The markets are a volatile place. Wars, pandemics, recession, inflation, rising interest rates are some of the major events that have shaken the markets in just the past two years alone. Who knows what could happen tomorrow?

As an investor, you have to accept that risk and uncertainty is always a facet of the future (and your investments). For some investors, they learn to control their emotions and, through experience, become more comfortable with volatility. They know to jump in to buy when markets are down and remain patient when markets are exuberant.

For others, volatility is like an emotional rollercoaster they never wish they got on. Every plunge sinks their stomach, every climb brings a serious case of FOMO. What can you do if market volatility makes you queasy.

Enter dollar-cost averaging (DCA).

DCA is a simple method of investing equal amounts of money at regular intervals. When prices are high, you buy less stock for the same amount. But when prices are low, you get to buy more stock for the same amount. At the end of the day, you average out your cost per share and ignore the impact of price volatility.

| Month | Unit price ($) | Contribution ($) | Units bought | Average cost per unit ($) | Investment value ($) |

| Jan | 1.00 | 500 | 500 | ||

| Feb | 0.95 | 500 | 526 | ||

| Mar | 0.90 | 500 | 555 | ||

| Apr | 1.00 | 500 | 500 | ||

| May | 1.10 | 500 | 454 | ||

| Jun | 1.15 | 500 | 434 | ||

| Total | 3,000 | 2,969 | 1.01 | 3,414.35 |

For convenience, many investors also combine a regular savings plan (RSP) with their DCA strategy. An RSP is essentially your DCA strategy in action. An RSP can automatically transfer a predefined amount from your bank account to your brokerage account every month (or a frequency of your choice), which can then be used for your investments.

Since the stock market tends to rise over time, DCA is best used for long-term investments in a diversified index fund. On the other hand, DCA into an individual stock is riskier as a single company may not always grow successfully and could face threats that disrupt its business.

Now what if you’re an investor that prefers stock picking and doesn’t employ a DCA strategy for a diversified index fund, can you still take advantage of RSPs?

Yes, you can.

Combining your RSP with a cash fund

If you’re an active investor that prefers to pick our own stocks, you typically wait for opportunities to pick up high-quality stocks at undervalued prices. In the meantime, you can still take advantage of an RSP by investing in money market funds while you wait for market opportunities.

