In September 2019, Interactive Brokers introduced IBKR Lite, a zero-commission trading platform. Other trading platforms like Charles Schwab, TD Ameritrade, E-Trade, and many others shortly followed suit. But how does a brokerage business survive without commissions? What’s the catch here?

In this article, we will analyze Interactive Brokers business model to find out more.

Business model

Interactive Brokers Group, Inc. is an electronic brokerage firm. Through their platforms IBKR Pro and IBKR Lite, investors can gain access to 135 markets in 33 countries and trade in 24 different currencies.

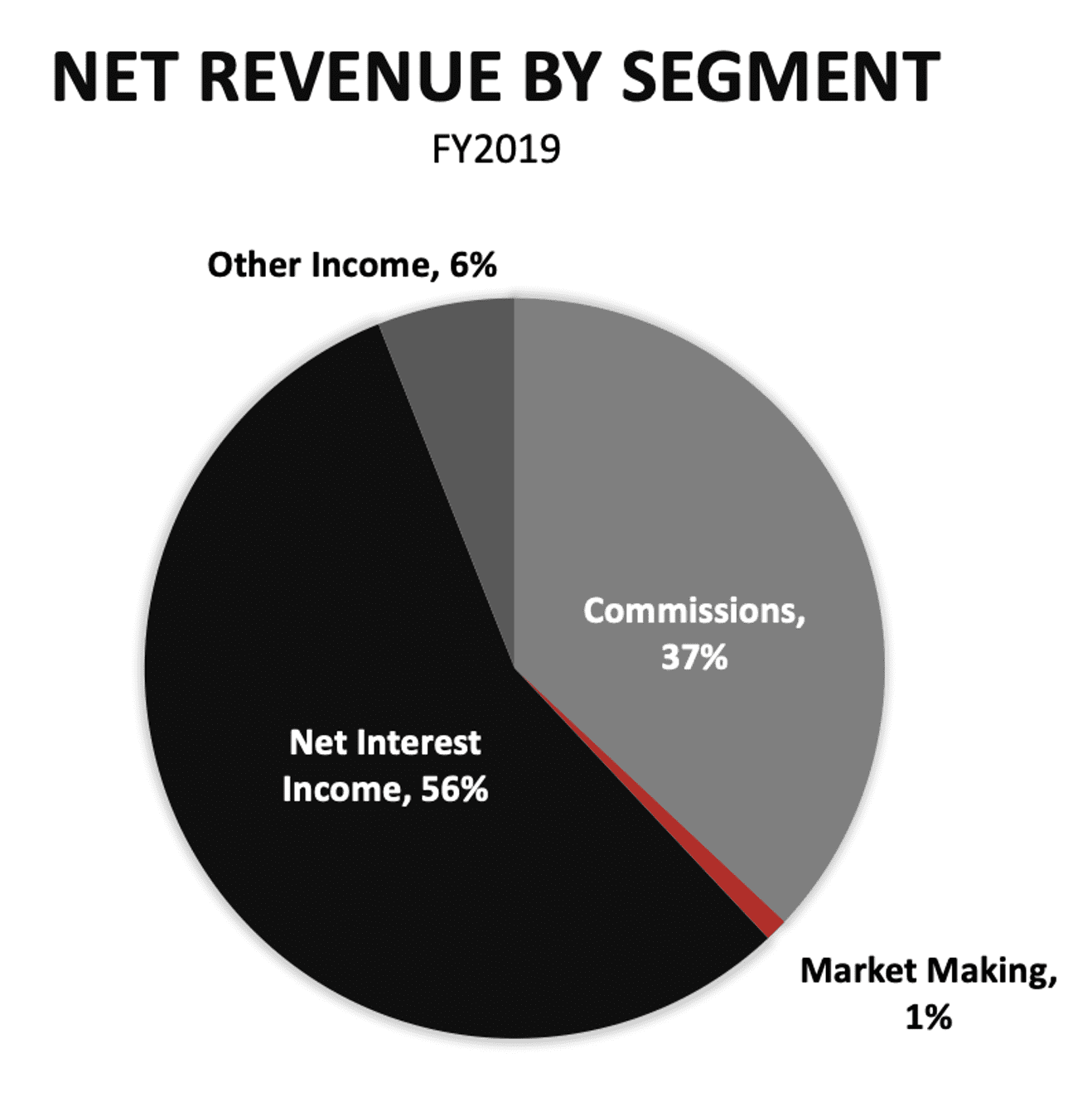

Interactive Brokers earned 93% of its $1.94 billion revenue in 2019 from commissions and net interest income. They also generate revenue from the payment of order flow though this is not one of their key business segments. However, I have included it so we have a good understanding of how they make money off their commission-free platform.

