The upcoming Astrea IV retail bonds issued by Temasek subsidiary, Azalea Group, have been the talk of town. It’s the first time retail investors have had the opportunity to be exposed to private equity bonds in Singapore. It was placed in the limelight especially after Temasek CEO, Ho Ching, commented that it can be used to supplement one’s retirement portfolio.

Given that private equity investment opportunities are normally reserved for sophisticated investors, we were surprised that these bonds were accessible by the retail market. Although the prospectus tried hard to simplify the issuance, it is still quite a handful to digest.

We have decided to put forth a short explainer and some of our own thoughts regarding the Astrea IV bond issuance.

What is private equity?

Private equity is essentially a term to describe investments directly into companies that are not listed (i.e. not traded on the stock market).

Private equity funds have similar goals to you and me – they are looking to make a good return, and the way that they add value is by typically taking a large stake in a business. With a large stake, they are able to engage in the following:

- Restructuring the business (i.e. reducing costs)

- Enacting new business strategies

- Taking on more debt to optimize the capital structure

- Selling parts of the business to realize value for shareholders

The big difference between us (the retail investor) and the private equity investors is that the private equity investors have control and are thereby able to take a long-term view and to leverage up the balance sheet of the company. They are able to take an active role in the business to generate better returns as opposed to minority investors who are normally more passive in nature.

Private equity funds are funds that engage in private equity deals and typically invest in several companies with the funds raised.

Astrea is in the business of investing in private equity funds and therefore when we invest in its bonds, we are getting exposure to the returns potentially generated by the performance of the underlying private equity funds.

You can think of it like a fund of funds. They are essentially an entity that invests in many different private equity funds.

3 things you need to know before you invest

1. You are getting private equity exposure, but getting bond-like returns

Institutional investors that invest in private equity funds are obviously looking to generate higher returns. There is an implicit assumption that you are taking on more risk (and hence the higher return).

Investors in these bonds do not receive the big upside from the transactions if these funds do extremely well.

The way that private equity funds normally exit their investment is to either do an IPO or to sell the portfolio company to another business. The ultimate end game is to generate a multiple of the amount of money they put in from their own pockets.

If it does go according to plan (and there are times where it may not), the private equity funds can generate extremely high returns.

It is extremely important to note at this point that the retail bond investors do not get access to these lucrative returns because such retail bond investors are only vested in the debt portion of the deal.

If the funds do reasonably well, we get our principal back (i.e. the money we put in) as well as the interest promised. Even if the funds do exceedingly well, we still get the same amount of principal and interest.

2. You are getting a lower return because you are taking on less risk than equity holders

Let us think about it in terms of a hypothetical Mr Tan buying a property:

Assuming that a property is worth $1,000,000.

Mr Tan puts in $200,000 in equity and takes on a bank loan of $800,000 in debt.

If property prices were to fall by 15%, the property would be worth $850,000.

If Mr Tan defaults on his loan and the bank had to sell the property via auction at the marketplace, the equity holder ‘would be wiped out first’.

Assuming the property was sold for $850,000:

- The bank would get back $800,000

- Mr Tan would get back $50,000

As you can see, the bank would recover its full principal ($800,000) and be ‘made whole’. There is a cushion for the banks in terms of how far property prices can fall before they are in any real danger of making a loss. Mr Tan on the other hand as an equity holder would have lost $150,000 of his equity.

This above example illustrates that while the bank is taking less risk, it is also the same reason why the bank is charging a much lower interest rate and also receives no benefits from the upside gains of a property down the road that the homeowner gets.

In other words: less risk, less return, higher risk, higher return.

Let us just use a further example to drive home the point:

Assuming that a property is worth $1,000,000

Mr Tan puts in $200,000 in equity, the bank is only willing to loan $700,000 in debt at 2% interest rate, (secured over the property).

Mr Tan’s friend, Mr Wong, is willing to loan him the last $100,000 at 5% interest rate (this being an unsecured loan).

If property prices were to fall by 25%, the property would be worth $750,000. If the bank were repossess the property of it, and sell it off at market prices, the following distribution will occur:

- The bank would get back $700,000;

- Mr Wong would get back $50,000; and

- Mr Tan would not get back anything.

You can see how Mr Wong took on more risk to generate a higher return, but in exchange, he also took on higher risk in that he got back less of his money in the event of property prices falling dramatically.

The above example is crude but essential in understanding what a lot of people miss. Investors get a higher return because they are taking on some form of risk. In the bond market, they are either taking on the chance of a higher likelihood of default, or duration risk (i.e. the bond takes longer to mature).

