Singapore’s Deputy Prime Minister, Tharman Shanmugaratnam, declared recently that the CPF Investment Scheme (CPFIS) is not fit for purpose. Over the past ten years, 45% of investors lost money and 80% of investors can’t even make the 2.5% benchmark given by the CPF Ordinary account. The Deputy Prime Minister had the following observation:

“We mustn’t allow the individual to feel that they’re an expert in market timing. You’ve got to lock your money in for some defined period, and there has to be (an) incentive to not switch from one investment to another. There has to be that incentive to keep your money locked up in one account for the long term, because that is how superior long-term returns are earned.”

In other words, the government has recognized that market timing is a major reason why Singaporean investors lost money in their CPFIS. Such losses impair our ability to purchase our houses with our CPF Ordinary Account and meet our retirement needs through the CPF Special Account. The reason why most people lose money when they attempt to time the market is that they end up buying high and selling low.

How your own psychology sabotages you

Most people understand that they must buy low and sell high to make money so why do they end up doing exactly the opposite? For us to understand that, we must look at the psychology behind their investment process that overrides the rational mind and destroys their portfolio returns in the process.

Berkshire Hathaway’s vice chairman, Charlie Munger, recommends investors read Robert Cialoni’s ‘Influence: The Psychology of Persuasion’. In this classic book, it explains the concepts on social proof and scarcity biases which cause us to make stupid investment decisions.

1. Social proof

Social proof is defined as informational social influence where people assume that the actions of others to be correct. It is about conforming to a social norm and people do so to be liked by others. If a lot of people are doing the same thing, then we assume it to be correct. People tend to look for cues to interpret an ambiguous situation which happens frequently in your investment decision.

For instance, if you read two conflicting reports on Singtel. One report urges you to sell Singtel because of the possible entry of a fourth telco that will depress earnings. Another report urges you to buy Singtel because most of its earnings come from overseas and it would be a good defensive stock in uncertain times. Confused?

In this scenario, you will look for social cues of whether to buy Singtel. You may be influenced to buy when you read that reputable investors such as GIC are buying into Singtel. Another social cue would be the stock market where you see that Singtel’s price is rising steadily which indicates social acceptance.

After observing it for a month, you decide to buy Singtel. By then, it could already have reached a peak with all the good news already priced in. Shortly after your purchase, the demand for Singtel shares subside at such high prices and the share price starts to correct itself. You now start to read reports that other reputable investors are now selling Singtel which is sufficient social proof for you to sell Singtel. (Note: This is a hypothetical example and we are not making any recommendations about Singtel.)

This is the typical scenario of how the typical amateur investor ends up buying high and selling low by following their social proof bias. All these happen at the subconscious level and most investors are not aware of this motivating factor.

2. Scarcity and loss aversion

Scarcity and loss aversion work hand-in-hand to influence our behaviour. When the stock price is rising, we are more likely to jump into the trade because we are afraid of losing out. This is why people will queue up for the new iPhone (or get into fights over Hello Kitty toys at McDonald’s). After you buy a stock and it drops, you are more likely to start selling to preserve the capital you have. Scarcity and loss make a powerful combination. Studies have shown that people are more sensitive to possible loss than possible gain and this behavioural bias can be a killer to your investment returns. When you ask people if they are more willing to avoid a $5 surcharge or get a $5 discount, they are more likely to choose the former.

The classic example would be how Nick Leeson drove Barings to bankruptcy in 1995. It all started with a small loss in July 1992 when he made a small loss of £20,000 pounds and he hid it in an error account instead of owning up. The losses quickly ballooned into £2 million at the end of the year and shot up to £208 million by the end of 1994. In other to recoup his growing losses, Nick engaged in increasingly riskier bets which backfired.

One of his last major moves was a short straddle which bet that the Japanese stock market would not move on 16 January 1995. However, the Kobe earthquake struck on 17 January 1995 which caused huge movement not only in Japan but Asian markets everywhere. Then he made his final bet that the Nikkei would recover rapidly after the earthquake but it didn’t. In the end, losses reached £827 million which ultimately bankrupted the 233-year-old bank.

When you trace how Leeson’s losses grew from a mere £20,000 to £827 million, you realize that they can be traced back to the simple bias of scarcity and loss aversion. If he had accepted that initial loss, he would have been in a clearer, non-desperate frame of mind to execute his second trade. Has something similar happened to you or your close friends before?

