The future will look different. In the last few years, the cumulative effects of COVID, political and social unrest, war and economic disruption have tilted the world on its axis, so that the next few years will look very different by comparison. In the previous two decades, growth and stability seemed almost guaranteed: that’s no longer the case.

Looking ahead, we see three key themes that will dominate.

1. High secular inflation

Having not been a problem for 20 years, inflation is back with a vengeance. We are transitioning from an era of price stability to one of higher, more structural inflation. Globally, prices rose by 8.8% in 2022, and in 2023 is currently projected to come in only slightly lower, at 6.5%. Although cost pressures eased a bit by the end of 2022, they seem likely to remain at an elevated level for the next few years. A key feature of this is due to the lag effect of postponed wage awards being made as companies struggle to attract and retain staff.

2. Deglobalisation

In simplified terms, whilst globalisation leads to lower costs, deglobalisation has the opposite effect — and is now a real feature of the global economy. This was illustrated by the recent 2023 World Economic Forum’s theme of ‘Cooperation in a Fragmented World‘. The first signs of this were the UK’s disengagement from the EU after Brexit in 2016. At the same time increased trade tensions between the U.S., and pretty much everywhere else – but notably China – resulted in the Trump administration’s trade war, followed by allegations of cyberwarfare and corporate espionage. In 2020, COVID caused a further locking down of borders and trade flows, whilst Russia’s invasion of Ukraine in 2022 highlighted the strategic risks of ‘offshoring’ critical parts of supply chains.

A new U.S. President in 2020 made no difference to this increase in protectionism: the recent U.S. CHIPS act is one of latest examples of official efforts to secure U.S. semiconductor supply chains, forcing China to find suitable replacements.

