‘Heads, I win. Tails, I don’t lose much.’

That was the quote by Monish Pabrai, author of The Dhandho Investor that came to my head when I was looking at GameStop.

The problem

GameStop Corporation is one of the largest gaming retailers with 5,800 stores peppered around the world. The share price of the company has been on a decline for the past six years as GameStop faces digital disruption. Today, gamers don’t have to step out of their house to get their consoles, accessories, and games. Everything can be purchased online — you can buy your gaming electronics on Amazon or purchase your games from the PlayStation Store or Xbox Game Store and download them straight to your console.

When you pair structural decline with the end of a gaming console cycle, you’ll get a taste of bitter performance and a bold flavour of negativism surrounding GameStop. Sales tend to erode over time towards the end of a gaming console cycle as consumers hold back on spending, awaiting the release of the next generation of gaming consoles (in this case, the PlayStation 5 and Xbox Series X which is due for release towards the end of 2020).

This is the cyclical nature of the gaming industry. Once every seven years or so, the new release of new gaming consoles — almost like a tide that raise all boats — drive the sales of accessories, and new and pre-owned games for GameStop.

As you can see from the table below, the release of the PlayStation 3 and Xbox 360 in the previous console cycle doubled GameStop’s new and pre-owned games sales from 2006 to 2011 before falling off in 2012.

Source: GameStop annual reports

However, things are a little different for the current console cycle (PlayStation 4 and Xbox One) as the rise of digital games disrupted GameStop’s new and pre-owned game segment which has been on a downward trend since.

Source: GameStop annual reports

From the console manufacturer’s perspective, you can also see that the shift towards the digital download of games is happening progressively for the PlayStation 4 (PS4). Although bears like to focus on the fact that digital game sales exceeded physical game sales for the first time in Q1 2019, if we look at it from an annual perspective, you can see that change is happening at a slower pace. The PS4 full game software digital download ratio increased from 32% in FY2017 to 37% in FY2018. At least for now, gamers still prefer physical over digital.

Source: Sony Q1 2019 supplemental information

Investors have every right to worry though, because the shift towards digital games has a huge impact on GameStop’s bottom-line. Without physical discs to trade, GameStop’s pre-owned game business would be negatively affected. This is the crown jewel of the business that has consistently been the highest gross profit contributor for years.

Source: GameStop 2018 annual report

And the tide doesn’t look to be turning as GameStop posted declines in quarterly growth in hardware, new game, and pre-owned game sales.

