Contrary to popular belief, Mastercard is not in the ‘credit card’ business. Rather, Mastercard is a vital network that connects customers and merchants around the world. They provide financial telecom infrastructure that allows financial institutions to communicate and transact with one another.

As the second largest financial telecom network in the world behind Visa, Mastercard has a wide geographical reach. Mastercard allows us to use our credit, debit, and prepaid cards to make payments in more than 150 currencies in over 210 countries and territories. In 2019, Mastercard processed a mind-boggling 87.3 billion transactions, a total of US$6.5 trillion in gross dollar volume.

So how does Mastercard make money? Let me take you through an example below to give you a better understanding of how Mastercard generates its revenues.

Business model

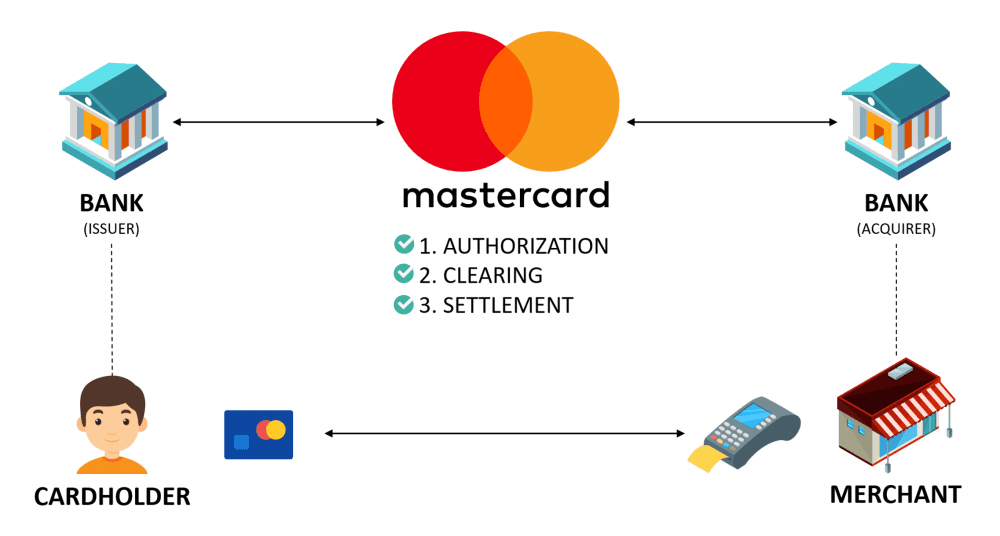

In any transaction, there are four participants – the cardholder, the issuer (the cardholder’s bank), the merchant, and the acquirer (the merchant’s bank). Mastercard is at the center of it all, acting as a toll operator responsible for the authorization, clearance, and settlement of payments.

