Chuck Akre, a seasoned investor and the visionary founder of Akre Capital Management, has a remarkable investment philosophy known as the ‘Three-Legged Stool Strategy.’ This strategic approach has not only stood the test of time but has also delivered outstanding results, compounding at an impressive rate of 14.92% since the inception of Akre Focus Fund in 2009.

The Three-Legged Stool symbolizes a synthesis of three indispensable investment pillars: 1) great businesses, 2) talented management, and 3) high reinvestment rates. Akre’s profound commitment to this metaphor is accentuated by the presence of an actual three-legged milking stool in the conference room of Akre Capital, serving as a tangible testament to the strategy’s resilience honed over years of experience. This article seeks to break down Akre’s Three-Legged Stool Strategy as a framework for sustainable investment success.

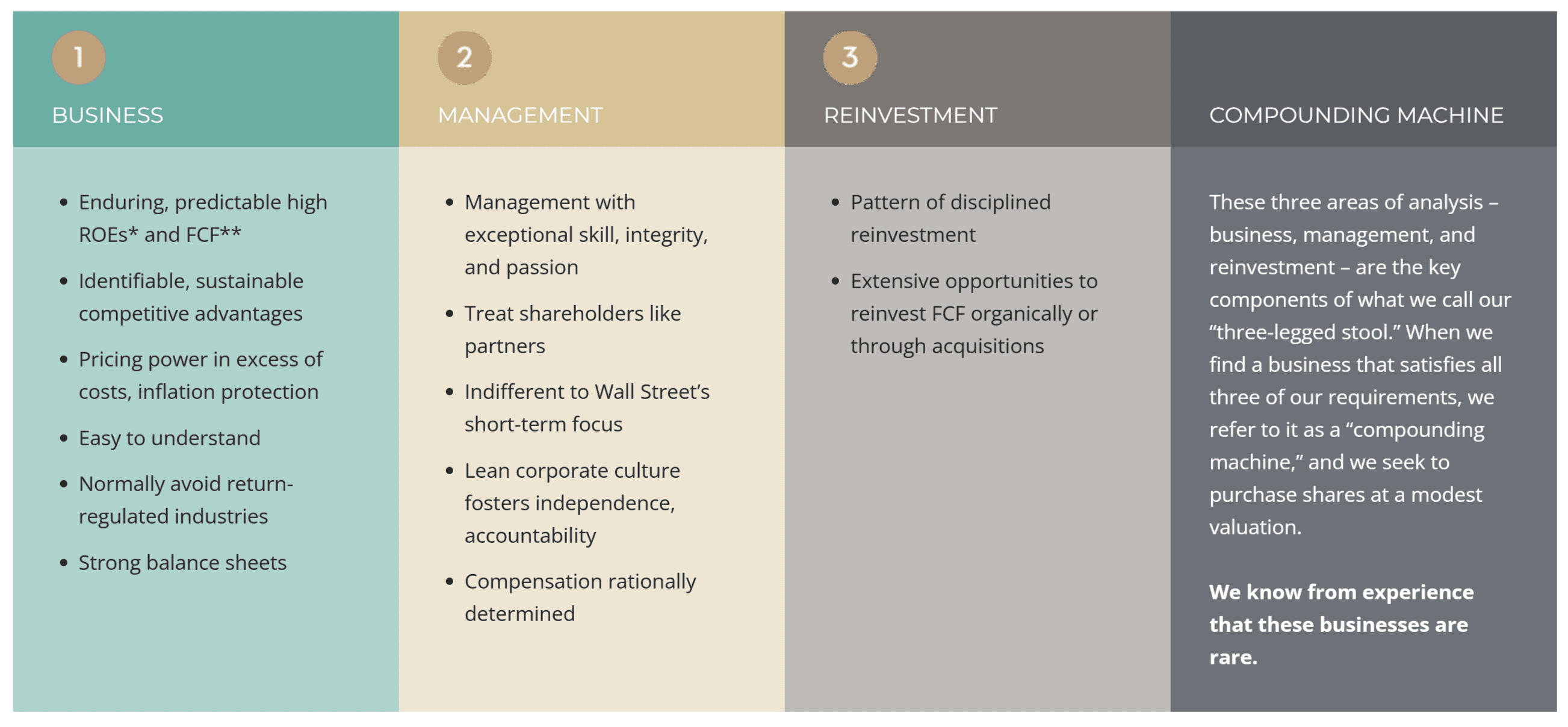

1st leg: Great business

Akre’s early investment in Berkshire Hathaway (since 1977) significantly influenced his investment philosophy, where he observed that the book value per share growth was a key driver of shareholder returns. Akre believes that, over the long term, a company’s returns are closely tied to its ongoing return on capital.

