Dairy Farm International Holdings Ltd (DFI) is a pan-Asian retailer that operates 9,700 retail outlets consisting of hypermarkets, supermarkets, convenience stores and health and beauty stores. The group has a presence in Singapore, Malaysia, Indonesia, Hong Kong and China and employs over 230,000 people.

DFI has grown over the years to become a powerful force in retail, as it expands its retail brick-and-mortar presence. The group has Giant (hypermarkets), Cold Storage (supermarkets), 7-Eleven (convenience stores), and Guardian (health and beauty stores) as its core brands, while also operating Maxim’s food and beverage outlets in Hong Kong, IKEA home furnishing stores in Taiwan and Indonesia, and Starbucks coffee chain in Macau.

Challenges facing the business

However, in the last couple of years, DFI has faced headwinds and challenges to its business, both in the form of increased competition from other brick-and-mortar retailers as well as e-commerce. With rising rental and staff costs in many Southeast Asian countries, DFI has seen its margins being increasingly squeezed even as it manages to grow its revenue base.

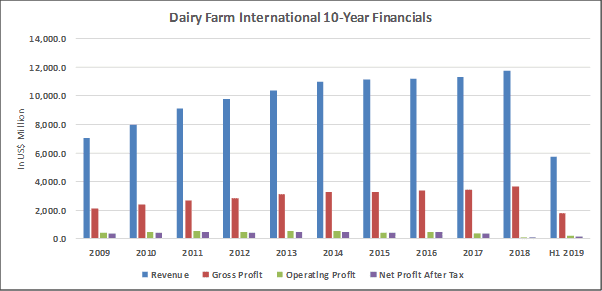

A glance at the 10-year financials above shows that even though DFI’s revenue has been growing steadily over the years, operating and net profit has actually declined. Note that DFI has been reporting weakness in its hypermarkets and ‘fresh’ segments in the last few years, culminating in the massive restructuring charge (to the tune of US$453 million) in FY2018 of Giant hypermarkets.

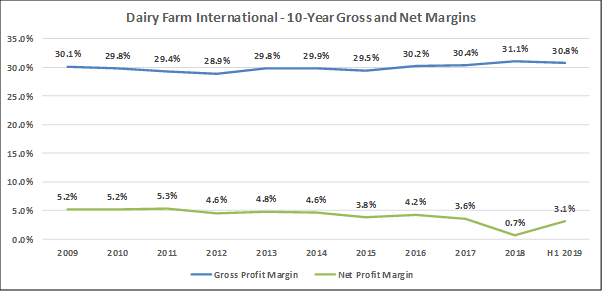

The gross and net margin trends for DFI have also been telling. DFI has managed to maintain its gross margin between a consistent range of 29% to 31%. This is great news for investors as it demonstrates that the retailer has strong pricing power and brand recognition, allowing it to negotiate for lower overall sourcing costs.

It’s a different story for net margins, though. If the exceptional items were adjusted for FY2018, then 1H 2019’s net margin of 3.1% would have been at a ten-year low. DFI used to be able to command net margins of 5-6%, but this has since fallen to the 3-4% level, in what appears to be a new normal for the business.

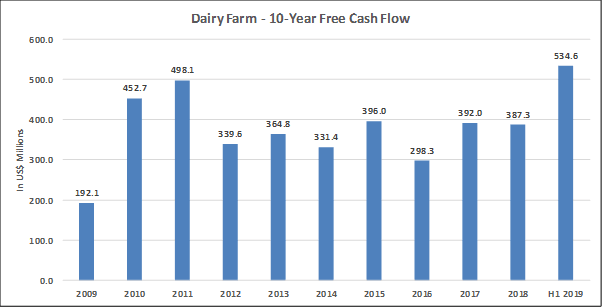

Free cash flow remains strong

Despite the pressures on its profitability, DFI continues to generate strong and consistent free cash flow (FCF). In fact, 1H 2019 saw the highest FCF generated in the last ten years, and this was only half a year’s worth of operations! This shows that the business is still essentially a cash-based one and that the group is able to churn out good FCF despite the challenges it faces in its hypermarket division.

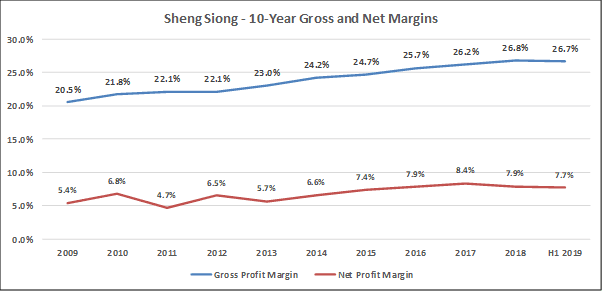

In Singapore, DFI faces competition from an up-and-coming player, Sheng Siong Group Ltd. Sheng Siong is an operator of supermarkets that feature both fresh live food as well as essentials and sundries, and its stores are located in HDB heartlands serving the mass market.

While Sheng Siong does not exhibit the same high level of gross margin as DFI, it’s worth noting that its gross margin has improved significantly over the last 10 years, from 20.5% to the current 26.7%. Its net margins are, on the whole, higher than DFI’s at the 7-8% level. One key reason could be due to Sheng Siong operating just one main segment – supermarkets — rather than having to manage a variety of different formats, which ties up resources, manpower, and money.