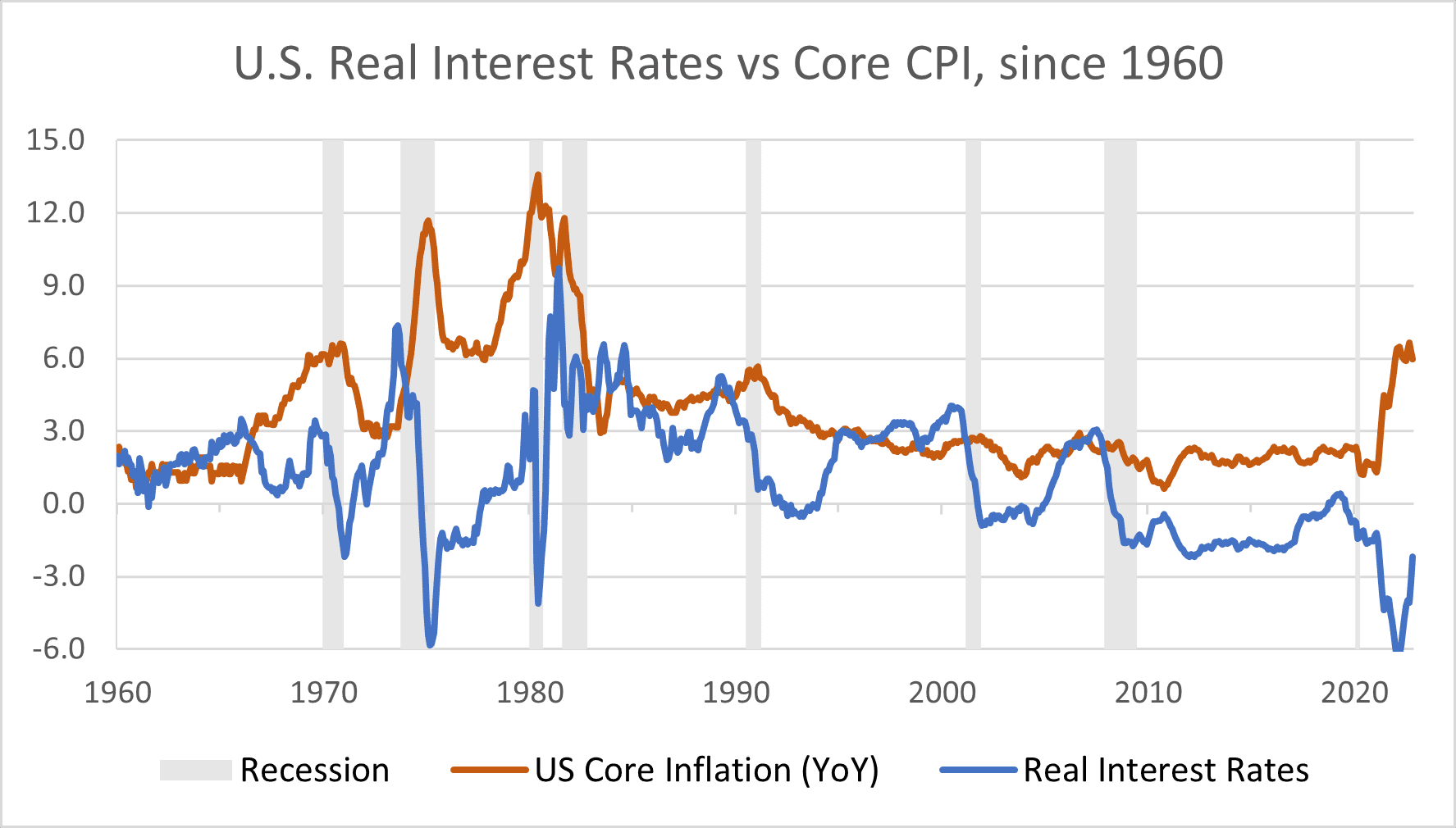

3. ‘Higher for longer’ interest rates

A by-product of the above two themes, interest rates that are ‘higher for longer’ will be the unavoidable third thematic. Central banks traditionally use interest rates as their main tool to curb inflation. In the 1970s, the U.S. Fed raised interest rates to a peak of 13% before inflation numbers started to fall. The same could be seen in the 1980s.

Although we are witnessing a gradual slowing of price and cost growth in recent inflation data, there is always the question of whether interest rates are high enough to really put the inflation genie back in its bottle. The lessons of history are not encouraging since they show interest rates must at least exceed inflation before it starts to revert, and that inflation is usually more persistent than predicted. Since in the U.S., inflation is currently running at 6.5% compared with the current Fed rate of 4.25%, interest rates seem likely to be higher for longer in order to eliminate that gap.

Where do we go from here?

With such a sea change in global conditions, investors might be thinking of tossing out their investment playbooks and rethinking their strategy. Some asset classes that rely on ‘cheap money’ and low interest rates, will struggle. So will those that rely on borrowed money: they need a higher return just to cover the increased cost of debt.

That said, the tried and tested fundamentals have held firm through many cycles, and this time is unlikely to be any different.

Establishing the groundwork

The complexities of investing in an increasingly noisy world can be reduced by sticking with actively holding on to a few tried and tested principles:

1. Investing should be for the long term.

2. Invest in good quality businesses. For example, quality could mean companies that deliver consistently high returns on invested capital (ROIC).

3. Cash (flow) is king. This is increasingly important when market valuation multiples are falling – profitability takes priority.

4. Diversification is key. The 60/40 portfolio got hammered in 2022, but that’s the only the third occasion that this has happened since 1930. (In the span of 90 years.) Security and fund selection seems likely to be more important in a deglobalizing world where ‘growth’ is likely to be more challenging.

5. Don’t be greedy. Focus on long term compound growth. Such compounding was referred to as the eighth wonder of the universe: ‘Those who understand it, earn it. Those who don’t, pay it.’

