The advertising industry used to be a simple one. Want an advertisement? Want some attention? Take out an ad in the Straits Times or relevant language-related paper and you could virtually guarantee some amounts of interest. I even remember scanning the classifieds section as a secondary school kid looking to earn some money during the holidays.

Fast forward two decades — the rise of Google, Facebook, and a declining local interest in state affairs beyond headline centrepieces, and you have the current situation: Singapore Press Holdings’ (SPH) print media business is in terminal decline and not headed anywhere but down.

Indeed, even Chairman Lee Boon Yang remarked multiple times during the extraordinary general meeting: ‘Investing more resources into SPH’s print media business is akin to changing pounds for pennies.’

Having said all that, here are the top five takeaways I had from the 2021 SPH EGM.

1. The newspaper business is an albatross around the neck

There’s probably been a lot of internet ink spilled over the secular decline of the print media industry already, but for those not in the know, here’s a recap. The print media business served as old world aggregators of attention. You read it every day to know what was going on nationwide, and around the world.

Because you read it every day, it was a valuable ‘platform’. Businesses could and often did advertise there, splashing half or full-page ads for five to six-figure sums. And classifieds were fill with ads for job vacancies, services offered, and deals to sell/rent/buy a property/car/item. This meant despite the newspapers selling for $1-2 a copy, SPH collected fat fees on advertising within Singapore because of its nearly monopolistic power.

This all changed when Facebook and Google became the rulers of attention aggregators globally (sans China). Digital aggregators could also show articles by relevance, allow commenting and discussions, and were published in real time (versus next-day printing for the press).

Just as important as the qualitative aspects of the digital platform are the quantitative aspects. It costs Facebook/Google next to nothing to service the next 100,000 customers. A newspaper on the other hand printing another 100,000 copies of a paper incurs real cost (in raw materials, labor, transportation, and distribution).

Further, Facebook and Google’s return on incremental capital invested was high: since the main business did well, reinvesting cash flows to grow the business was a naturally good thing to do. This isn’t quite the same when you’re running a capital-intensive newspaper business with distribution partners, physical goods, transportation costs, and a dwindling reader base and a dwindling ad revenue base.

In short, for SPH to continue running its media business would be akin to carrying a deadweight around while trying to move forward. Management has repeatedly mentioned that reinvesting cash flows into this business is exchanging pounds for pennies. I can’t help but agree. Times have changed.

2. Shareholders must accept short-term pain to cut off legacy media business

Having discussed the competitive dynamics and quantitative aspects of the business, here’s a clever remark a friend, working as an analyst, once recounted to me.

‘My boss once told me that you should be willing to own any business at some price point…’ And he paused, as if reliving some great trauma, ‘And sometimes that price is negative.’

This point is made less humorous by the fact that, today, SPH shareholders are doing that very thing. They’re paying someone else to take SPH’s media assets off their hands so they can be rid of it for good.

Is this short-term pain worth it?

That depends. Is holding onto a deadweight while trying to outrun competitors any good? Of course not. SPH has other assets that can do better without having to support the ‘burden’ that is the media business.

Is SPH better off by a significant amount cutting off its media arm? I can’t say for certain. But I’d say anything that’s losing money and set to lose more money over time is something I don’t want a part in.

