy applies in this case, and Astrea IV still has certain ‘capital commitments’ in the event a good opportunity surfaces and one of their private equity funds wants to deploy the cash. The capital call facility allows Astrea IV to borrow money from the bank to meet this commitment.

It’s important to note that because of this, the loan-to-value ratio may increase and thus there is the safeguard explained earlier on ‘maximum loan-to-value ratio’.

In general, the structural safeguards from Astrea IV’s bond issuance provides investors with a fair amount of protection. The reserves account structure coupled with the sponsor sharing and maximum loan-to-value features allow for timely and prompt built up of reserves to ensure that there will be funds to redeem the Class A-1 and Class A-2 bonds.

The liquidity facility and capital call facility ensures that Astrea IV will not face any issues with cash flow given the illiquid nature of the underlying private equity portfolio. These structural safeguards should provide comfort to the retail investors to invest in the bonds and not have to worry about the illiquid nature of the underlying portfolio.

Ending thoughts

It’s clear that a lot of thought was put into the structuring of the bonds, especially with regards to the structural safeguards. There a distinct lack of quality bond issues in the market. We welcome the addition of the Astrea IV bonds the investor’s portfolio. Our own opinion is that any risk of real default is small, and in light of this, the yield offered to investors far compensates them for any risk taken.

Tay Jun Hao & Terence Fong

Tay Jun Hao is the co-portfolio manager of the Heritage Global Capital Fund, a global value fund at Swiss Asia Financial Services Pte Ltd. Cumulative performance of fund strategy net fees from Jan 2012 – May 2018 is +149.13% (CAGR +15.50%).

Terence Fong practiced as a lawyer with a top-tier international law firm specializing in finance and capital market deals. He has practice experience in various jurisdictions in Europe and Asia advising on cross border transactions. He currently works with hedge funds to advise them on their capital and investment structure. He also works with venture capitalist funds to help start-ups grow and scale regionally and internationally.

Disclaimer: The authors will be subscribing in the bond issue. The above article does not constitute investment advice and simply represents the opinion of the authors.

Additional reading material: S&P Global Ratings report on Astrea IV Bonds

If the reserves account cap is met but the loan-to-value ratio still exceeds 50%, the remaining cash flows will be diverted to the redemption of the outstanding principal amount of the Class B bonds, until the loan-to-value ratio is brought below 50%.

What do you think is the reason that class B bonds should be redeemed before class A bonds in such an eventuality?

Hi John,

The main reason would be a significant write-down in the NAV of the PE funds that would decrease the value of assets (the denominator).