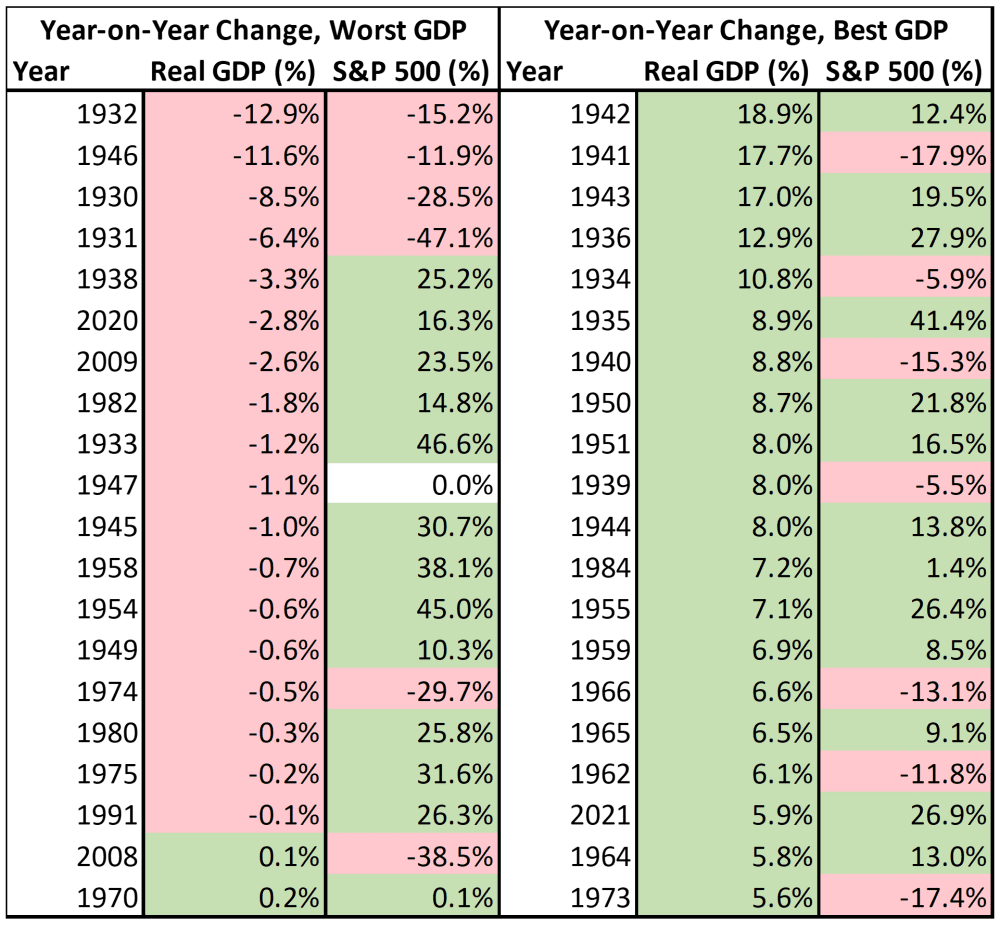

6. The market is not the economy. Invest in good businesses, not GDP numbers. Even for the years in the U.S. with the 20 worst GDP contractions, the S&P 500 posted double digit returns at a counterintuitively high rate. The same can be said likewise — the best years for the economy also resulted in declines in the S&P 500, but with less frequency of occurrence.

Outlook for investment growth

With central banks reversing the money printing presses, stock markets have seen the tidal flows of money reverse too.

One of the obvious knock-on effects in terms of tightening monetary policy is the end of the TINA (There Is No Alternative) strategy. ‘Low or no’ interest rates meant that stock and bond markets were a great alternative to leaving the money doing nothing in the bank (or under the bed). Share prices were bid up to successive record highs, companies leveraged up their balance sheet, and growth was easy.

With higher costs of capital, a slowdown in demand, and increased operating costs, the task of finding investments that outpace these is going to be a lot harder.