You might be wondering why we have bothered to pen the above illustration regarding Mr Tan but understanding this analogy is crucial to understanding what investors are getting what they get in the Astrea IV bond issue.

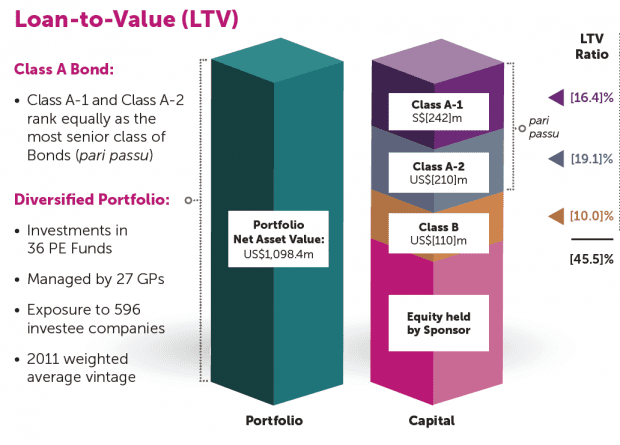

Investors are investing in the Class A-1 bonds are the most senior in the capital structure. Being the most ‘senior’ simply means that you have the highest likelihood of receiving your money back. If there are losses in the private equity funds that Astrea IV has invested in, the more ‘junior’ debtholders and equity holders are more likely to suffer a loss.

If you recall the analogy above, in the event of a loss, the bank is the least likely to lose money. Mr Tan and Mr Wong who have more upside are more likely to lose money in the event that prices go down and the property has to be sold in a fire-sale. In the case of the Astrea IV transaction, we are essentially the ‘bank’ and have the most safety (and thus a lower return than the other lenders or equity holders).