Trading commissions

Commissions still contribute greatly to Interactive Brokers’ revenue stream. Interactive Brokers takes a cut based on the number of shares traded or a percentage of trade value when we buy or sell stocks on its platform. For example, if you were to buy 1,000 shares in the U.S. market, Interactive Brokers will make a commission of $3.50. And if you are an active trader, it gets cheaper as you accumulate trading volume throughout the month.

In the past decade, revenue from commissions grew at a CAGR of 7.18%, from US$353 million in 2009 to US$706 million in 2019.

Payment for order flow

A business is not a charity organization. They have to make money one way or another.

Interactive Brokers gets paid $0.00026 for every dollar they route through market makers such as Virtu and Citadel on their commission-free platform, a payment for order flow. With enough volume, they could potentially generate hundreds of millions of revenue, as Robinhood has done.

Market makers are basically high-frequency traders. Their objective is to profit from arbitraging against your position. Let’s say you were to put in a limit order for a share at $50.00. If the market maker can find one at $49.80 in the market, they will sell it to you at $49.90 and pocket the difference. This may not matter to retail investors who have missed out on the optimal price they could get for their shares, but for professional traders with big accounts, that could mean thousands or millions of dollars in savings or profits left on the table.

Net interest income

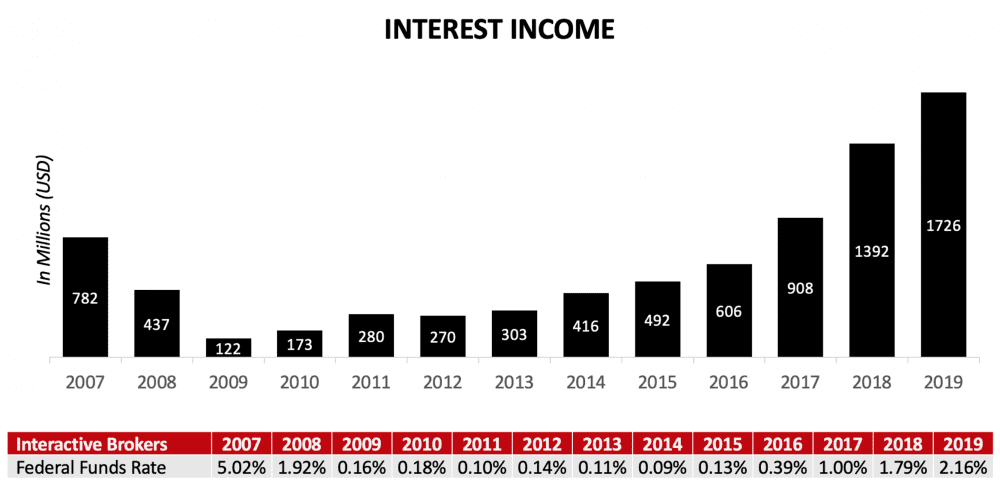

In the past, brokerages put a lot of emphasis on commissions. Today, it’s all about attracting as much assets as possible to generate net interest income, the main driver of revenue. And Interactive Brokers does this by taking your cash balance in your account to invest in government securities, deposit in FDIC-insured banks, and loan to traders to earn interest. At the same time, Interactive Brokers compensate you by paying you interest on your cash. This is what we call net interest income.

In the past 10 years, net interest income grew at a CAGR of 30.34%, from US$122 million in 2009 to US$1.73 billion in 2019. The ability of Interactive Brokers to generate net interest income, is affected by interest rates. When the Fed slashes interest rates, the company will generate a lower yield and earn a narrower spread on their assets. Conversely, in a hawkish environment, an increase in interest rates will boost their revenue.