Winners and losers

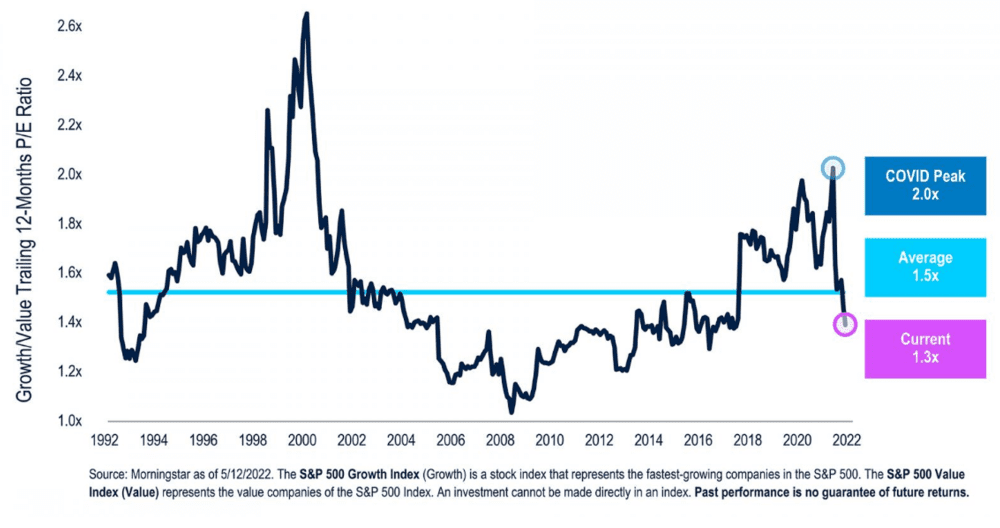

The top performing stocks, asset classes and sectors of the past decade might no longer be the winners for the next. Tech stocks, private equity, Start-ups and growth focused companies have since been hammered. In a world that now values cash flow more than it did, the absence of that for any company or start up pitch will be seen as a no-no. Valuations will get pegged back. It’s for this reason that value made a relative comeback in 2022, outperforming growth – with the growth-to-value valuation comparison now below its long-term average.

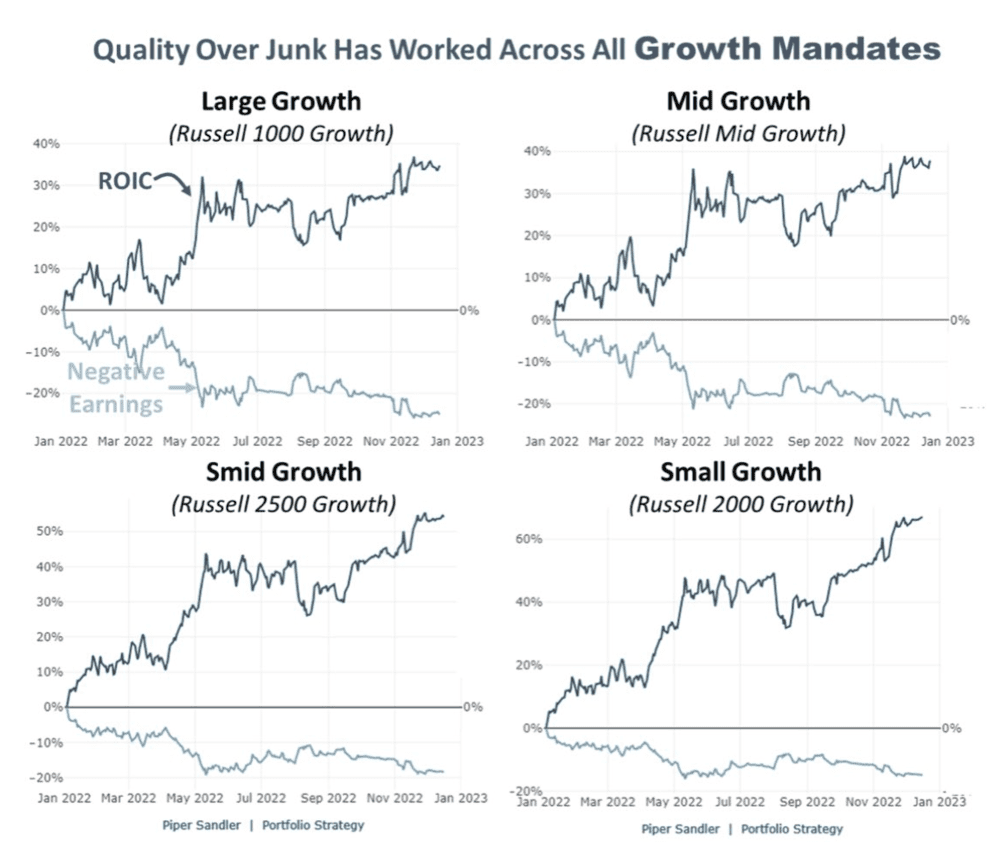

That means, for the time being at least, ensuring you focus on quality companies with healthy balance sheets that are able to sustainably grow free cash flows would be the safe(r) bet. In addition, selecting from that list, companies that have a high ROIC also adds to portfolio security.