Source: GameStop Earnings Transcript

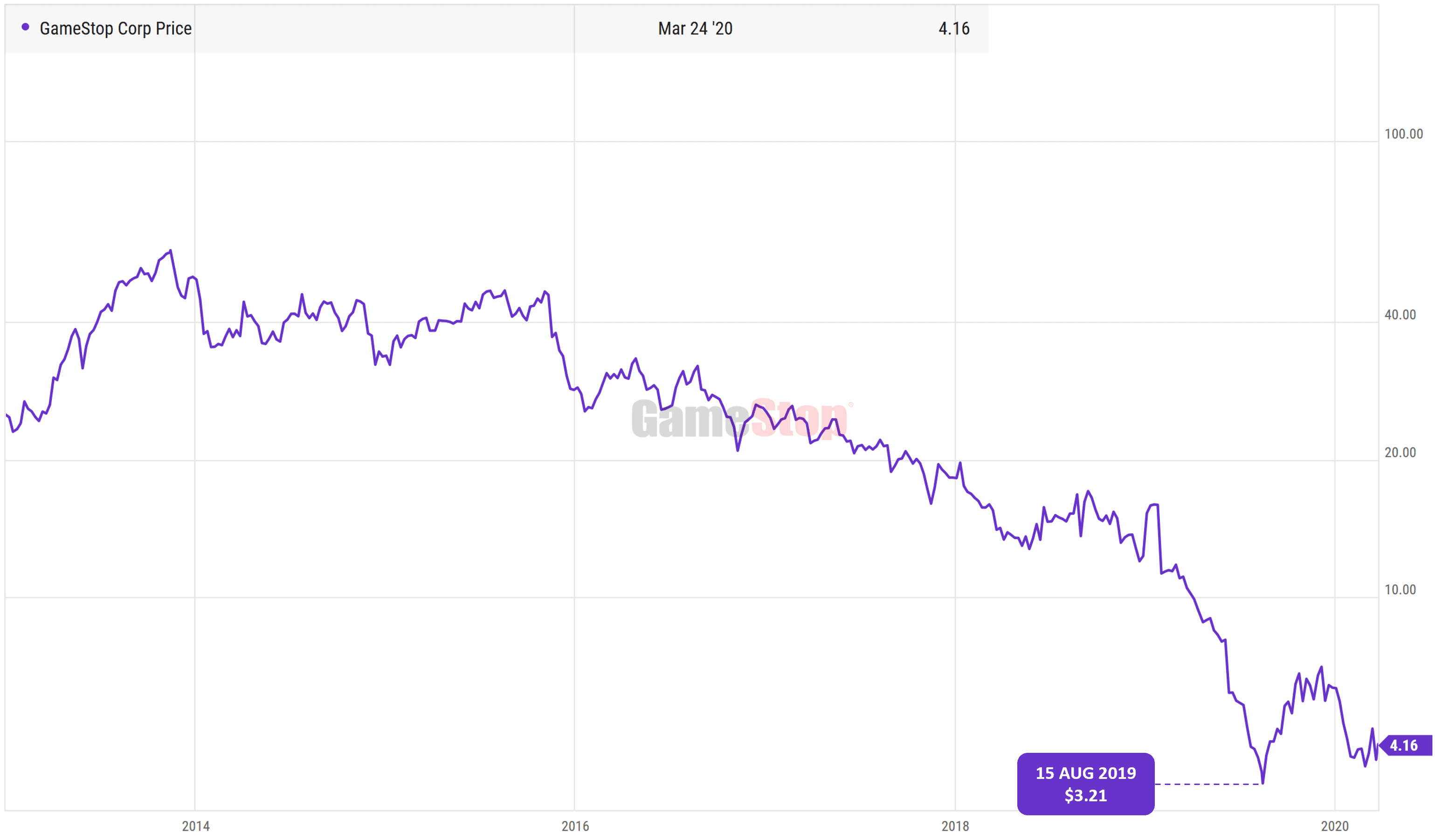

After reporting a 25.7% drop in revenue and an operating loss of $18.6 million after adjusting for restructuring, asset impairments and other one-off charges in Q3 2019, GameStop’s share price hit a low of $3.21 in August 2019.

Source: YCharts

But GameStop’s decline had already been set in place due to a series of poor capital allocation decisions made by the management over the past decade. In 2013, when GameStop entered the smartphone store business by acquiring Spring Mobile, it turned out to be a complete disaster.

As Wedbush analyst Michael Patcher said, ‘These stores were going to do a million apiece. So with 1,500 stores you’re looking for $1.5 billion in revenue and double-digit margins. So $150, $200 million profit, and I think they got to $80 [million]. They were just never even close.’

The company went from no debt and generating about $400 million in cash before the acquisition to $800 million in debt and generating $300 million in cash.

The opportunity

What caught my attention is the 117.46% short interest on GameStop. As of 25 March 2020, GameStop has a public float of 58 million shares and a short interest of 68.1 million shares.

This means that Wall Street has totally written off GameStop, thinking that it’s just a matter of time before it goes bust like RadioShack and all other physical retailers before them. However, any inkling of good news will trigger a short squeeze in the stock, which represents a good risk-reward ratio for investors who long the stock.

Thankfully for GameStop, the new generation of PlayStation and Xbox will come with disc drives. Physical games are gradually fading, but not dead yet.

As Phil Spencer, the head of Xbox put it in an interview: ‘I want to give people choice, and right now physical is a choice that millions of people love.’

Millions of gamers out there love collecting physical games, especially blockbuster games like Grand Theft Auto or Call of Duty. They like having the option of loaning the game to a friend after they are done with it or trade it in at GameStop. They can use the credits they obtained from the sale of their games to buy a new one, paying on average $17 for a pre-owned game compared to a new one for $48. A great way to play more for less.

