Ant’s IPO was set to become the largest IPO of all time. It was set to raise US$34.5 billion at a valuation of US$313 billion. The Shanghai retail offering was oversubscribed by 870 times and the Hong Kong offering 389 times, soaking up over US$3 trillion of funds. Until it was abruptly cancelled just days before the IPO day by the Chinese government. Now investors including BlackRock, GIC, and Silver Lake are left holding illiquid stakes in Ant.

The IPO halt came shortly after Ant’s founder Jack Ma gave a speech at the Bund Summit in Shanghai, where he criticized the China’s regulators and state-owned banks for stifling innovation in the industry.

‘We cannot use the way to manage a railway station to manage an airport. We cannot use yesterday’s way to manage the future,’ he declared. The audience included the Vice President of China and the governor of China’s central bank.

Days after the speech, Ma and two other executives of Ant were summoned by regulators for regulatory interviews in Beijing. Then the Shanghai and Hong Kong exchanges aborted the IPO, because ‘Ant may not be able to meet listing qualifications due to significant regulatory changes in China’s fintech industry.’

Ant and its dominance in China

Ant Group is the parent company of third-party mobile and online payment platform Alipay. Alipay is the leading digital payments provider by total payment volume and the leading digital finance platform by transaction volume in China.

Through Alipay’s reach of more than one billion users and 80 million merchants, Ant works with its partner financial institutions by leveraging its proprietary technology and data to provide financial services such as consumer credit, SMB (small & medium-sized businesses) credit, investments, and insurance. These services are provided to the consumers and small businesses who had been underserved by and largely left out of China’s financial system. Ant has created an ecosystem that consists of consumers, merchants, financial institutions, third-party service providers, and its strategic partners.

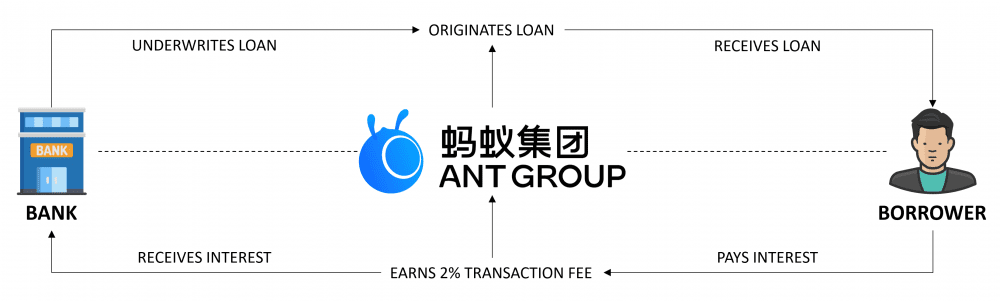

Ant’s consumer credit business

Ant’s credit/lending business (called CreditTech) is the company’s largest segment by revenue, comprising 40% of total revenue in the first half of 2020. In 2014, Ant launched Huabei (meaning ‘Just Spend’), which is a built-in virtual credit card in Alipay used for daily expenditures. In 2015, Ant launched Jiebei (‘Just Borrow’), a short-term consumer credit product for larger transactions offered to users who either have developed a credit history on Alipay or are eligible for Huabei. Ant enjoys as much as a 40% cut of loan interest.

Ant uses artificial intelligence (AI) to quickly assess an applicant’s creditworthiness. The company owns a 30% stake in MYbank (MY is short for mayi, ant in Mandarin) which pioneered the ‘3-1-0’ lending model. The 3-1-0 model offers collateral-free loans that takes less than three minutes to apply for on a mobile phone, less than one second to approve, and requires zero human intervention.

However, Ant doesn’t actually make the loans. They screen and qualify the borrowers, originate the loans, then hand them off to its partner banks. These banks take on the credit risk (i.e., the risk that some of these borrowers might default) and receives interest payments, out of which Ant charges banks a 2.08% technology service fee for each transaction. Those banks do not perform the due diligence on the loans, only relying on Ant’s AI.

According to its prospectus, as of 30 June 2020, about 98% of credit balance originated through Ant’s platform was underwritten by its partner financial institutions or securitized. Which means that Ant only records about 2% of the loans on its balance sheet, which would be more than fully offset by its technology service fee. In other words, Ant bears none of the credit risk for the loans it originates and is therefore incentivized to generate as many loans as possible to earn fees. Sounds familiar?

The 2008 subprime mortgage crisis

Following the burst of the Dotcom bubble, the U.S. Federal Reserve cut interest rates to historically low levels to stimulate the struggling American economy. As economic growth increased, demand for housing and subsequently, mortgages, rose, and home ownership increased to record levels, which made it difficult to find more new homebuyers. This led some lenders to extend mortgages to people with weak credit scores, known as subprime loans.

Investment banks wanted a piece of the action, so they bought these mortgages, repackaged them as mortgage-backed securities (a financial asset made up of a pool of mortgages), and sold them to investors. At one point, lending standards became so lax that the NINJA loan (no income, no job, no assets) was created. However, when the housing market started to crash and borrowers defaulted on the loans, the rest was history.

The subprime crisis was directly attributable to the originate-to-distribute lending model – where the originator of a loan sells it to various third parties – which experts say led to the decline in lending standards. Since the originators were not exposed to any of the risk that the mortgages might go bad, they had no incentive to make sure the loans were of appropriate quality. The risk had gone to investors who bought these loans and their payment streams. This is essentially the same as what Ant is doing with Chinese consumer credit.

How new regulations will affect Ant’s business model

The Chinese government was cognizant of the possibility of a financial crisis if Ant was allowed to list with its current business model. In the weeks before Ant’s IPO, Chinese regulators had hinted at more stringent regulations on micro-lending and the process of granting micro or small loans to individuals with financial need.

On 2 November 2020, the regulators imposed a new requirement forcing originators of credit (including Ant) to keep at least 30% of the loans on their balance sheet. This effectively makes Ant a bank, and a very capital-intensive one at that. By comparison, the Dodd-Frank Act, which was passed in the U.S. after the 2008 financial crisis, only imposed a 5% requirement, and that seemed to be working fine. Regulators also proposed to limit the loan size for online microlenders at RMB300,000.

On 26 December 2020, regulators ordered Ant to return to its origins as a payments service provider, restructure its lending, insurance, and investment services, and provide a timetable for doing so. The company was also required to set up a separate financial holding company to ensure capital sufficiency and protect personal data privacy. Regulators also reprimanded Ant for poor corporate governance, not complying with regulations, regulatory arbitrage, and alleged monopolistic practices.

In the best-case scenario, Ant will have to put up additional capital to meet the 30% requirement, thus earning a lower return on invested capital for each loan it originates. As a result, Ant will look more like a bank, and its valuation will closer reflect one than that of a tech company.

As of 15 January 2021, technology companies in the S&P 500 were valued at 28.4 times forward earnings, almost double that of banks’ price to forward earnings ratio of 14.7. Analysts have estimated that Ant’s IPO market value could halve if it were to hold just 20% of the loans on its balance sheet.

In the worst (but unlikely) case, Ant might have to spin-off its lending, insurance, and investment businesses, keeping only Alipay.

The fifth perspective

All that said, Ant is still a giant player in China’s burgeoning fintech industry and will be here to stay. However, the IPO could happen later rather than sooner, as it will take some time for the company to comply with the flurry of regulations. This will no doubt slow its growth and lead to a loss in potentially a hundred billion dollars in market value, but I believe that the new regulations are necessary to prevent a potential second financial crisis.