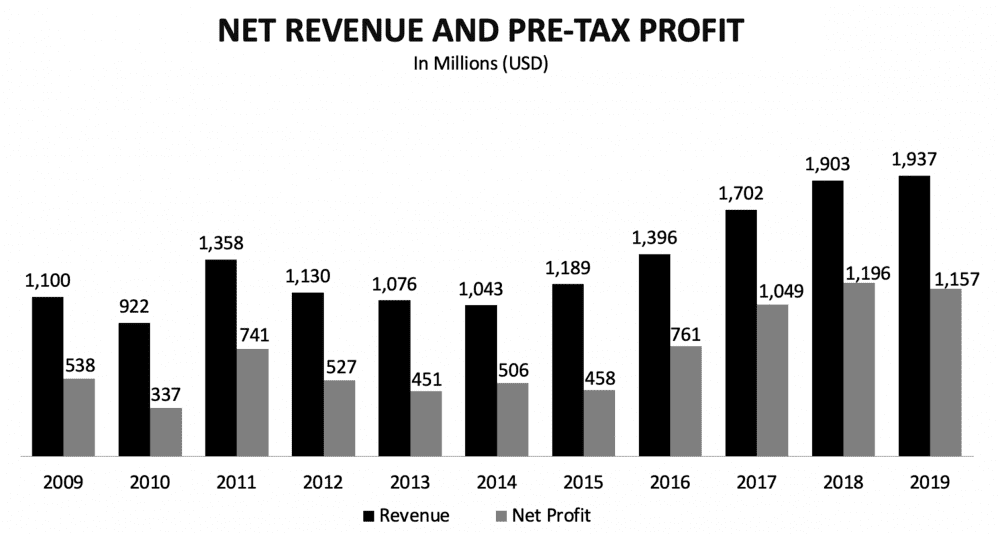

Interactive Brokers Group’s revenue grew at a CAGR of 5.82% to US$1.94 billion in 2019. The choppy growth of both revenue and net profit is due to the semi-cyclical nature of their business which is quite dependent on economic conditions. Commissions are driven by market volatility. The more volatile the market, the more active the traders, the more commissions Interactive Brokers will make.

Economic moat

Interactive Brokers is the low-cost leader of the industry. Management believes the value they offer is good enough to attract customers through the word of mouth. Over the past 10 years, the number of Interactive Brokers accounts have quintupled to 690,000 in 2019. Unlike most brokerage business, they do not spend a lot of advertisements.