3. You are getting exposure to a widely diversified group of companies

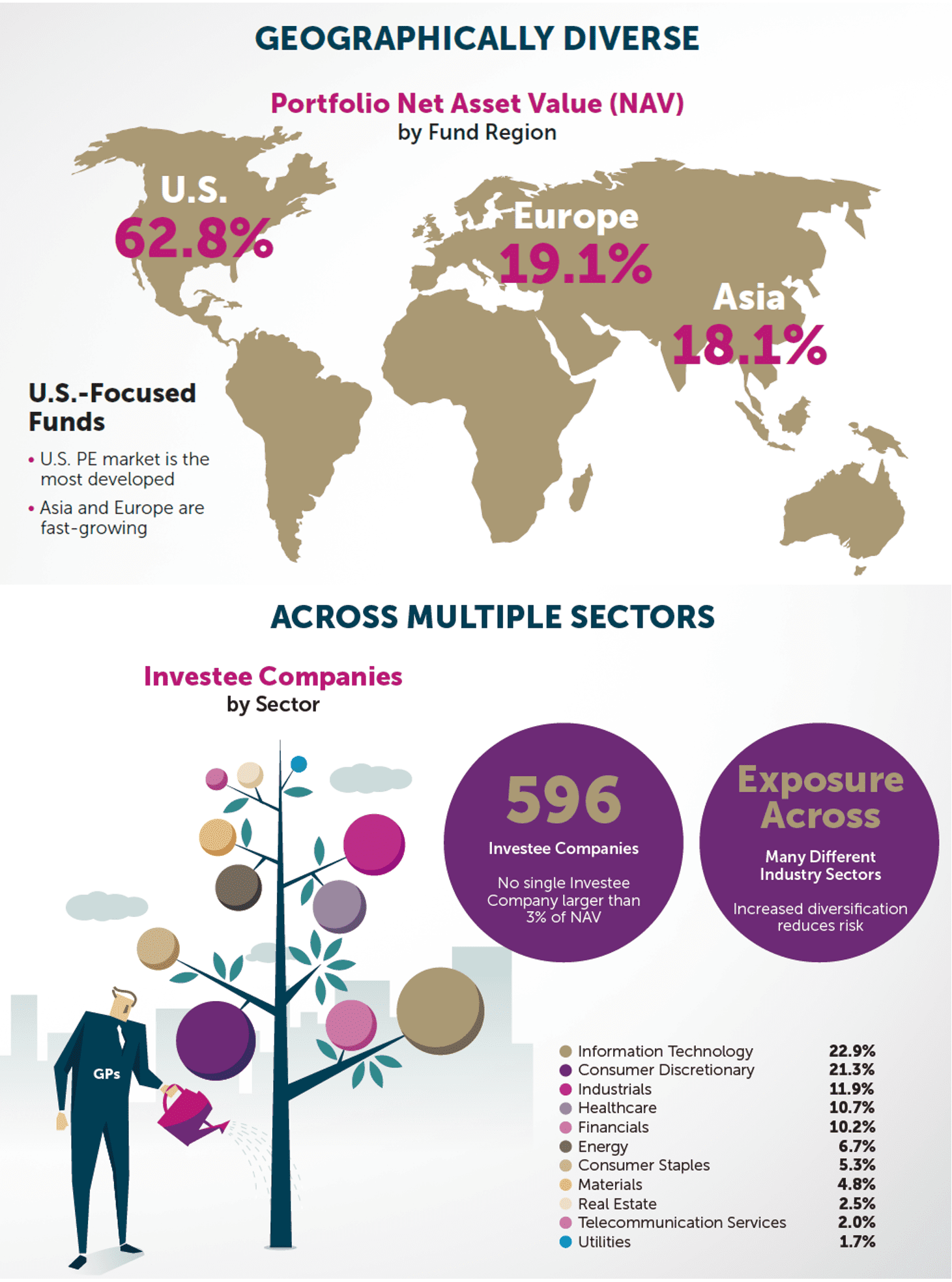

The underlying portfolio assets are investments in 36 private equity funds. These private equity funds are then further invested in 596 investee companies from a diverse range of industries from around the world (although there is a strong tilt towards the U.S.). The diversification across industries and companies means that investors bear little concentration risk (no company represents more than 3% of the value of the portfolio).

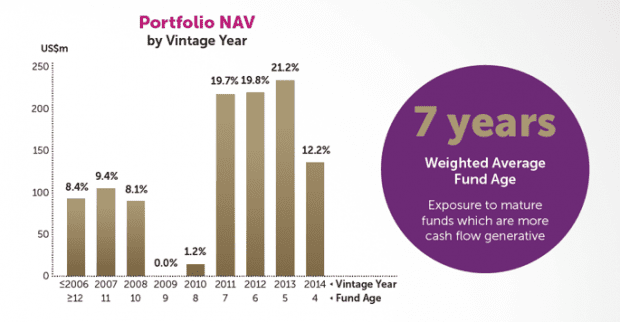

It is important to note that most of the funds were deployed in the years 2011-2013 (around 60%). At the end of the day, private equity funds have the same underlying drivers as stocks. They are able to generate significantly higher returns if the funds are deployed when market conditions are bad because they are able to pay lower prices and extract better deal terms.

In this case, 2011-2013 were not particularly good years for the U.S. economy because of a host of issues that included the downgrade of the U.S. debt for the first time in history and the Eurozone crisis which nearly threatened a breakdown of the European Union.

Although we are not able to get a deep dive into the portfolio companies, we think of it as an index fund of portfolio companies. The idea is not very far off from investing in the STI or S&P 500.

In this case, the general partners (i.e. fund managers) of the private equity funds are some of the biggest and best private equity funds managers in the market, which gives one some comfort of though in terms of capital allocation.

The short summary

The Astrea IV bonds provide an interesting investment opportunity. They are backed by cash flows from a diversified portfolio of equity funds. This is a very new fundraising instrument in the capital markets and probably not easily understood by retail investors.

It is important to note that the bonds are NOT guaranteed by Temasek. There is still a chance that interest is not paid or that investors’ capital is at risk.

Our personal view is that interest risk and capital risk is unlikely. This is not because of the reputational risk that a lot of people are banking on, but simply because the bondholders are really exposed to very little capital risk given the capital structure of the issue and the ‘structural safeguards’ which is built into the issue.

For more information, be sure to check Part 2 of the article which discusses these structural safeguards.

Tay Jun Hao & Terence Fong

Tay Jun Hao is the co-portfolio manager of the Heritage Global Capital Fund, a global value fund at Swiss Asia Financial Services Pte Ltd. Cumulative performance of fund strategy net fees from Jan 2012 – May 2018 is +149.13% (CAGR +15.50%).

Terence Fong practiced as a lawyer with a top-tier international law firm specializing in finance and capital market deals. He has practice experience in various jurisdictions in Europe and Asia advising on cross border transactions. He currently works with hedge funds to advise them on their capital and investment structure. He also works with venture capitalist funds to help start-ups grow and scale regionally and internationally.

Disclaimer: The authors will be subscribing in the bond issue. The above article does not constitute investment advice and simply represents the opinion of the authors.

Hello,

I’ve never purchased bonds before, so can i ask if this bond is still avail for purchase? If so how do i buy ?

Heard that V is releasing soon, what are your takes on this?

Hi Chris,

The Astrea IV bonds were fully subscribed last year. But, yes, the Astrea V bonds are being released soon which should be largely similar to the Astrea IV bond issue in terms of structure and features.