Founded in 1933, Hang Seng Bank serves over 3.5 million local residents via about 280 branches located in Hong Kong. It is a principal member of the HSBC Group where HSBC presently owns a 62.14% equity interest in the bank. As of 30 January 2020, Hang Seng Bank is worth HK$304 billion in market capitalisation and is one of the largest listed companies on the Hong Kong Stock Exchange presently.

In this article, I’ll cover its latest annual results and stock valuation. Here are 10 things to know about Hang Seng Bank before you invest:

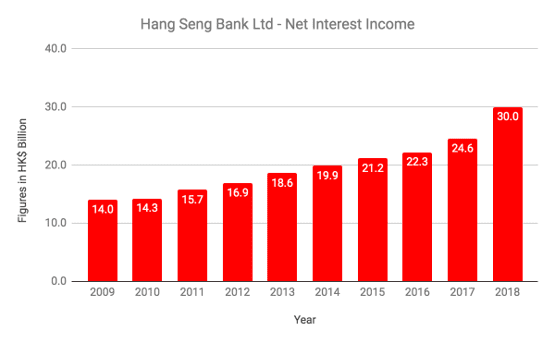

1. Net interest income (NII) has increased by a CAGR of 8.8% for the last 10 years, growing from HK$14.0 billion in FY2009 to HK$30.0 billion in FY2018.

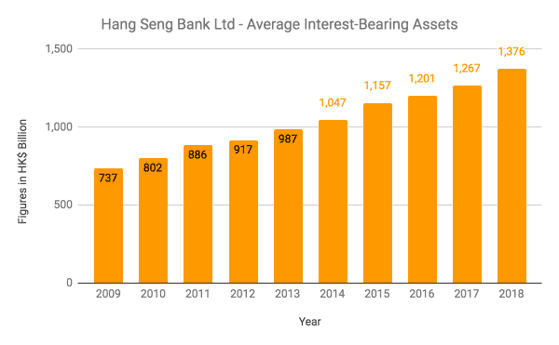

This is mainly attributed to growth in its average interest-earning assets which increased from HK$737.0 billion in 2009 to HK$1,376.1 billion in 2018, and also a slight rise in net interest margins from 1.90% to 2.18% during the period. Its growth in average interest-earning assets is due to a stable rise in corporate, commercial, and mortgage lending during the period.

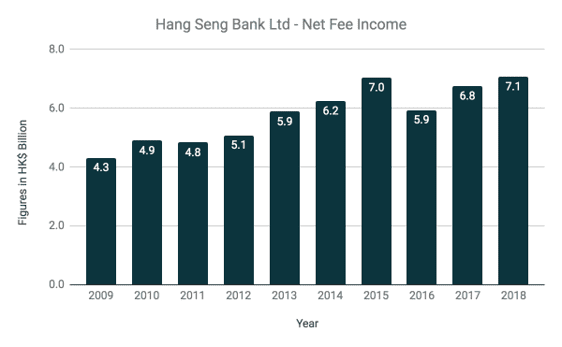

2. Net Fee Income (NFI) has increased by a CAGR of 5.6% for the last 10 years, growing from HK$4.3 billion in 2009 to HK$7.1 billion in 2018. This is mainly due to growth from its credit card business and wealth management services which mainly involves the sale of retail investment funds.

Here’s a list of Hang Seng Bank’s major sources of fee-based income:

| Major Sources | 2009 Gross Fee Income (HK$ million) | 2018 Gross Fee Income (HK$ million) | CAGR |

|---|---|---|---|

| Cards | 1,413 | 3,014 | 8.8% |

| Stockbroking and Related Services | 1,566 | 1,704 | 0.9% |

| Retail Investment Funds | 604 | 1,682 | 12.1% |

| Other Fee-based Income | 1,607 | 3,269 | 8.2% |

| Total Gross Fee-based Income | 5,190 | 9,669 | 7.2% |

| Fee Expenses | (869) | (2,602) | 13.0% |

| Total Net Fee-based Income | 4,321 | 7,067 | 5.6% |

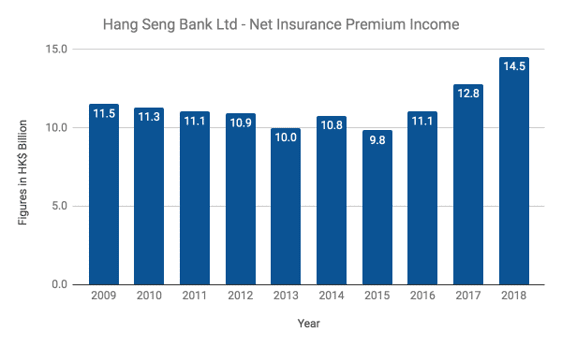

3. Net Insurance Premium Income (NIPI) has grown to HK$14.5 billion in 2018 from HK$9.8 billion in 2015. This is a turnaround from a gradual fall from HK$11.5 billion since 2009. This is because Hang Seng Bank has managed to increase its gross insurance premium income over the last three years as a result of rising demand for its retirement and protection products, which surpassed the amount of reinsurance expenses conceded during the period.