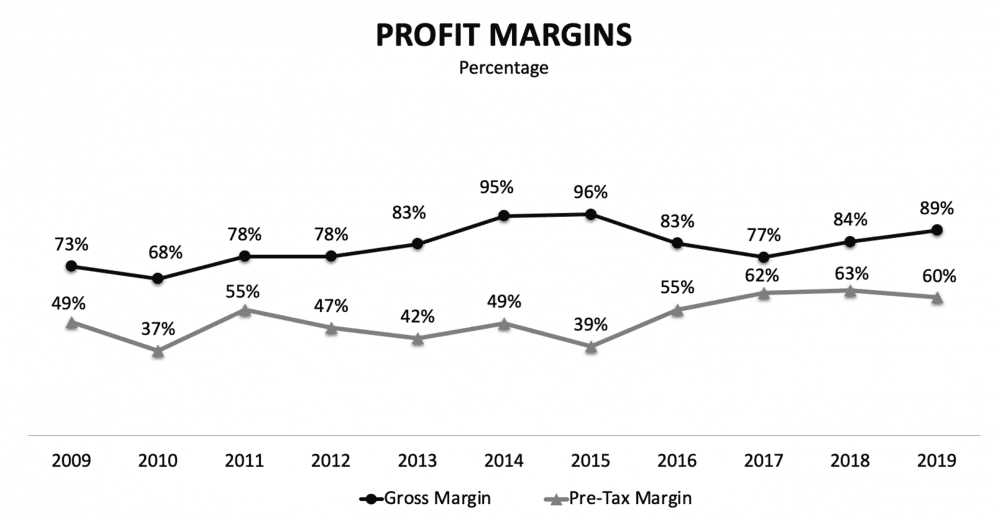

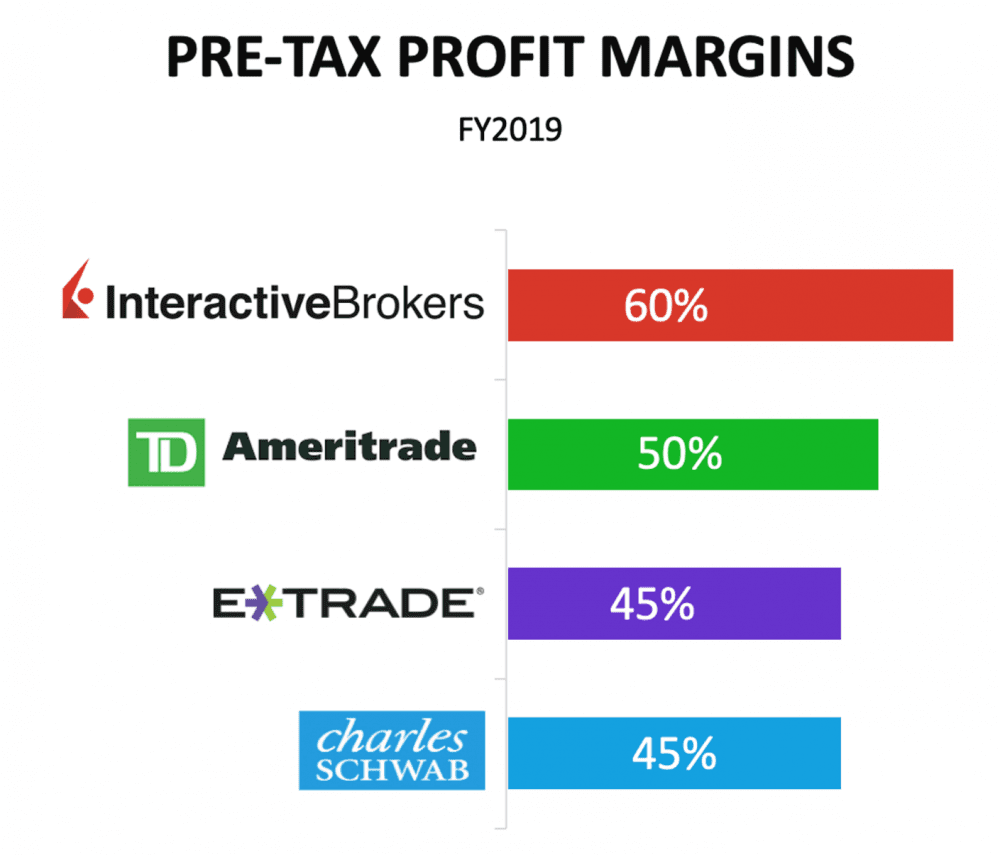

As an electronic brokerage, Interactive Brokers is able to spread its fixed costs over a growing number of accounts, achieving economies of scale. Interactive Brokers’ economies of scale contributed to the company’s margin expansion in the past 10 years. Pre-tax profit margins increased from 49% in 2009 to 60% in 2019.

Among its competitors, Interactive Brokers has the highest pre-tax margins in the industry. This gives the company a lot of room to slash prices to compete with their peers.

Right after Interactive Brokers launched their zero-commission brokerage — IBKR Lite — the industry went through a wave of consolidation. Charles Schwab merged with TD Ameritrade and E-Trade was acquired by Morgan Stanley. Unlike Charles Schwab that has spent years growing its wealth management business, some brokerage firms like E-Trade will have a hard time offsetting the loss in commission revenue.

This will not be an issue for Interactive Brokers because they are serving a niche market of sophisticated traders who are attracted by the company’s offers of the lowest commission, the lowest interest on margin, and the highest interest on cash.

A company like Robinhood will not be much of a threat to these giants in the industry because investors with sizeable assets tend to seek professionals from these firms to manage their wealth.

Risks

Interactive Brokers has good risk controls in place. Processes are automated (e.g. margin positions are closed immediately if the traders fail to top up their accounts.) However, from time-to-time they will be hit by unexpected movements in the market.

In April, Interactive Brokers lost US$104 million when oil crashed to negative US$37. A lot of their traders who were long oil got caught and instead of waiting for the price to recover, Interactive Brokers decided to close out the positions and compensate the trades for their losses below zero. The market is capable of pulling off crazy stunts that no one can be prepared for so it’s prudent of us to expect Interactive Brokers to meet such challenges.

The fifth perspective

The brokerage industry is undergoing a wave of consolidation triggered by Interactive Brokers’ move to offer zero-commission trades. This business model requires a large number of customers and high volume of trades, leaving consolidation as the only way forward for many smaller firms, especially those reliant on trading commissions.

Interactive Brokers and other larger brokerage firms like Charles Schwab and Fidelity will emerge as even more dominant players in the industry after the wave of consolidation passes, making it harder for new entrants to gain a foothold in the market.

In India a zero brokerage business called ZERODHA has survived and thrived. It continues to grow rapidly and the full service bank run brokerages are being forced to cut their own brokerage. For now the discounted brokerage offers of banks are based on volumes transacted.

Hi RV,

Thanks for the insights.

Zero-commission is definitely a threat to discounted and full-service brokerages. This is how I see the future will play out for this industry. Generally, retail investors will flock to apps like ZERODHA cause of the no-cost, user-friendly features suitable for beginners with small capital to invest. Discount brokerages will still exist but they will cater to sophisticated traders to get the best possible price. And, lastly, full-service brokerages will service high net worth individuals.

Very good article! I recently choose IBKR(through introducer broker) as my primary international broker after exploring a few options given their sizable and established company, while still offering super competitive rates. Enjoying it so far as I wouldn’t have to worry about their stability or hassles to deal with in the event if broker go bust.

Please correct your article. IBKR only takes payment for order flow on Lite clients. In fact for Pro users IBKR has one of the best price improvement in the industry. Read their sec rule 606a disclosure.

Hi Anonymous Cow,

Yes, the article lists the various revenue sources that Interactive Brokers (the company as a whole) generates which includes trading commissions (IBKR), PFOF (IBKR Lite), and net interest income.