A basket of stocks with high ROIC and avoiding those with negative earnings has generally outperformed in 2022.

Bonds are back

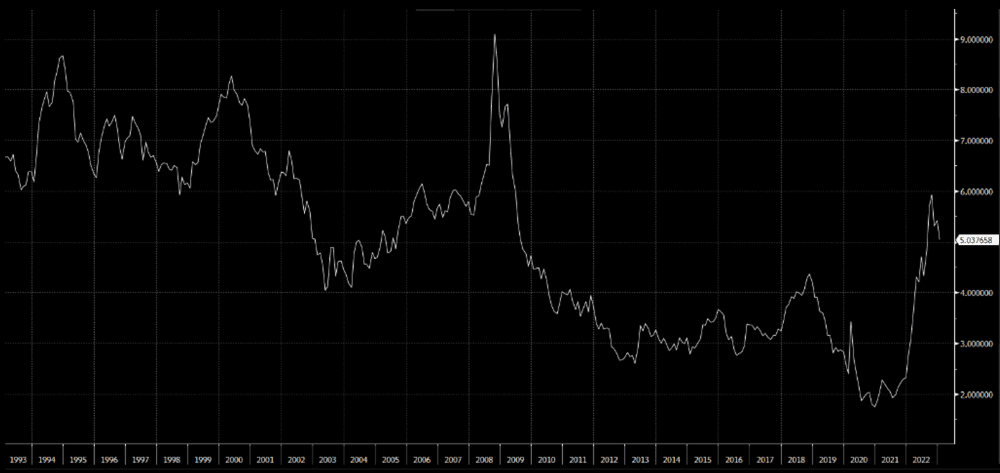

With rising interest rates, bond yields have gone considerably higher (i.e. their prices have dropped). At the end of 2022, U.S. 10-year Treasury yielded 3.62%, whilst the two-years yielded 4.41% (compared with 1.52% and 0.55% respectively at the start of the year). U.S. corporate investment grade bond yields have also surged, having risen from 2.0% to 5.0%. Bonds now look a lot more attractive than they have done at any point in the last 10 years.

Since yields have become attractive again, investors have a higher opportunity cost in terms of allocating to stocks against some of the relatively lower risk but higher yielding bonds.

