Mapletree Logistics Trust (MLT) was listed on 28 July 2005 as the first Asia-focused logistics REIT in Singapore. The REIT owns logistics real estate located in Singapore, Hong Kong, Australia, China, Japan, Korea, Malaysia, and Vietnam. As at 31 March 2018, MLT was valued at S$3.76 billion in market capitalization.

In this article, I’ll give you an overview of MLT’s performance over the last 10 years and an update on its growth plans for the near future. Here are 13 things you need to know about Mapletree Logistics Trust before you invest.

Track record

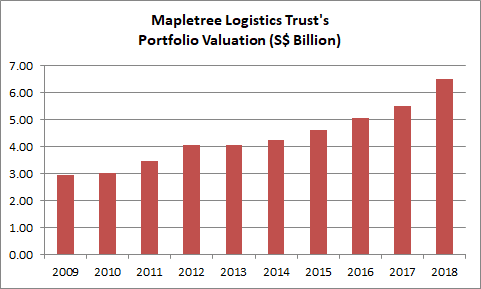

1. MLT has achieved a CAGR of 9.1% in valuation of its properties over the last 10 years. Its portfolio value has grown from S$2.97 billion in 2008 to S$6.52 billion in 2018 — an indication that the management has been proactively expanding its portfolio over the last 10 years.

Source: Annual/quarterly reports of Mapletree Logistics Trust

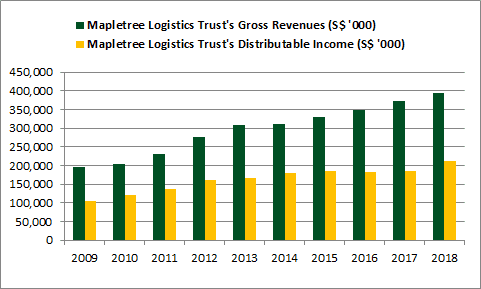

2. Gross revenues have grown from S$195.6 million in 2009 to S$395.2 million in 2018. This, in turn, has contributed to rising distributable income from S$105.0 million in 2009 to S$212.9 million in 2018. Its distribution per unit (DPU) increased from 5.11 cents in 2009 to 7.62 cents in 2018. This growth is in line with the management’s efforts to invest and expand its portfolio over the last 10 years. (Note: Financial data from 2009-2012 have been adjusted to reflect MLT’s results over 12-month period ending on 31 March for each financial year).

Source: Annual/quarterly reports of Mapletree Logistics Trust

3. As at 31 March 2018, MLT has reported a total debt of S$2.51 billion and its gearing ratio is at 37.7%. Its weighted average cost of debt is 2.3% and 78% of its total debt is hedged at fixed interest rates. Its average debt duration is 4.5 years and MLT was a ‘Baa1 with stable outlook’ credit rating from Moody’s.

Income visibility

4. As at 31 March 2018, MLT has a stable 96.6% occupancy rate for its portfolio. It derives rental income from a diversified pool of 556 tenants and its top 10 tenants account for 23% of MLT’s gross revenues. Its largest tenant, Wesfarmers Group (that own Coles Supermarkets) accounts only for 3.7% of gross revenue. This means MLT does not rely on a single large tenant for a substantial portion of its income.

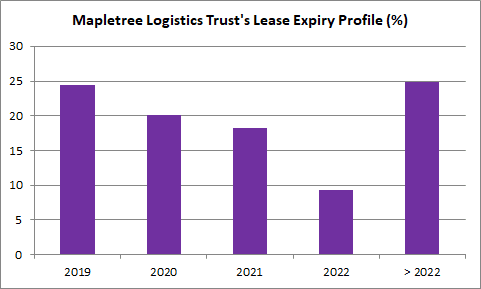

5. As at 31 March 2018, MLT’s weighted average lease expiry (WALE) is 3.5 years. 37.2% of leases are not due for renewal until FY 2022 and beyond. In the short term, 24.4% of its leases are due in FY 2019. The management intends to remain proactive in keeping and securing tenants to maintain MLT’s high occupancy rate and WALE. In 2018, MLT has a healthy tenant retention rate of 70%.

Source: Mapletree Logistics Trust 2018 annual report

Growth drivers

6. In January 2018, MLT completed the redevelopment of Mapletree Pioneer Logistics Hub. At a cost of S$90 million, the property is now a five-storey ramp-up logistics facility with a gross floor area (GFA) of 72,000 square metres — 1.8 times larger than before its redevelopment. The facility is situated at the heart of a mature industrial area and enjoys good connectivity to both Iskandar in Johor, Malaysia as well as the upcoming Tuas mega port.