Dairy Farm’s ambitious transformation plan

DFI has, to its credit, not been standing still. Management has identified key areas of weaknesses and embarked on an ambitious ‘Transformation Plan’ when it announced its FY2018 earnings.

One shocking revelation emerged: the group would no longer be building hypermarkets, as the format had struggled to deliver decent returns over the years. Instead, DFI will be introducing pilot stores, trialling new innovations, and placing greater emphasis on fresh food.

As a result, some hypermarkets will be repurposed for other uses while others will be shut down. The US$453 million impairment charge relates to the write-down of assets within the hypermarkets division. While this move may send shock waves through investors, I feel that it’s timely that management has taken action to stem the bleeding rather than sweep the problem under the carpet.

Strategic priorities (as at 1H 2019)

Embedded within the Transformation Plan are five strategic priorities that the management envisions will allow the group to recover its footing and display growth once again. I shall briefly explain each point and how I believe it will impact the group:

- Grow in China. DFI has a 20% stake in Yonghui Superstores Co., Ltd, a leading supermarket chain in China. The group plans to work with Yonghui to undertake trials in order to better understand the Chinese consumer in order to work out targeted approaches to engaging them.

- Maintain strength in Hong Kong. DFI has many strong brands such as Mannings, Wellcome, and 7-Eleven in Hong Kong. The plan is to work on strengthening these brands and re-launching e-commerce here. However, with the current unrest and protests occurring in Hong Kong, this may hinder the progress of the group’s initiatives somewhat.

- Revitalise Southeast Asia. The plan here is to re-engineer DFI’s food offerings and convert hypermarkets to large food format stores over time in order to better engage the Asian consumer base. This requires both right-sizing, optimising, and redefining space allocations to ensure maximum efficiency and utility are achieved.

- Build capability. New senior appointments to be made in order to strengthen the group’s capabilities and experience in tackling different challenges.

- Drive digital innovation. DFI has admitted to under-investing in technology and digital initiatives and being behind the curve when it comes to utilising technology to improve business performance. Two new positions were created — Chief Digital Officer and Chief Technology Officer — in order to spearhead the necessary changes. The IT infrastructure will also be upgraded and a SAP system rolled out more quickly to all regions.

These initiatives are forward-looking and are an encouraging sign that the management is candid, willing to admit its flaws, and is taking progressive corrective action to steer the business back on the right footing.

Improvement programmes

Apart from the strategic initiatives highlighted above, DFI is also rolling out improvement programmes to enhance productivity and increase efficiency. If done right, these programmes should help to reduce overall waste and lower both the cost of goods sold as well as operating expenses.

Supply chain efficiency involves looking at the entire supply chain end-to-end to see how it can be optimised. An example would be ordering from a few key suppliers in order to consolidate orders rather than dealing with a wide range of suppliers with different requirements and terms and conditions.

Labour productivity involves extracting more value from each worker by improving the flow of product into the stores and improving overall net working capital requirements. Assortment optimisation will help to reduce cost prices and lead to better overall gross margins, while procurement centralisation involves the group taking on a more consistent approach in negotiations with suppliers so as to improve coordination. All these improvement initiatives are operational in nature, and their effects will be observed incrementally as each starts to deliver results over time.

My take on Dairy Farm’s transformation plan

Of DFI’s five strategic imperatives, I have stronger confidence in just three of them:

- Growing in China is achievable through DFI’s stake in Yonghui, and the group’s existing presence in China should also make it easy for more doors to open.

- Revitalising Southeast Asia is also an initiative that is likely to succeed, as management has recognised that hypermarkets are not financially viable and are willing to try smaller, targeted store formats.

- Finally, hiring a new team with fresh blood is positive as it helps to bring in new perspectives and skillsets to replace any form of antiquated or outdated thinking.

However, maintaining strength in Hong Kong is not going to be an easy task. The riots in Hong Kong have thrown a spanner in DFI’s works, though at this juncture, no one is sure if these protests will have a permanent, lasting effect on retail demand and footfall. What has been reported is that tourism and retail have both taken massive hits in the wake of six months of continuous protests. DFI may wish to revisit this initiative as it was announced during the February 2019 earnings release when the riots had not yet begun.

The other aspect that I lack confidence in is management’s ability to drive digital innovation. It seems rather surprising to me that such a large company had taken so long to embrace technology and digitalisation when there have been so many changes in retailing in just the last few years. There’s even technology that allows customers to walk in and take items from the shop while scanners and software employing artificial intelligence will record the items and bill that customer accordingly.

While such cutting-edge technology is still at a nascent stage, it underscores the pressing need for companies like DFI to embrace technological change rather than being stuck in the past. I was also very surprised to learn of the new CDO and CTO roles being created only recently, as the assumption here is that no one took charge of both the technological and digital aspects of the business (including e-commerce) for so long.

The fifth perspective

It’s still too early to determine if the above initiatives will have the desired effect on the group’s performance. The CEO mentioned that it will be at least a five-year wait as such changes need time and lots of planning in order to execute well.

Investors should note that significant risks are involved here: that the plan may go awry along the way, certain initiatives may suck up lots of time and resources without achieving tangible results, or worse, that new challenges crop up along the way with management always being ‘two steps behind’ and trying to catch up.

Investors need to have significant amounts of patience and continue to monitor the business to see if things really do improve over time.