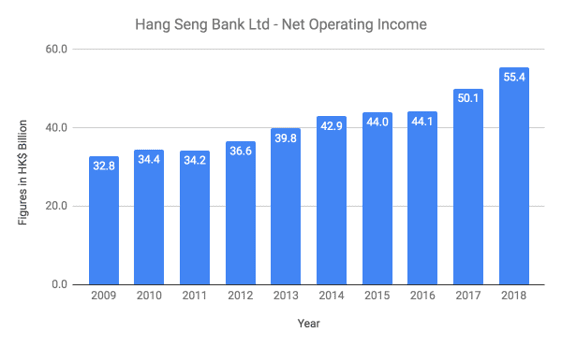

4. Overall, Hang Seng Bank has attained a CAGR of 6.0% in net operating income (NOI) over the 10-year period. NOI has increased from HK$32.8 billion in 2009 to HK$55.4 billion in 2018, attributed to increase in NII, NFI and NIPI as described above.

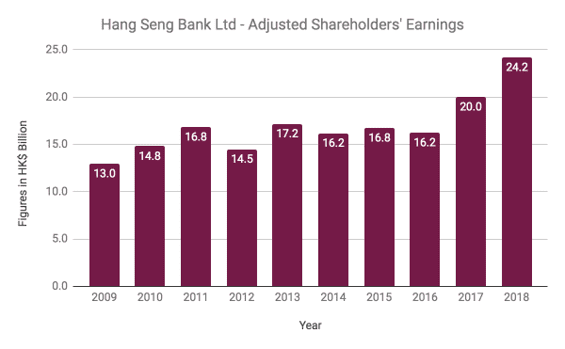

5. Adjusted shareholders’ earnings have risen from HK$13.1 billion in 2009 to HK$24.2 billion in 2018 — a CAGR of 7.2%. This is attributable to an improvement in Hang Seng Bank’s asset quality and cost-efficiency – from 2009 to 2018, its gross loan impaired ratio dropped from 0.39% to 0.25%, and its cost-to-income ratio improved from 33.7% to 29.5%.

Note: Hang Seng Bank’s shareholders’ earnings from 2012 to 2015 have been adjusted to exclude the financial impact of its stake in Industrial Bank:

| Year | Transactions Arising From Industrial Bank |

|---|---|

| 2012 | Share of Profits: HK$5.2 billion |

| 2013 | Accounting Gain: HK$8.5 billion (reclassification of IB from associate to financial investment) |

| 2014 | Impairment Loss: HK$2.1 billion |

| 2015 | Gain on Partial Disposal of its Stakes: HK$10.6 billion |

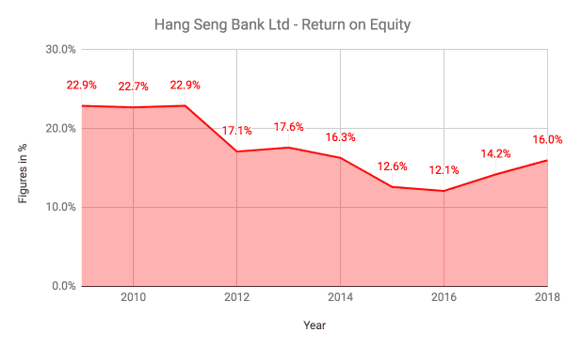

6. Hang Seng Bank has a five-year return on equity (ROE) average of 14.2%. This is a decline from ROEs of above 20% prior to 2011.

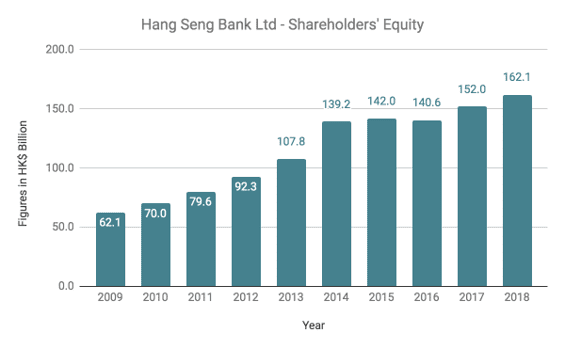

The fall is due to Hang Seng Bank’s growth in shareholders’ equity from 2012 to 2015 as the bank recognised an accounting gain for Industrial Bank in 2013 and the issuance of perpetual capital instruments in 2014.