7. In May 2017, MLT embarked on the redevelopment of Ouluo Logistics Centre which is situated close to Pudong International Airport, Shanghai. The centre will be transformed into a two-storey ramp-up logistics facility with a GFA of 80,700 square metres — 2.4 times larger than before its redevelopment. The redevelopment will be carried out in two phases with Phase 1 completing in Q2 2019 and Phase 2 in Q4 2020.

8. On 12 October 2017, MLT completed the acquisition of Mapletree Logistics Hub Tsing Yi for S$832 million. This property is a 11-storey modern ramp-up warehouse that has a GFA of 84,951 square metres located in Hong Kong. Tsing Yi is fully-occupied with 12 tenants which include Ever Gain, adidas, Angliss, HKTV, and Aramex. Based on its investor presentation, MLT will generate an additional S$43 million in annual net property income.

9. On 29 January 2018, MLT completed the acquisition of the remaining 38% stake in Shatin No. 3 for a sum of S$103.7 million. Shatin No. 3 is an 18-storey warehouse with cargo lift access in Shatin, the second largest warehouse market in Hong Kong. After the acquisition, MLT now has full ownership of Shatin No. 3 and has full control to increase the value of the property through refurbishment, asset repositioning, etc.

10. On 6 June 2018, MLT completed the acquisition of a 50% stake in a group of 11 logistics properties in China for S$212.8 million. Combined, the 11 properties have a committed occupancy rate of 97.7% and has 58 tenants that include JD.com Inc., Cainiao, Sinotrans Limited, Best Logistics Technology (China) Co. Limited and China Post Group Corporation. Based on its investor presentation, MLT will generate an additional S$19 million in annual net property income.

11. Mapletree Investments is the sponsor and the largest unitholder of MLT with a 35.72% shareholding. Mapletree is a leading integrated real estate development, investment, and capital management company that owns and manages S$39.5 billion worth of properties worldwide. Mapletree has a pipeline of 51 logistics properties that MLT can potentially acquire in the future. 45 of these properties are located in China (which include the 11 Chinese properties that were recently acquired). This acquisition pipeline from its sponsor will provide MLT with a stream of potential acquisitions over the long term.

Valuation

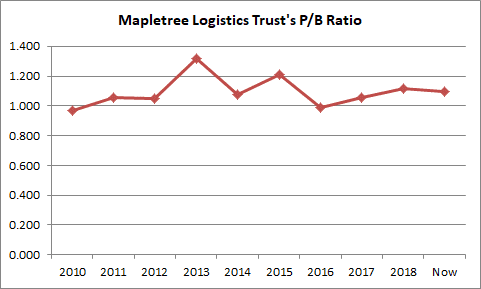

12. P/B ratio – MLT’s share price (as of 29 July 2018) is S$1.27 and its net asset value per unit (as at 30 June 2018) is S$1.12. Thus, its current price-to-book ratio is 1.10, which is close to its average of 1.09 since 2010. (Note: I excluded data from 2009 as MLT’s stock price was skewed downward by the Global Financial Crisis. In fact, it was an ideal time to invest in MLT as its stock price was extremely cheap in 2009.)

Source: Calculated from data from annual/quarterly reports of Mapletree Logistics Trust

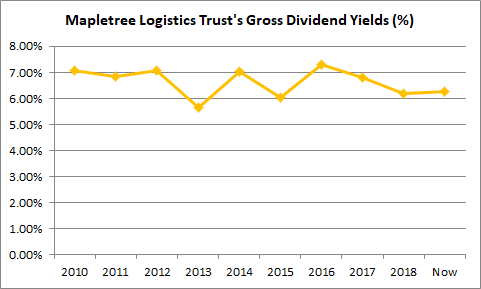

13. Dividend yield – Inclusive of its 50% stake in the new 11 logistics properties in China, MLT’s pro-forma DPU for financial year 2018 is 7.65 cents. Thus, its expected gross dividend yield is 6.0%, which is below its nine-year average of 6.66%. (Note: Data from 2009 was excluded for the same reason above.)

Source: Calculated from data from annual/quarterly reports of Mapletree Logistics Trust

The fifth perspective

Mapletree Logistics Trust is a REIT that has delivered consistent growth in revenues, distributable income, and DPU to its unitholders for the past 10 years. Evidently, MLT has placed its emphasis of growth in China as it intends to capitalize on key market trends such as rising affluence levels, growth in e-commerce sales across Asia-Pacific, and China’s implementation of the One Belt, One Road initiative.

At the moment, MLT is slightly overvalued when you compare it to the 10-year average P/B ratio and dividend yield. At the right price though, MLT is a good potential pick for an industrial REIT as it has proven to be a well-managed REIT with solid track record over the last 10 years.