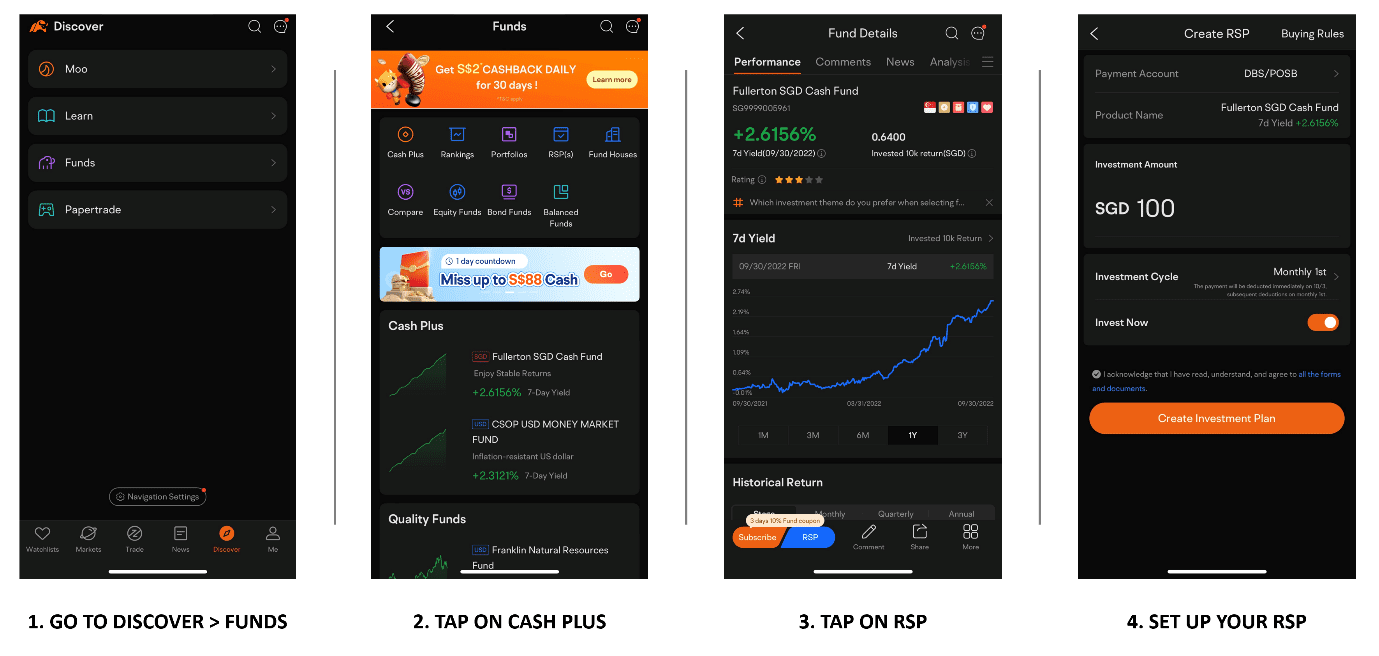

Here’s how you can do so using moomoo.

Moomoo SG offers an RSP and has two money market funds available: the Fullerton SGD Cash Fund and the CSOP USD Money Market Fund.

- The Fullerton SGD Cash Fund is the largest domestic cash fund in Singapore and aims to generate a return that matches the Singapore Dollar Banks Saving Deposits Rate. As of September 2022, the fund has not had a negative monthly return since its inception in 2009.

- The CSOP USD Money Market Fund is cash fund that aims generate a return comparable to U.S. dollar deposit rates. This fund was only launched in July 2022, so there isn’t a long-term track record we can refer to at the moment.

The Fullerton SGD Cash Fund and CSOP USD Money Market Fund currently offer an annualised yield of 2.6% and 2.9% respectively (as of October 2022). These cash funds can earn a potentially higher return than Singapore fixed deposits, while offering the flexibility to redeem your money anytime with no penalty.

Here’s how you setup an RSP for either cash fund with moomoo.