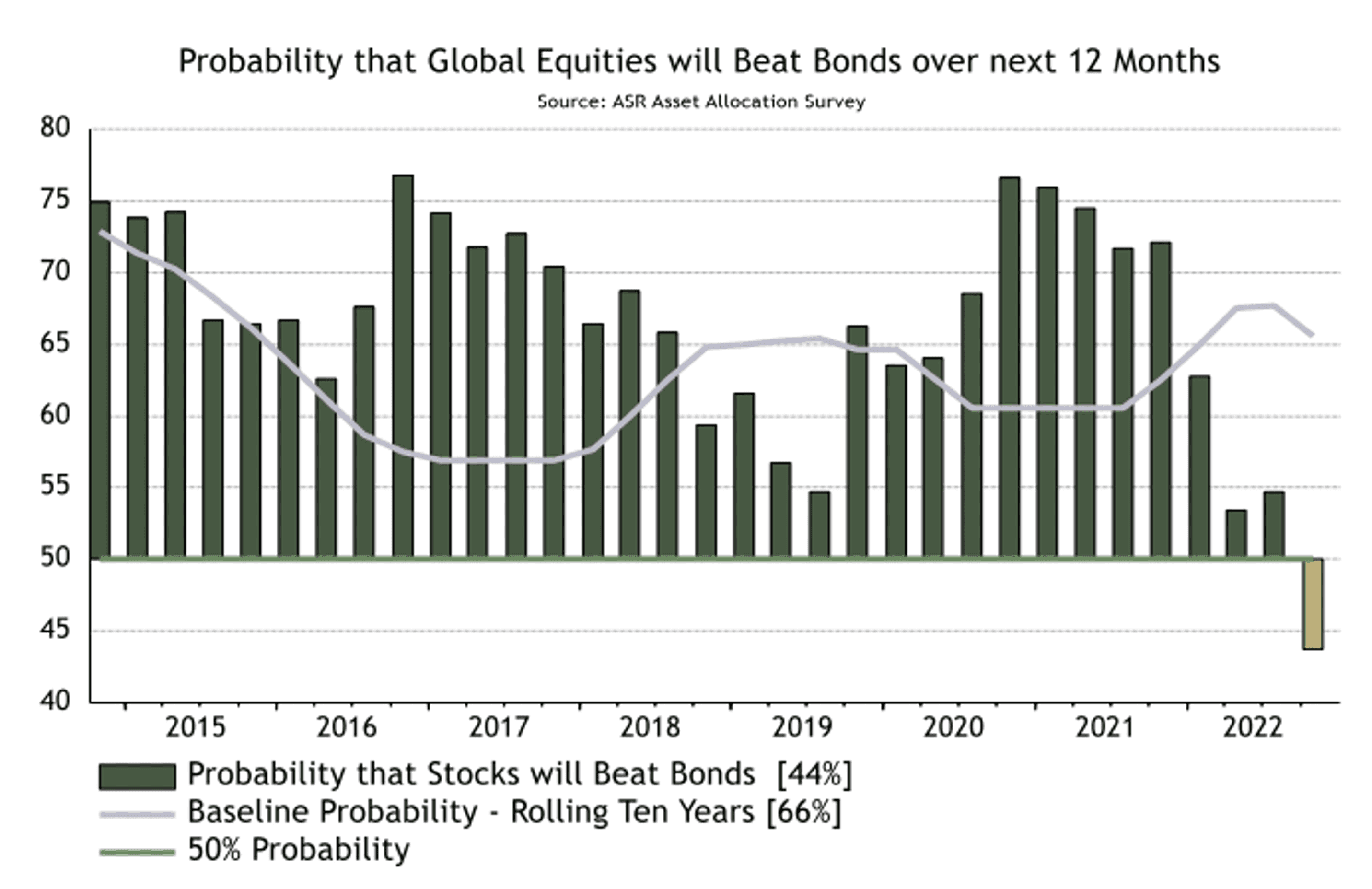

A recent survey of asset allocators is a good illustration of that shift in relative attractiveness. For the first time in 7 years, sentiment implies that the probability of stocks beating bonds was now below 50%.

Active vs passive?

The other interesting aspect would be the ongoing debate between using an active vs passive fund: pay an expensive manager or just buy a cheap index ETF.

By and large, passive has outperformed active over the past decade – and this had the reflexive effect of outflows from active managers into passive investments, further reinforcing that cycle.

