Kuala Lumpur Kepong Berhad (KL Kepong) (Bursa: 2445) is the third largest plantation company listed on Bursa Malaysia. It has an integrated business model and the company derives income mainly from both upstream palm oil plantation activities and downstream oleochemicals manufacturing activities. As I write, KL Kepong is worth RM26.3 billion in market capitalization.

In this article, I’ll bring a detailed account of KL Kepong’s tremendous success and achievements thus far and its outlook fir the future. Here are the 10 things you need to know about KL Kepong before you invest.

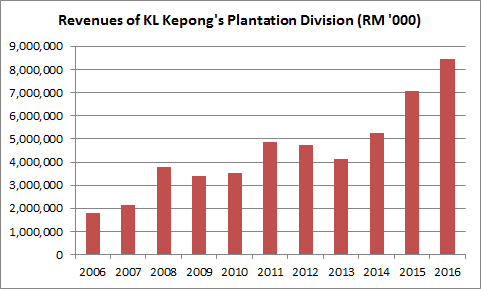

1. KL Kepong’s Plantation division achieved a CAGR of 16.70% in revenues over the last 10 years from RM1.80 billion in 2006 to RM8.46 billion in 2016. This is directly contributed by KL Kepong’s continuous efforts in enlarging its portfolio of plantation estates which resulted in steady increases in production of fresh fruit bunches (FFB), crude palm oil (CPO) and palm kernel (PK) during the 10-year period.

Source: KL Kepong annual reports

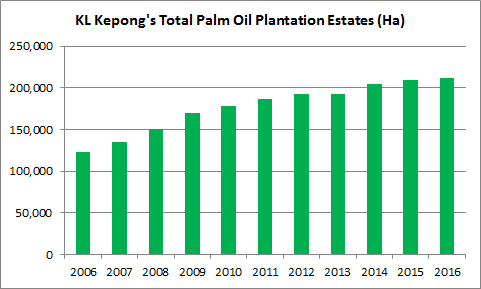

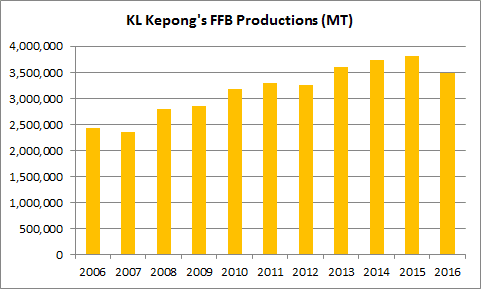

2. As of 30 September 2016, KL Kepong has 211,574 hectares of palm oil plantation estates. Out of which 44% are located in Malaysia, 52% in Indonesia, and the rest in Liberia. It is a substantial increase from the 123,462 hectares the company owned in 2006. Accordingly, KL Kepong has achieved a CAGR of 3.74% in FFB production over the last 10 years. It has grown from 2.42 billion metric tonnes (MT) in 2006 to 3.50 billion MT in 2016.

Source: KL Kepong annual reports

Source: KL Kepong annual reports

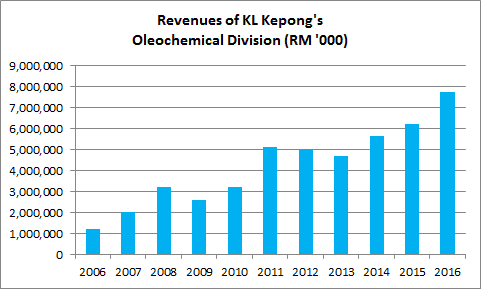

3. KL Kepong’s Oleochemicals Manufacturing division achieved a CAGR of 20.67% in revenues over the last 10 years from RM1.23 billion in 2006 to RM7.74 billion in 2016. Sales growth was attributable to multiple expansion projects, acquisitions, and joint ventures which has enabled KL Kepong to produce a wider range of oleochemical products such as fatty acids, glycerine, fatty alcohols, esters, amines, biodiesel and fine chemicals in plants located in Malaysia, China, and Europe.