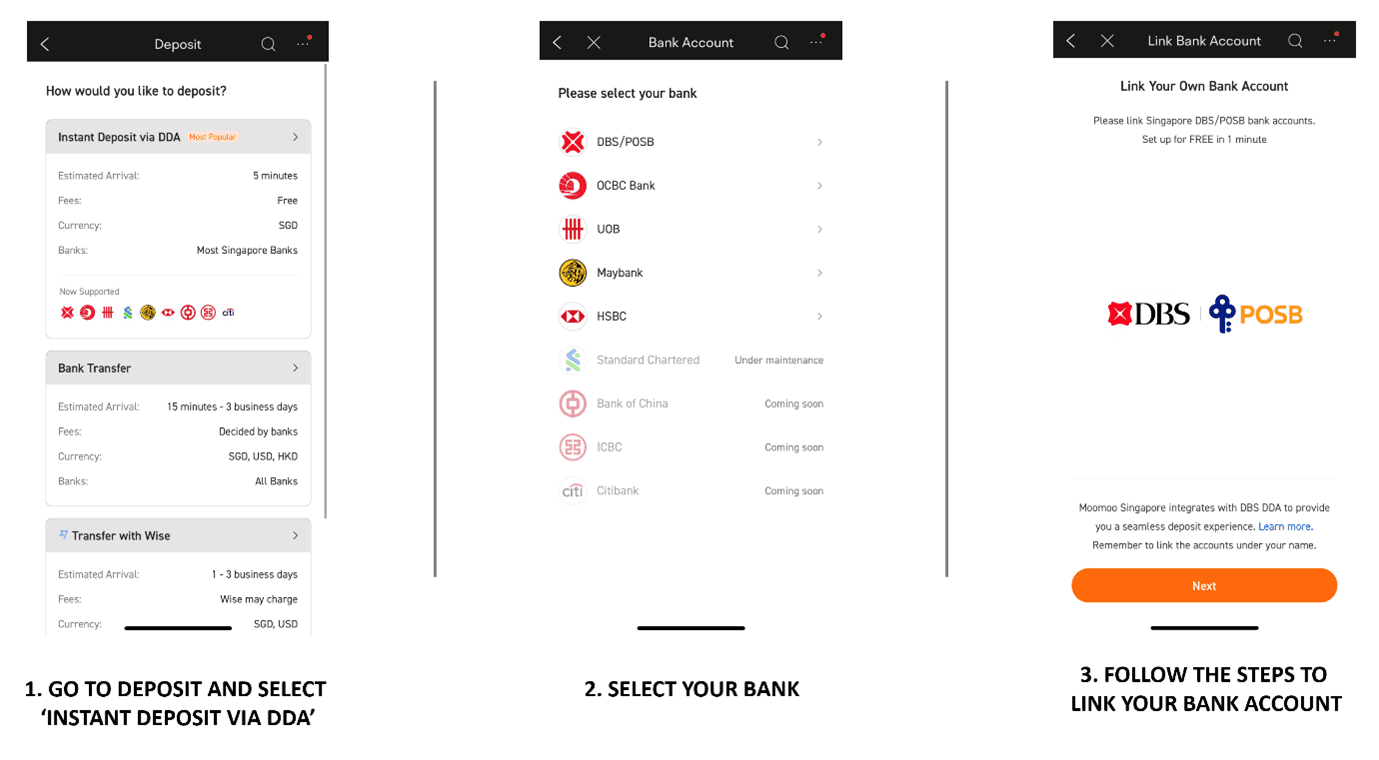

First link your bank account with the moomoo brokerage app.

Once you’ve linked your bank account, you can set up an RSP with your chosen cash fund.

You can set your preferred investment amount and frequency. Remember to also select your bank account as your payment account. You can stop your RSP at any time.

The fifth perspective

An RSP is a simple, disciplined way to save and invest your money into a fund of your choice. With interest rates inching higher and higher, it makes sense to hold your cash in a flexible cash fund to take advantage of rising rates as you wait for market opportunities to invest your cash.

From now till 31 October 2022, moomoo SG is giving S$2* cashback every day for 30 days if you make a one-time deposit of just S$100 in moomoo Cash Plus. That’s literally S$60 cashback! Moomoo SG charges ZERO fees when you subscribe to or redeem from moomoo Cash Plus.

So if you’re looking for flexible options to park your cash that earn a higher yield while waiting for potential stock market opportunities, you can consider subscribing to money market funds through moomoo Cash Plus.

Moomoo SG via moomoo trading app has announced a lifetime $0 commission on US market for eligible clients. They are offering one of the most competitive trading fees across US, HK, SG & China A Shares with live market data.

When you successfully register for your moomoo SG universal account via the moomoo app, you will get to enjoy $0 commission-free* trading for the U.S. stock markets, platform fees will be waived for the first year. You would also gain free access to Level 2 market data for the U.S. stock market; Level 1 market data for the Singapore stock market; Level 1 market data for China A Shares.

Investment products available through the moomoo app are offered by Moomoo Financial Singapore Pte. Ltd (moomoo SG), a capital markets services licence holder regulated by the Monetary Authority of Singapore. moomoo SG’s parent company, Futu Holdings Limited, is backed by world-class investors which include venture capital affiliates of Tencent, Sequoia Capital and Matrix Partners.

Open your moomoo SG universal account today with the moomoo app here. *Terms and conditions apply.

All views expressed in the article are the independent opinions of The Fifth Person. Neither moomoo Singapore or its affiliates shall be liable for the content of the information provided.

The content is provided for entertainment & informational use only. The information and data used are for purposes of illustration only. No content herein shall be considered an offer, solicitation or recommendation for the purchase or sale of securities, futures, or other investment products. All information and data, if any, are for reference only and past performance should not be viewed as an indicator of future results. It is not a guarantee for future results. Investments in stocks, options, ETFs, and other instruments are subject to risks, including possible loss of the amount invested. The value of investments may fluctuate and as a result, clients may lose the value of their investment. Please consult your financial adviser as to the suitability of any investment. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Why not just buy some Singapore Savings Bonds (SSBs) and some 6-month T-Bills every month? That way you build up a rolling portfolio of fixed-interest money with higher interest. That way we’re quite likely to do better than with the fund managers. SSBs are an excellent product and offer what is arguably (IMHO) the best combination of security, flexibility and return for a Singaporean investor’s safety fund.

Hey Jonathan! SSBs are great too. The only drawback is that you’d need to wait till the following month to redeem your SSB and this can take anywhere from 4-30 days (depending on when during the current month you decide to redeem). The funds offer a flexible, comparable alternative where you can redeem your money the same day and deploy it into the stock market the moment you see an opportunity.

Adam, when I think “Safety Fund” that’s real rainy-day money that’s ring-fenced and separate from investment capital. That one-month (sorry 4 to 30 days) wait to get our SSB money back (with any interest accrued) ensures that it’s not blown on impulse. My own strategy is always to have a safety fund, and take the view that the opportunity cost and erosion by inflation is akin to paying an insurance premium!

Definitely agree with you! Rainy day money should be saved and kept separately from investments; SSBs are perfect for that. At the same time, if you have investible cash waiting to be deployed, then the funds are flexible alternative.