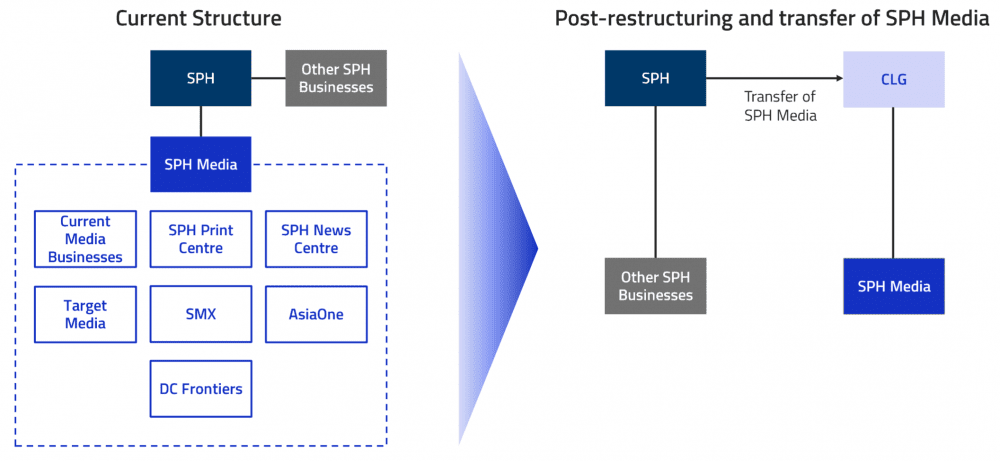

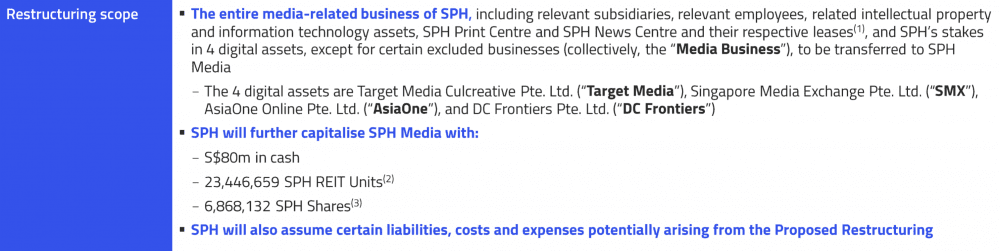

3. Issuance of shares to CLG is not ideal

Part of the transaction of hiving off its media assets to the newly formed not-for-profit company limited by guarantee (CLG) requires SPH to cough up S$80 million in cash, 6.9 million in shares, and, notably, 23.4 million SPH REIT units.

This part of the deal I’m not as much a fan of. A common theme throughout the entire EGM was that SPH wanted to wash its hand off its media assets. Units of SPH REIT currently trade at a 3.9% yield. Sure, it’s not a sky-high yield, but it does mean that those units are ‘subsidizing’ the media operations through future SPH REIT distributions. I get there’s a need for an incentive, but I’d rather have paid all cash and been done with the deal forever as opposed to owing a sum of cash flow indefinitely via dividends.

4. Political ramifications of news media is important

We live in a time where fake news and random articles about events that have never happened can spread like wildfire over social media. Most people fail to check for truths and, even then, most of them may not be able to find it.

Perhaps important then is the role that the national newspaper aims to provide: timely, factual, important information to the citizenry. SPH management has stated that its media business plays a ‘critical function’ in Singapore and winding it up is ‘not an option’.

At the same time, new ways of communication are now here. We now have a Gov.sg WhatsApp channel (a Facebook platform). I can easily see a time where the country expands its own means of media distribution beyond newspapers, TV, and radio.

5. A shareholder asked if SPH could have increased prices

Management responded that this was an interesting question and one of the few natural ones to have as a response to the increasing pressures of a declining readership. However, remember that industry dynamics which are not in a business’s favour rarely allows pricing increases or what we call pricing power.

Autodesk, for example, recently received an open letter from the Royal Institute of British Architects complaining about prices increasing nearly 70% over the past five years. Underlying that humongous cost increase is a product’s stickiness. Autodesk’s key products — AutoCad and Revit — are viewed as industry leaders in the field of design, conceptualization, and construction with most major developers worldwide.

It’s quite different when you’re a newspaper with declining readership and no sticky customer base. SPH management mentioned that even small price increases in the subscription services saw significant discontinuation of services.

The fifth perspective

More important questions that were not addressed were things like why SPH failed to transition successfully into a digital platform subscription business. The New York Times for example has made a similar transition in the face of mounting pressures from Facebook and Google. Though I acknowledge their customer base is larger and American news more well-followed around the world.

Some would even argue that SPH has tried and failed (or still trying at least). On one hand, it feels like the transition was a little too slow, that Singapore journalism was not fostered enough and nurtured a voice that would make Singaporeans care and want to read more. On the other hand, under the stewardship of the CLG, a new dawn for Singapore news and journalism may well emerge, no longer shackled by the old pressures of profit and shareholder value.

Liked our analysis of this AGM? Click here to view a complete list of AGMs we’ve attended »