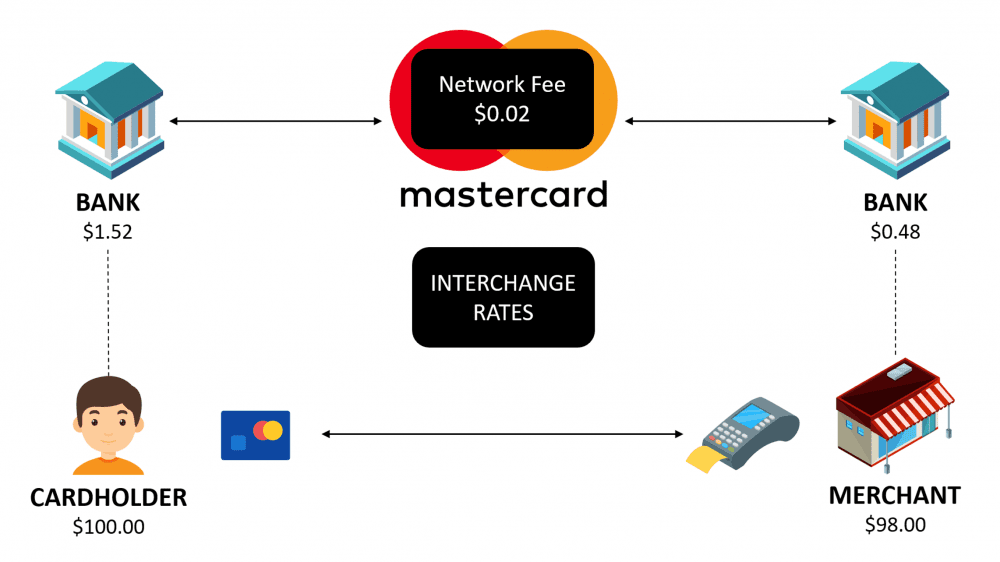

Whenever Mastercard processes a payment, the banks will pay 1) a fee per transaction (i.e. switch transaction fee) and 2) a percentage of the gross dollar volume (i.e. switch volume fee) to the network provider.

The transaction kicks off when you charge $100 to your credit card at say a clothing store. Once you have swiped your card, a signal will be routed from the merchant through the merchant’s bank and to your bank for authorisation. Your bank will check your credentials and whether you meet the financial requirements to make this purchase. Once approved, the merchant’s bank will give the merchant the greenlight to let the transaction go through. The point-of-sale system will spit out a receipt and you can be on your way home.

In the clearing phase of the transaction, which usually occurs within a day, the merchant’s bank will send the purchase details to your bank to update both the merchant’s and your account’s statements, determining how much is to be paid by your bank.

Finally, the settlement phase is where the acquiring bank and the merchant get paid by your bank. Notice from the chart above that the merchant received $98 instead of the $100 that you paid for the clothes.

The difference of $2 is known as the merchant discount rate that the acquirer collects from the merchant. Out of this, the acquirer then pays the issuer an interchange fee. Your bank gets a larger cut as they are taking on credit risk for loaning you the money when you use a credit card.

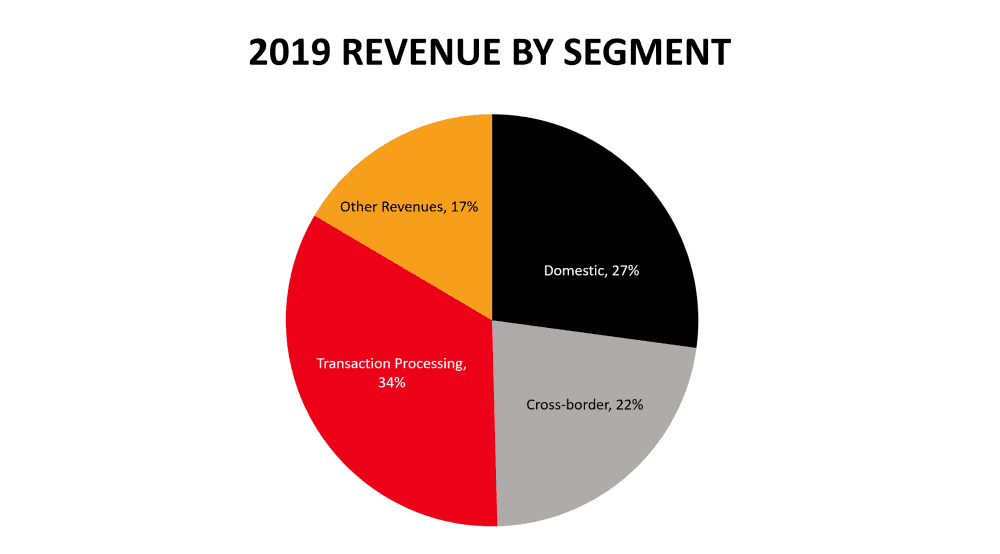

Mastercard classifies their revenue stream into four segments:

- Domestic assessment fees are generated based on switch volume fees.