Source: KL Kepong annual reports

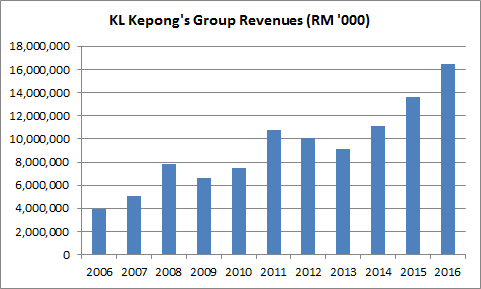

4. KL Kepong achieved a CAGR of 15.47% in group revenues over the last 10 years from RM3.92 billion in 2006 to RM16.51 billion in 2016. This is contributed by sales growth achieved by both plantation and oleochemicals manufacturing divisions during the period.

Source: KL Kepong’s annual reports

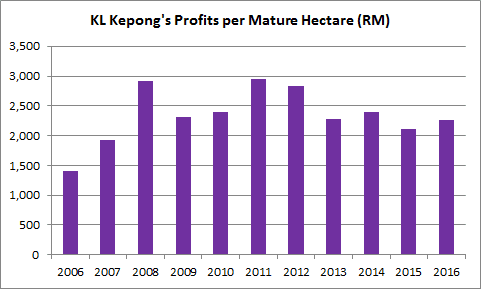

5. KL Kepong’s earnings are dependent on prices of palm oil products and costs of labour and fertilisers. For instance,

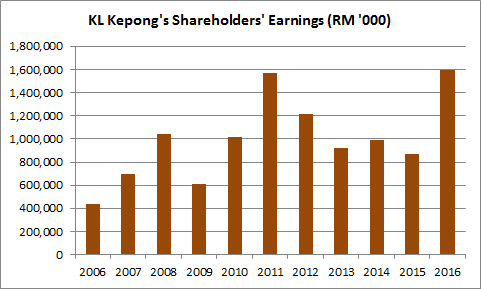

- 2006 – 2011: KL Kepong recorded higher profits per mature hectare from RM3,599 in 2006 to RM9,783 in 2011. This is because prices of palm oil products rose substantially during the period. The average selling price of CPO jumped from RM1,401 per MT in 2006 to RM2,958 per MT in 2011. As a result, KL Kepong reported a substantial increase in shareholders’ earnings from RM436.2 million in 2006 to RM1.57 billion in 2011.

- 2012 – 2015: KL Kepong’s margins were compressed as it reported declining profits per mature hectare from RM9,873 in 2011 to RM4,668 in 2015. This is due to lower prices of palm oil products and hikes in costs of labour and fertilisers. The average selling price of CPO declined from RM2,958 per MT in 2011 to RM2,106 per MT in 2015. Thus, KL Kepong reported a decline in shareholders’ earnings from RM1.57 billion in 2011 to RM869.9 million in 2015.

- 2016: KL Kepong recorded RM4,327 in profits per mature hectare in 2017, the lowest reported since 2007. However, KL Kepong was able to record RM1.59 billion in shareholders’ earnings, 83% higher than RM869.9 million in 2015. But this increase was largely due to RM496.5 million in gains on disposal of land and RM268.0 million in net deferred tax credits from the revaluation of its assets in Indonesia. According to the Chairman’s Statement, if these one-off gains are excluded, the underlying profits would be RM892.6 million which is comparable with the earnings reported in 2015.

Source: KL Kepong annual reports

Source: KL Kepong’s annual reports

6. Overall, KL Kepong has a 10-year return on equity average of 14.90%. This means it has made, on average, RM14.90 in annual earnings from every RM100 in shareholders’ equity over the last 10 years. Here’s why we like companies with consistently high ROE.