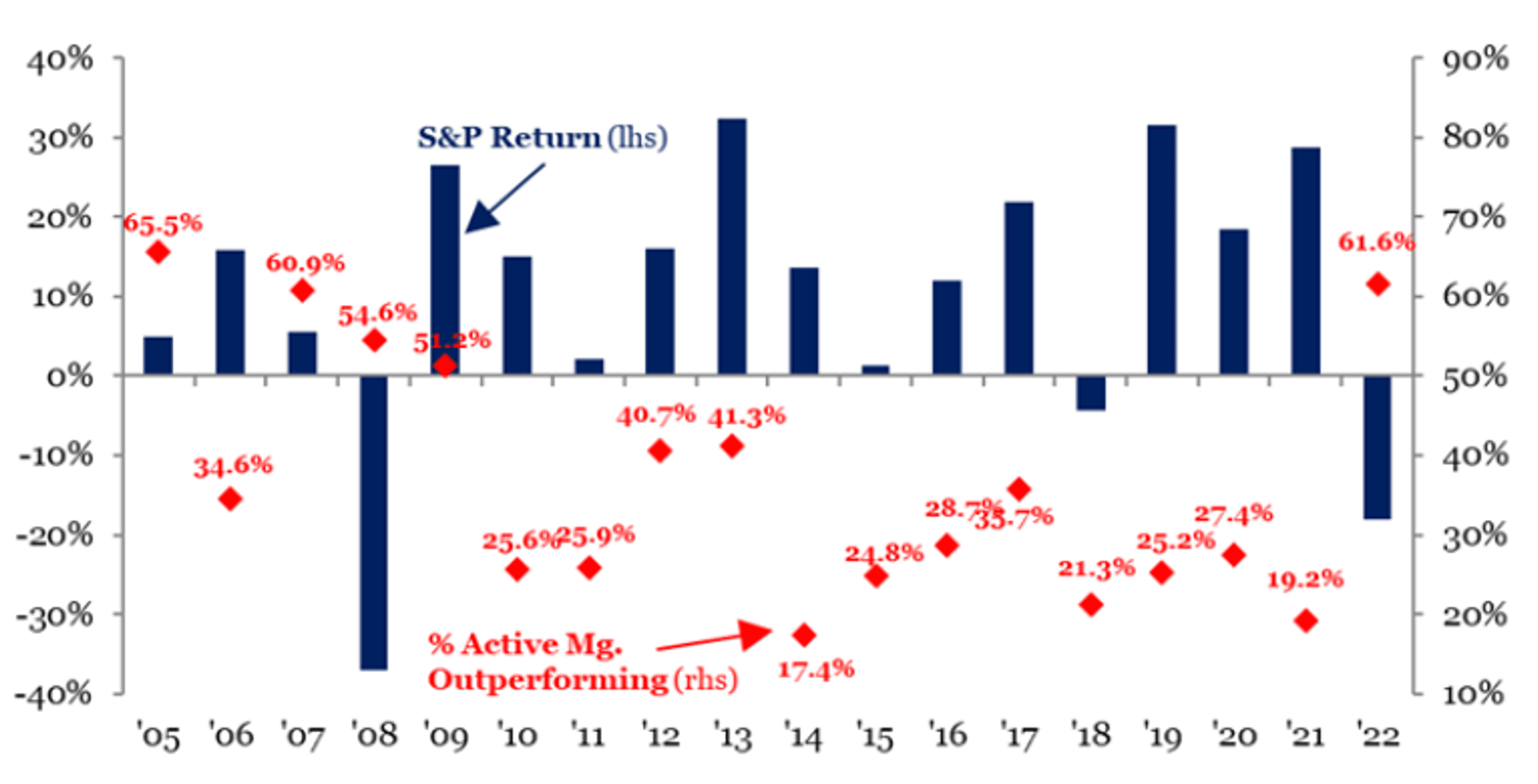

With the end of quantitative easing, passive funds dominated by a handful of mega cap stocks sucking in boatloads of liquidity could come into question. 2022 was a definitive year for active fund managers in terms of outperformance against passive instruments. 62% of large cap managers outperformed the S&P 500 which is reminiscent of active managers outperforming the S&P in 2009 (or could simply be a reflection of the fact that even a broken clock is right twice a day).

As the range of passive strategies has multiplied over the last few years, investors can strike a balance by switching to include an equal weighted index in their portfolio, as this would reduce the risk of active management myopia (and underperformance), as well as negate potential underperformance from megacaps such as FANGs. The S&P 500 Equally Weighted Index outperformed the S&P 500 by at least 6% in 2022.

The music is slowing, but you can still dance

2022 will go down as a year in which the investment paradigms shifted: big global geopolitical challenges combined with local ones. Governments and investors alike all struggled to find the right mix, proving that a reactive approach achieves nothing other than exhaustion. Growth might not hold steady as before, the previous decade’s winners might get replaced, biases will be confronted, and portfolio resilience tested.

However, the tried and tested fundamentals of investing still hold true. The effect of new dislocations, as the world struggles to find a new equilibrium could uncover new opportunities as well.