The BBC quoted Leeson about another rogue trader who lost billions for a French bank:

“Success was the thing that drove him on. It’s a fundamental part of the markets and the people that work within it. Probably his biggest fear is the fear of failure, as it was mine, as it probably still is today. When he got himself into the situation there would have been a degree of panic.”

Most people would have experienced this loss aversion before which prevents them from investing successfully. They are more likely to sell their winning trades and hold onto their losing trades to avoid the pain of losses.

A scientific study

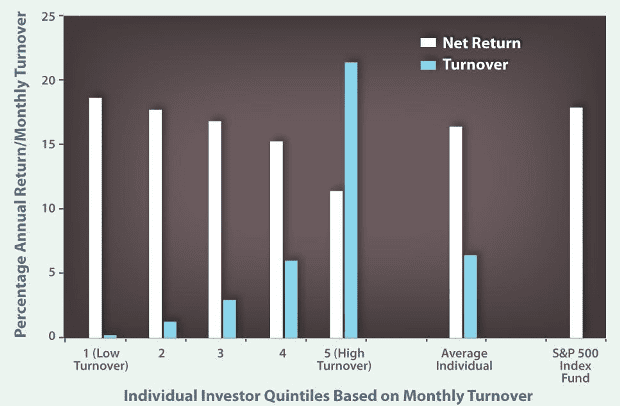

Professor Terrance Odean, from the University of California, Berkeley, did a real-life study on the trading records of 78,000 households from brokerages in the United States over a seven-year period. He focused his attention on investors who traded stocks based on speculative reasons based on their behaviour such as selling stocks for gains and buying another stock within three weeks. He filtered out trading for non-speculative reasons such as liquidity (e.g. selling a stock to pay for tuition).

Source: American Association of Individual Investors (AAII)

These speculative investors have high turnover but their returns are actually lower despite their efforts from 1991 to 1997. Even after adjusting for trading costs, higher turnover leads to lower returns for the investor and regret plays a prominent role. Investors have the tendency to sell their winners to make them feel good.

Researchers also found that only 1% of Taiwanese day traders are successful. Taiwanese investors traded even more frequently than U.S. investors. The professor noted that people look into the future when they buy, and look into the past when they sell. Investors tend to rationalize their decisions later which doesn’t help improve their decision-making skills or the size of their investment accounts.

The fifth perspective

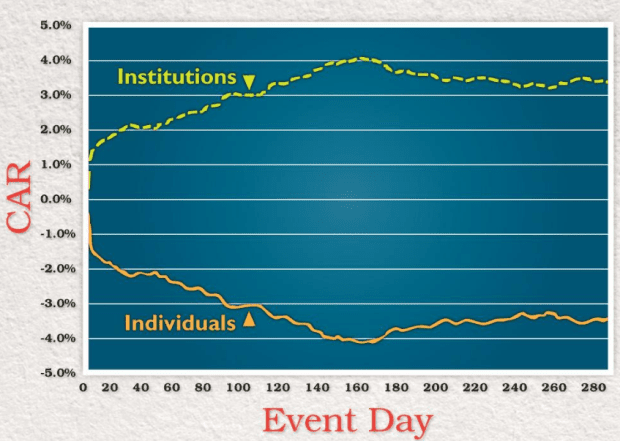

The deputy prime minister is basically saying that the government has to ‘save’ amateur investors from themselves with incentives for long-term investing. Indeed, studies have shown that most retail investors find it hard to manage their emotions nor have the time to do the necessary research.

Source: American Association of Individual Investors (AAII)

The performance of retail investors shows that investing is a professional job. Professor Odean encouraged investors not to chase performance and write down the reasons for owning a stock instead of buying on impulse because Jim Cramer recommended it or the Wall Street Journal gave a good report. According to him, most investors would be better off buying a low-cost and well-diversified exchange traded fund. Indeed, most people are better off not trading because it is very difficult to manage their social proof and scarcity biases.

At the end of the day, our CPF funds are not just some figures on a screen. It is real money for your retirement or housing needs even if you can’t withdraw the funds at will. These enforced savings will be crucial to your survival when you are not able to work and they must be nurtured carefully. If your trading record shows consistent losses in your account, then you are better off not touching your own CPF monies.