7. As of 30 June 2019, Hang Seng Bank has a total capital ratio of 20.4%, liquidity coverage ratio of 224.5%, and net stable funding ratio of 152.5%, which exceed the minimum requirements imposed by the Hong Kong Monetary Authority. This indicates that the bank has sufficient financial resources to meet its obligations and to weather adverse economic conditions if they arise in the future.

8. For 1H 2019, Hang Seng Bank has maintained its growth momentum in NOI and shareholders’ earnings. This was contributed by an increase in NII and NIPI which offset a dip in NFI due to falling sales in stockbroking and retail investment funds. Here is a summary of the bank’s latest interim results:

| 1H 2018 (HK$ million) | 1H 2019 (HK$ million) | Change | |

|---|---|---|---|

| Net Interest Income | 14,228 | 15,853 | +11.4% |

| Nee Fee Income | 3,989 | 3,485 | -12.6% |

| Net Insurance Premium Income | 8,732 | 9,224 | +5.6% |

| Net Operating Income | 20,411 | 21,899 | +7.3% |

| Cost-to-Income Ratio | 27.7 | 28.2 | +0.5% |

| Shareholders’ Earnings | 12,647 | 13,656 | +8.0% |

Source: Hang Seng Bank 1H 2019 interim report

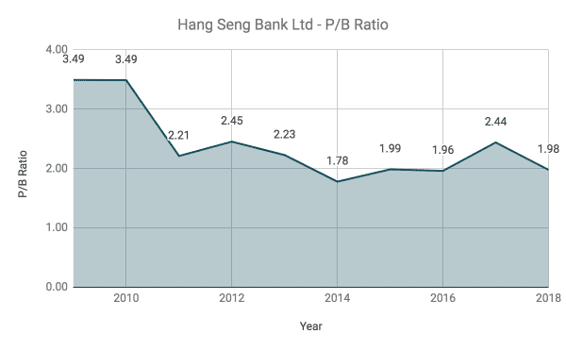

9. P/B ratio: As of 30 June 2019, Hang Seng Bank had net assets of HK$90.34 per share. Therefore, based on its share price of HK$158.20 (as at 30 January 2020), Hang Seng Bank’s P/B ratio is 1.75, which is a 10-year low.

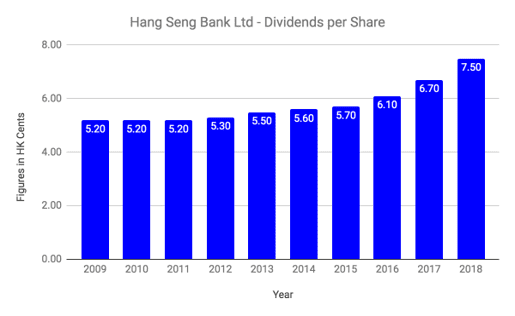

10. Dividend yield: Hang Seng Bank paid 7.5 cents in dividend per share in FY2018, which has steadily increased since FY2012.

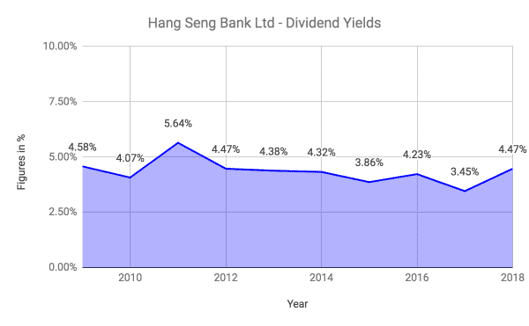

Based on this, Hang Seng Bank’s dividend yield is 4.74% which is higher than its 10-year average of 4.35%.

The fifth perspective

Hang Seng Bank Ltd has delivered consistent growth in NII, NOI, and dividends over the past 10 years. The bank has also kept its total capital, liquidity coverage, and net stable funding ratios at levels well above their minimum regulatory requirements. Presently, Hang Seng Bank is trading below its long-term P/B average and offers a decent dividend yield of 4.74%.

Read more: Compare Hang Seng Bank with UOB, OCBC, DBS, Public Bank, and Maybank here.

Hi, May I know how you get NAV value for Hang Seng bank? I tried to find in their financial report, they don’t have this clear.

Hi Ricky, you may take its shareholders’ equity (HK$172.7 billion) as of 1H 2019 and divide it with its number of ordinary shares (1.912 billion).