Love it or loathe it, the CPF is something that all Singaporeans and PRs have to accept as a way of life here. While there have been many vigorous discussions about our CPF in recent years, we’ll leave that aside because we’re a finance & investment site. So let’s focus on how the CPF works for you at a personal finance level.

As an investment site, we focus mainly on one thing: How can we as investors earn higher returns on our money? Now there are many ways of investing to generate the returns you want but the first objective as an investor is to make sure your returns are at least able to hedge against inflation.

So what is the inflation rate in Singapore over the last ten years?

Source: tradingeconomics.com

As you can see, Singapore’s inflation rate over the last ten years has been mostly between 2-4% with an average of 2.74% from 1962 to 2015.

Earning 2-4% returns per annum from your investments shouldn’t be too hard at all. For example, S-REITs, which are considered relatively stable investments, averaged a dividend yield of 6.3% in 2014 – that’s excluding capital gains.

But if you’re absolutely risk averse and prefer investing in assets that can give you “guaranteed” returns, what is the highest return you can get “risk-free”?

Well, it’s obviously not your savings account which gives you an annual interest of less than a percent. So the highest return you can earn that is considered risk-free is the 10-year Singapore Government Securities.

Singapore Government Securities are AAA credit rated and is considered one of the safest possible investments for investors. So what is the average return for investing in the 10-year Singapore Government Securities?

Source: tradingeconomics.com

The rate has been trending down over the years and the average return is 2.91% from 1998-2015. As you can see, that’s not too fantastic and it just about matches Singapore’s average inflation rate. Based on these figures, investing in Singapore Government Securities won’t make you rich; it will just protect the value of your money from inflation.

So is there a way to earn higher returns risk-free?

But of course! (Which is the point of the whole article in the first place…) The money in your CPF earns a higher return and is generally considered risk-free as well.

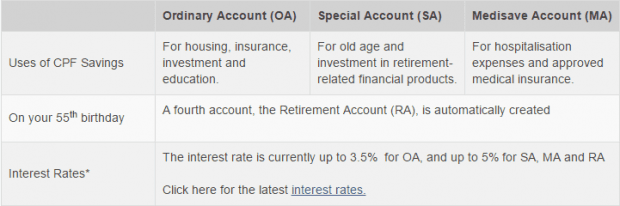

Here’s how it works. Your CPF contributions go into four accounts – the Ordinary Account, Special Account and Medisave Account, and when you turn 55, the Retirement Account.

- Your Ordinary Account earns 2.5% interest per annum or the 3-month average of major local banks’ interest rates, whichever is higher

- Your Special, Medisave and Retirement accounts earns 4% interest per annum or the 12-month average yield of 10-year Singapore Government Securities plus 1%, whichever is higher

Now the first $60,000 of your combined CPF balances earns an additional 1% interest. So technically, your Special, Medisave and Retirement accounts already earn you a risk-free return of up to 5% per annum. Not too bad.

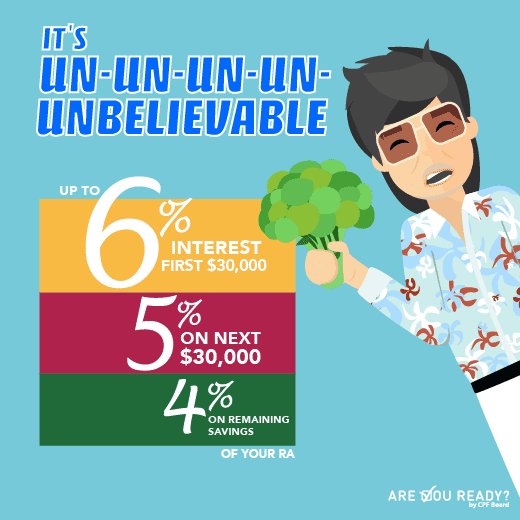

So how do you hit 6% returns risk-free as I stated in the title of this article?

From January 2016 onwards, the CPF will now pay an extra 1% interest per annum on the first $30,000 in your CPF accounts. This is on top of the additional 1% interest that is already paid on your first $60,000. So moving forward, your Special, Medisave and Retirement accounts will earn you a risk-free return of up to 6% per annum.

But there’s a catch…

This extra, extra 1% interest only applies to members aged 55 years and above. So unless you’ve lived long enough to remember Elvis and his shagadelic sideburns take over the world in your teens, then too bad. But if you are that old and gold, then congrats, you actually make a 6% risk-free return on your money (a portion of it anyway).

Of course, the other catch is that it’s your CPF money. But in any case, CPF or not, it is still regular interest earned every year for us, so why not? We take whatever comes along!