Akre’s emphasis on compounding and rate of return is evident in his belief that all investing is ultimately about the compound rate of return. To achieve superior returns, he actively seeks businesses with high returns on capital, aiming for companies where the returns far exceed the market average, typically in the 20% range.

For Akre, the key lies in identifying businesses with enduring high returns on capital and understanding the qualitative factors that contribute to their success. He acknowledges that the source of a business’s strength may not always be obvious, requiring a thorough understanding of the business model and qualitative factors that drive exceptional returns.

Akre looks for specific business characteristics, such as intellectual property, scale economies, regulatory advantages, high customer switching costs, or network effects. These factors contribute to the company’s earning above-average rates on employed capital. The overarching goal is to uncover businesses providing essential services, enjoying limited competition, and often leading in robust, long-term growth markets.

Additionally, Akre values businesses with real pricing power and low capital requirements, traits that enhance resilience in challenging markets. Such businesses consistently generate profits throughout economic cycles, maintaining solid balance sheets.

2nd leg: Talented management

In Akre’s view, management’s capability to run the business effectively is crucial. He seeks out leaders who have proven their prowess in executing business strategies. Akre often engages in conversations with executives to understand how they measure success at their companies, preferring indicators beyond stock price appreciation. He expresses a distaste for CEOs fixated on watching their company’s stock prices all day, seeing such behaviour as a distraction from the core business goals.

To thoroughly evaluate management, Akre and his team at Akre Capital delve into extensive research. They pour over shareholder letters, proxy statements, and biographies. Beyond office research, they visit corporate headquarters, manufacturing facilities, and retail locations on-site. This hands-on approach allows them to ask open-ended questions and gain insight into managers’ thoughts. Akre acknowledges that the evaluation process is not always instantaneous, and multiple visits may be required to form a comprehensive understanding of management quality.

Integrity is a non-negotiable criterion for Akre. He explicitly states his disinterest in CEOs who appear personally greedy, emphasizing the importance of managers acting in the best interests of all shareholders. The measurement of success, according to Akre, should ideally be tied to the growth in the company’s real economic value per share, showcasing a commitment to long-term value creation rather than short-term stock price fluctuations.

Akre insists on investing in managers who exhibit a clear track record of integrity and act in the best interests of all shareholders. He notes that managers who compromise shareholders’ interests once are more likely to repeat such actions, emphasizing the importance of capable business managers and those with ethical standards.

Furthermore, Akre places great emphasis on the alignment of interests between managers and shareholders. He seeks managers who treat public shareholders as partners, even if they are unknown to the management team. According to Akre and his team, the proxy statement can offer instructive insights into how managers view and treat shareholders. They examine the size of pay packages and the incentives triggering bonuses, with a preference for managers with skin in the game through direct ownership of common stock.

3rd leg: High reinvestment

The third leg of Chuck Akre’s Three-Legged Stool Strategy underscores the essence of a ‘reinvestment machine’ — a business that consistently generates high returns on capital and effectively reinvests that capital at those elevated rates.

Drawing inspiration from Warren Buffett, Akre acknowledges that such businesses become powerful in wealth creation over time. The strategy involves identifying and purchasing these businesses at a modest valuation. Akre places great importance on disciplined pricing, acknowledging that the rate of return is influenced not just by the quality of the businesses but also by the entry price.

His enduring perspective is evident in Akre Capital’s historical investments, which typically maintain a minimum holding period of five to ten years, allowing for resilience against temporary market fluctuations and quarterly hiccups. Akre advises against reacting to short-term factors, such as missed earnings reports or market trends, emphasizing the true value lies in focusing on the rate of return a company can achieve over an extended period. Even if the initial price appears high, Akre, echoing Charlie Munger, contends that the real reward manifests in the long term. The key takeaway is the commitment to holding on for an extended duration, recognizing that compounding wealth is a journey that unfolds over time.

The fifth perspective

Chuck Akre’s ‘three-legged stool’ investment process is a simple yet robust strategy that has proven its resilience across diverse business and market cycles. It consistently delivers impressive returns, reinforcing Akre’s unwavering confidence in its reliability. For those keen on understanding Chuck Akre’s investment philosophy, I highly recommend tuning into his podcast with Patrick O’Shaughnessy from ‘Invest Like the Best’ and Google Talks.