Another positive trait of having a physical game is portability and convenience. They can bring it to any of their friends’ house instead of having to log onto their account on their friends’ consoles to download the game. Digital games also require more hard disk space which is a hassle for many people because a 500GB PS4 can only house between 10 to 12 games. For places with poor internet connection, it will take a long time to download a game.

What’s more, the new GameStop management is focused on engagement. To give their customers reasons to step into their stores, George Sherman, who became the CEO of GameStop in early 2019, wants to focus on turning the store into a ‘cultural gaming centre’.

Right now, they are testing different concepts at their stores in Tulsa, Oklahoma, which you can find out more about here. This is where gamers come together to try out new games before they buy, learn new skills, and gain excess to exclusive digital content.

GameStop can also leverage on its 60 million active members on their PowerUp Rewards Loyalty Program. Recently, they introduced the PowerUp Rewards Pro membership with benefits like monthly coupons and exclusive offers to encourage their members to spend more at their store.

According to GlobeNewswire, ‘During the test, GameStop noticed a double-digit lift in Pro membership sign-ups and an overall positive sentiment across its customer base. The research also reinforced that customers are looking for more value and benefits while making their shopping experience easier and more personal.’

GameStop has also delved into esports, establishing partnerships with some of the biggest esports teams in North America. They have built an 11,000-square-foot GameStop Performance Center in Frisco, Texas, to serve as the headquarters to Complexity Gaming – a professional esports organisation.

Watching other people play games is a big maket that’s projected to hit $1.8 billion by 2022. Although the details weren’t included, GameStop could potentially profit by taking a cut of live event ticket sales, merchandise sales, and sponsorships from game companies like Activision Blizzard and Electronic Arts. This ties in well with their new concept stores where they can bring in professional gamers to connect with their customers and teach them new skills on how to defeat that level 80 monster!

The numbers

Operationally, the management is working to streamline operations and diversify non-core businesses. At the Q3 2019 earnings call, George Sherman announced a $200 million profit improvement goal, half of which will be delivered in the form of expense reductions and the other half from product margins enhancements. They have achieved 50% of the target so far, mostly from the closing down of stores and cutting headcount. GameStop also divested Simply Mac, an authorized reseller of Apple products for an undisclosed price; and Spring Mobile’s AT&T wireless stores to Prime Communications for $700 million to focus on their core business. This frees up capital for the GameStop to pay down their debt and repurchase shares.

Fundamentally, GameStop has adequate financial capital and stamina to reposition the company to benefit from the new console cycle at the end of 2020. It has a cash balance of $290.3 million and inventory worth $1.3 billion, which is more than enough to paydown their debt of $419.4 million today. If they need, GameStop can also tap on their $900 million in credit facility to revamp their stores.

During Q3 2019, the company spent $175 million to retire 34% of its outstanding shares. With $121 million worth of remaining authorised share repurchases at a share price of $3.63, GameStop could reduce their share count by 50% to 33.33 million shares.

For the short squeeze to occur like it did before in 2013 at the beginning of the PS3 and Xbox 360 console cycle — which caused the share price to more than triple from $16.02 to $55.38 — GameStop does not have to be wildly successful in reinvigorating growth in the company.

Source: YCharts

All GameStop has got to do is to generate an operating cash flow of around $300-400 million like they did back in 2018-19 and reinstate the $150 million in dividends that they’d been distributing over the past five years.

With a smaller share count of 33.33 million shares, the dividends per share will amount to $4.50. That’s a 108% dividend yield based on today’s price of $4.16. That’s a good enough reason for investors to swoop in and buy up the stock.

At a market capitalization of $274.2 million, we are basically betting on whether the company will generate that level of cash flow we are looking for. Whether it represents a good value or not is up to your judgement.

The fifth perspective

Deep value stocks are fraught with risks. GameStop’s investment thesis could be derailed when management makes foolish acquisitions, refuses to buy back shares, or console manufacturers decide not to release their consoles by the end of 2020. You’re either right or wrong, nothing in between. Therefore, it’s essential for investors to manage their risk and not make a concentrated bet on such plays.

Note: This is neither a recommendation to purchase or sell shares of GameStop, and the information here is for educational purposes and/or for study or research only.