Photo credit: DonkeyHotey

- Warren Buffett shares his investment wisdom in his recent 2014 Annual Report and why market volatility is not necessary risk

- Example of SingTel’s performance over 10 years to illustrate periods of ideal market conditions and high volatility due to recession

- Five other conditions for investors to benefit from volatility in the market and your edge over professional investors

One of the most admired value investors of our times has recently issued his widely acclaimed and read annual report after 50 years at the helm. As we will be celebrating 50 years of Singapore’s independence with various activities, let us turn out attention to the wisdom of Warren Buffet, the self-made investment billionaire that is worth over $71 billion as of 04 March 2015 according to Forbes.

Billionaire rankings in the world wax and wane according to the volatility of the stock market and Warren Buffet is now number 3 in the world up from number 4 last year. He has consistently stayed at the top of heap and if you have read his newsletter you will know that such minor changes in rankings does not matter. The point to note that it is his timeless and superior wisdom coupled with skillful execution that led him to where he is now and we would benefit from a few of his choice advice in this article extracted from his 2014 Annual Report to Shareholder. As a bonus, Warren Buffet’s long term partner, Charlie Munger also added his perspective in this letter.

While commoners like us would never be anywhere near his rankings or wealth, I believe we can benefit from his wise words. A good understanding of his investment wisdom followed by steadfast implementation would lead to steady accumulation of wealth and eventually the final destination of financial independence. Or at the very least, it would prevent disastrous investment results.

I believe that the most famous Warren Buffet piece of advice is that the first rule of investment is to never lose money and the second rule is not to forget the first rule. I am not quoting it verbatim but the gist is there. So the very obvious question is how do we get there.

Every investor in the world wants to make money and nobody wants to lose money. Obvious and simple as this self-evident truth is, it is very difficult to achieve in practice and maybe the next segment will give you an idea. It may not make you rich overnight but if you follow it diligently over time, you will reach your financial goals.

Never Confuse Volatility with Risk

I think this is one of Warren Buffet’s greatest contribution to the investment community today. If you open any advanced financial textbook, you will see that mainstream financial teachings equate volatility with risk. There are various measures of volatility such as standard deviation and value at risk which measures how far share prices move over time and thus determines how risky that particular security is. This is actually quite misleading for the common investor and a major cause of wealth dissipation for them.

This erroneous concept of risk had been accepted and misled a significant portion of the investment community (for various reasons but the appearance of authority is actually one of them as they are backed by top business schools) but it is this same volatility that actually provides us with opportunities to grow our wealth exponentially.

I quote from the guru himself below from his annual report:

“Stock prices will always be far more volatile than cash-equivalent holdings. Over the long term, however, currency-denominated instruments are riskier investments – far riskier investments – than widely-diversified stock portfolios that are bought over time and that are owned in a manner invoking only token fees and commissions. That lesson has not customarily been taught in business schools, where volatility is almost universally used as a proxy for risk. Though this pedagogic assumption makes for easy teaching, it is dead wrong: Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.”

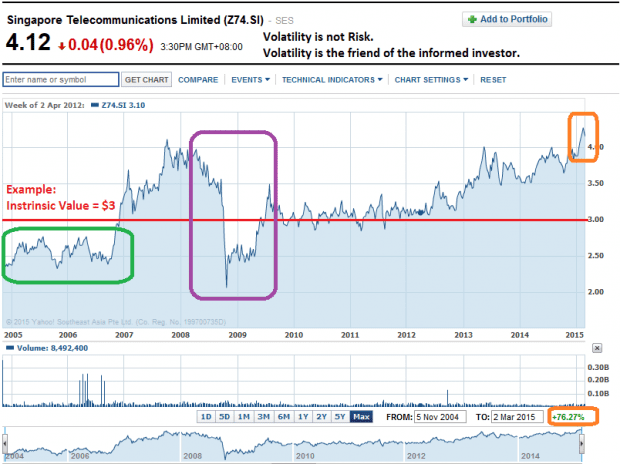

SingTel Case Study

If you were to consider the risk of an investment deeply and free from the influence of conventional wisdom, you will come to realize that the only true risk in investment comes when there is a permanent loss in capital. Let me give you a local example to anchor this concept which can be quite abstract. Singapore Telecommunications or commonly known as SingTel to the wider public is an example of a wonderful business. Suppose that after doing your homework, you decide that it is worth $3 per share in 2005 and started to accumulate your shares as it is trading below its intrinsic value.

Source: Yahoo Finance

We can look at the 10 year chart of SingTel above to illustrate a point.

Green Box – Ideal Market Environment

Let us look at the green box from late 2004 to early 2007. This is generally known as the post-Sars crisis period (the Asian pandemic that peaked in 2003 which dampened investment sentiment with gloomy predictions) and before the bursting of the US housing bubble which led to the Credit Crunch triggering the collapse of Lehman Brothers and the start of the Great Recession.