7. KL Kepong generated RM9.31 billion in cash flows from operations over the last 10 years. It has also raised another RM3.11 billion in net long-term debt. Out of which KL Kepong has allocated RM5.26 billion to capital expenditures, RM1.39 billion to plantation development expenditures, and RM5.60 billion in dividend payments to shareholders.

This means that KL Kepong is itself a cash-producing business and doesn’t need to continually raise equity or debt to expand its business or reward its shareholders with dividends.

8. Overall, KL Kepong has a 10-year dividend payout ratio average of 56.55%. Over the last five years, KL Kepong has paid out the following amount in dividend per share:

| 2012 | 2013 | 2014 | 2015 | 2016 | |

|---|---|---|---|---|---|

| Dividend per Share (in Malaysian sen) | 65 | 50 | 55 | 45 | 50 |

As at 16 October 2017, KL Kepong is trading at RM24.74 a share. If KL Kepong is able to maintain its dividend per share at RM0.50, its expected dividend yield is 2.04%.

9. At present, KL Kepong has several potential risks involved and discussed initiatives to mitigate the impact on its business performance. They are:

- Firstly, KL Kepong faces the risk of fluctuation in palm oil prices. It is largely influenced by crude oil prices. For instance, low crude oil prices would negatively impact the economic feasibility of producing biodiesel. As such, it will affect the demand and prices of palm oil. Thus, containing production costs through enhancing productivity is important to boost profits in times of low palm oil prices.

- Secondly, the growth in Indonesia’s refining capacity is outpacing production growth of CPO. In 2016, Indonesia had a total refining capacity of 47 million tonnes which is substantially more than its CPO available output of 31 million tonnes. KL Kepong is at risk of receiving lower refining margins as refiners are competing to secure feedstock and is at risk of not being run at full capacity due to insufficient feedstock. In response, KL Kepong has set up an aggressive procurement team and forged partnerships with key upstream players to ensure feedstock supply continuity to its refineries in Indonesia.

- Thirdly, palm oil plantations are labour intensive. KL Kepong faces several risks such as labour shortages, heavy reliance on foreign workers, and rising wages. As such, KL Kepong continues to reduce its ‘workers to hectare ratio’, introduce new planting materials, and execute replanting programmes to enhance production yields from its plantation estates.

10. Looking ahead, KL Kepong is embarking on several plans to sustain future growth. They include:

- As of 30 September 2016, KL Kepong has 176,391 hectares and 35,183 hectares of mature and immature plantation estates respectively. The estates in Indonesia are younger with 40,908 hectares (37.9%) of trees in these estates between four to nine years old and have yet to reach prime harvesting age. As such, FFB production is expected to rise in 2017 and 2018 from 3.50 billion MT reported in 2016.

- In 2017, KL Kepong is projected to spend RM88 million on new planting and replanting activities in Malaysia, Indonesia, and Liberia. It plans for new planting activities across 2,000 hectares and replanting activities across 5,000 hectares for the year.

- In 2016, KL Kepong started the development of a 30 MT per hour mill in Liberia and 60 MT per hour mill in Medan, Indonesia. It is also expanding its Indonesian palm oil mills from 60 MT to 90 MT per hour in Belitung Island and from 60 MT to 80 MT per hour in Riau. These projects were initiated as KL Kepong expects higher FFB production in Indonesia and Liberia in the immediate future.

The fifth perspective

In summary, KL Kepong has built a track record of expanding its plantation assets, rising production and sales, high profitability, and consistent dividend payouts to shareholders. As at 30 June 2017, KL Kepong has RM1.33 billion in cash reserves, a current ratio of 1.93, and a debt-to-equity ratio of 0.35. Maintaining a healthy balance sheet remains important as KL Kepong intends to strike a balance between dividend payments and investing for growth in the future. This enables KL Kepong to maintain its position as one of the leading conglomerates in the plantation sector.

if you like KLK, do take a look into Batu Kawan, who is the major shareholder of KLK.