So suppose you did your homework and found that SingTel was worth $3 during this green box period with periodic review. Will it matter to you if the market decided to price SingTel at say $2.40 when you bought it in November 2004 and it went up to $2.77 in July 2005 and then dropped to $2.33 in October 2005?

If you labor under the assumption that this volatility is risk and/or you do not have the concept or conviction of its intrinsic value at $3, you might think that SingTel is risky and promptly sell it after holding it for one year. This is an excellent example of how people squander their money even during a period of conducive market environments and how other people make money.

For the astute investor who understands that volatility is his friend, he would have accumulated SingTel on a monthly basis, diverting a portion of his monthly income to SingTel. The price of SingTel, regardless of whether it is at $2.77 or $2.33, would not have mattered to him. He would continue to buy SingTel as long as it is below the fair price of $3 as he will be accumulating his wealth by buying a wonderful company at a fair price.

For the sake of simplicity, assuming that the fair price for SingTel remained at $3 in October 2007 and the market volatility brought it up to $4.02 for various reasons. One excellent reason, which is clear on hindsight, is that this is a period of excessive confidence before the bubble burst and a lot of liquidity came as a result of the US mortgage market securitization. This liquidity ended up in the global equity market in search of higher yield pushing up equity prices especially blue chip companies like SingTel beyond its intrinsic value.

At this point, we should recall the words of famed value investor and Warren Buffet’s mentor, Ben Graham, words which Warren Buffet quoted in his annual report and reproduced here:

“As Ben Graham said many decades ago: ‘In the short-term the market is a voting machine; in the long-run it acts as a weighing machine.” Occasionally, the voting decisions of investors –amateurs and professionals alike – border on lunacy.’”

At this point, the rational investor has only two choices. One is to sell it to the lunatic market at $4.02 and earn 76% of his return in four years or he can continue to hold a wonderful company in his portfolio and enjoy the periodic dividends payment. Above all, he would not seek to add to his exposure at this high prices.

Advantage of Retail Investors over Professional Managers

In this first instance, he made use of the volatility of the market to realize his accumulated wealth into cold hard cash and stay on the sidelines until better opportunities came along. One point to note is that only retail investors can sit on the sidelines. Most professional managers like mutual funds do not have that luxury as their investment mandates force them to stay invested with 95% of the funds in equities even when the market is overvalued in 2008 and even if they realize it as such.

The rationale is that fund managers are being paid to invest and it is not acceptable for them not to stay invested at all times. Hence it is acceptable for them to pay for overvalued equities and lose money, as long as they don’t lose more money than the average loss of their benchmark. In other words, if your mutual fund manager loses 10% when the market loses 50%, he probably deserves an award for it.

The professional mutual fund manager that seeks to protect the value of his clients’ funds by staying on the sidelines might be lauded in private for his audacity but would be quickly shown the door. He has just broken the rule no matter how convincing or eloquent he might be in acting in the best interests of his clients. The only recourse is for the investor to fire the fund manager by withdrawing his funds, provided that he has the foresight to see the recession coming.

Purple Square – Recession and Period of High Volatility

Now back to the topic of volatility being your friend, the period of the purple box indicates the worst of the Great Recession effect on the market. The deep plunge in SingTel stock from September 2008 of $3.57 to the low of $2.06 in October 2008 looked as if the collapse of Lehman Brothers meant that we had to throw away our mobile phones and broadband internet connection.

This is actually a market panic which should not be confused with the meltdown of SingTel’s business model. Even if the US is burning, Singaporeans will still have to make calls and surf the Internet as an integral part of our modern lifestyle. Suppose for the sake of simplicity, your calculations show that SingTel is still worth $3, then you should be accumulating your SingTel shares once it dropped below $3 and even more at $2.06 which is a godsend! This is actually free money, the market playing Santa Claus early in October for the astute investor to seize the opportunity to enhance his assets.

Therefore this period of high market volatility is an excellent point for investors to buy and hold a wonderful company at a wonderful price for long-term asset accumulation. If the earlier investor chose to keep his SingTel accumulation instead of selling at $4.02 in October 2007, the concept that volatility is not risk would give him comfort and strength to hold onto his investment. It would fortify him from selling it at a loss under the influence of fear and accumulate as much as he is able from a position of confidence.

Additional Conditions for Investment Success

As we have seen in the SingTel example above, volatility is actually the friend of the astute investor as it allows him to pick up undervalued stocks cheaply. However in order to benefit from volatility, this is conditioned upon the presence of these five skills below:

#1 Know the difference between price and value

Warren Buffet reminded us once again to never pay for an investment above its intrinsic value. This is common sense but really worth repeating and this is something that most investors are guilty of violating. This is some food for thought from Buffet again below:

“I can promise you that long after I’m gone, Berkshire’s CEO and Board will carefully make intrinsic value calculations before issuing shares in any acquisitions. You can’t get rich trading a hundred-dollar bill for eight tens (even if your advisor has handed you an expensive “fairness” opinion endorsing that swap).”

Just like the common sense trading rule is to buy low and sell high, most traders actually do the opposite. They buy high and sell low. This is why only a sliver of traders are successful. They are skilled enough to actually buy low and sell high.

The only way to know the intrinsic value of the stock is to do your homework thoroughly and there is no shortcut for it. It is likely taking an exam only that you won’t know the date for it. The volatility of the market will test your conviction from time to time and if you fail to do your homework properly, you will not have the conviction to hold onto your holdings and end up paying for it dearly.

#2 Patience when waiting for the right price to enter a stock

I think this is self-explanatory. After knowing the intrinsic value of the stock, if it is trading above it, do not enter even if it were to go up later on fear of losing out. For inspiration, let me quote how Charlie Munger described the patience of Warren Buffet when he was just starting out:

“And, finally, even when Berkshire was getting much better opportunities than most others, Buffett often displayed almost inhuman patience and seldom bought. For instance, during his first ten years in control of Berkshire, Buffett saw one business (textiles) move close to death and two new businesses come in, for a net gain of one.”

In the future, when you find your patience is wearing thin, reflect on the above-mentioned sentence on how patient Warren Buffet is and how far it got him.

#3 Don’t use leverage to hold during periods of volatility

If you want volatility to be your friend, you have to use cash for your purchase. It is simple as that. Leverage may boost your return but it will also kill you when things go wrong. Even if you are very convinced after doing thorough homework, your broker is still working on the assumption that volatility is risk especially when it is going against you. So it is advisable to build you wealth the old-fashioned way.

#4 Buy and hold over an extended period of time. Know the difference between trading and investing

While trading may make you rich, investment is still the true manner for companies to build wealth in society. You can trade the shares of a property developer within days but it actually takes 3 to 5 years for the property to be built. When investing, think of yourself as a part-owner of the company as if you are buying a HDB flat with a minimum holding period of five years for a local reference. Hence you should not buy a share on a whim as much as you will be buying your flat where you will be staying for at least five years. Buy the shares as if you are part of the effort to build a new mall or housing district in Singapore.

#5 Cut your losses when you realize you’ve made an investment mistake. Everyone makes mistakes, even the legend himself, the key is to acknowledge your mistake and accept the loss

I have heard too many stories from friends of how their elderly parents are holding onto some underwater stocks that they should have sold a long time ago. While it makes sense to ride out the volatility in the market, there is a difference holding the security because given time the market will realize it is wrong and come to its senses and holding it because you are wrong but not willing to admit it.

Sometimes the difference is hard to tell because emotions are involved and the legend himself is not immunized from it. So you are not alone if you ever fall into this trap of self-illusion. Not many people will admit it and especially in front of billions of audience as Warren Buffet did bravely and this is indeed a valuable and rare lesson for us:

“Even with Charlie’s blueprint, I have made plenty of mistakes since Waumbec. The most gruesome was Dexter Shoe. When we purchased the company in 1993, it had a terrific record and in no way looked to me like a cigar butt. Its competitive strengths, however, were soon to evaporate because of foreign competition. And I simply didn’t see that coming. Consequently, Berkshire paid $433 million for Dexter and, rather promptly, its value went to zero. GAAP accounting, however, doesn’t come close to recording the magnitude of my error. The fact is that I gave Berkshire stock to the sellers of Dexter rather than cash, and the shares I used for the purchase are now worth about $5.7 billion. As a financial disaster, this one deserves a spot in the Guinness Book of World Records.”

When you make a mistake, admit that you made a mistake and cut your losses. Lying to yourself will be the biggest mistake and you might end up holding onto a loser into your grave when the money can be put to better use when you are alive.

#6 Invest in a quality company instead of a cheap company

Again we have Warren Buffet below:

“From my perspective, though, Charlie’s most important architectural feat was the design of today’s Berkshire. The blueprint he gave me was simple: Forget what you know about buying fair businesses at wonderful prices; instead, buy wonderful businesses at fair prices.”

Warren Buffet also gave the cautionary tale of how the conglomerate model in the 1960s encouraged CEOs to buy and combine cheap (let just say that they are cheap for a reason) companies which failed ultimately.

Conclusion

We have came to the end of the article and I must first pay my tribute to the master investment guru Warren Buffet himself. All these are not my ideas. I have merely read his outstanding Annual Report and interpreted his words and put it into local Singapore context for local readers to relate better to. I would advise you to read his original Annual Report and gain further insight from it. So all the best to your investment road ahead and hopefully you can come out ahead in the years to come.

Dear ” The Fifth Person”,

Your post about wisdom in investing has given me some refreshment and reconfirmation about “How to Invest” in a wise way.

I have lost a lot of money in stock trading in the past 20 years, its not that I don’t know the Rules but its because I had not clearly understood and had never put the Rules into practice.

Hence forth I shall put the rules into practice and revert from losing trades to winning results.

Thank you for sharing

Rosalind Tay

Hi Rosalind,

Thank you for the kind words. We’re glad we can help in whatever way we can!