- Cross-border assessment fees are collected similarly except that it includes currency conversion fees for international transactions

- Transaction processing fees are the switch transaction fees generated both domestically and internationally

- Other revenues are a mix of Mastercard’s consulting, data analytics and research; safety and security service; loyalty rewards; and program management services businesses all lumped into one

The first three segments comprise Mastercard’s core business representing 83% of the company’s revenue.

Economic moats

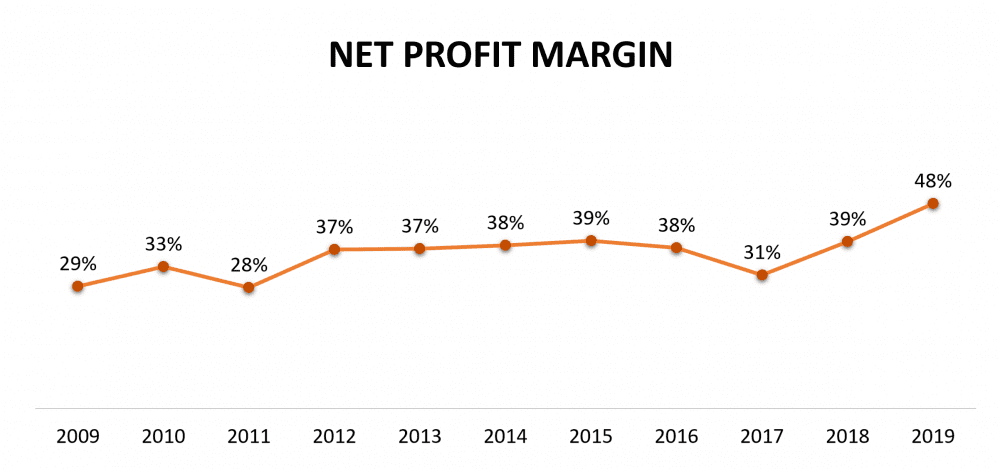

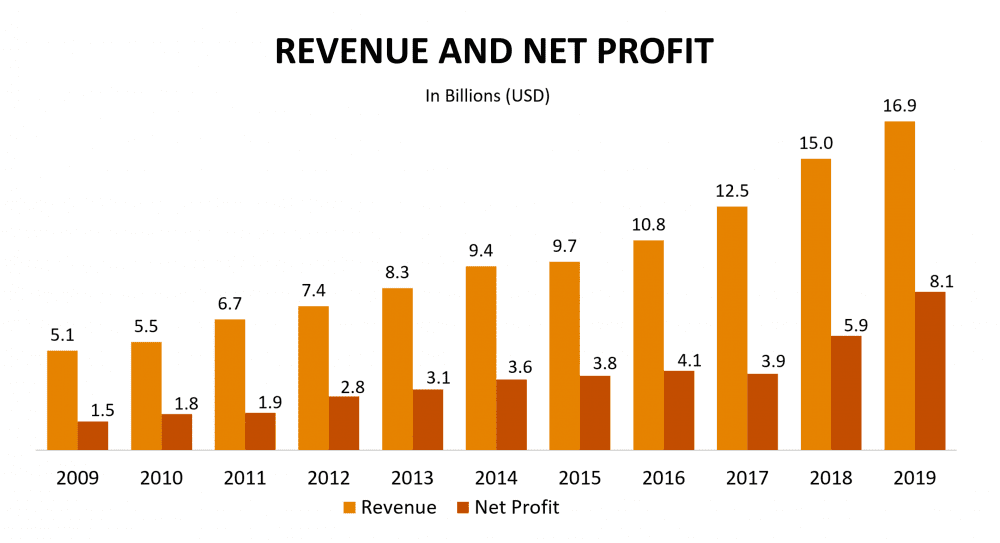

Outside China, this industry is dominated by three major players: Visa, MasterCard, and American Express. Over the years, Mastercard has amassed millions of merchants along with 2.2 billion Mastercard branded cardholders, giving the company economies of scale, driving its net profit margin from 29% in 2009 to 48% in 2019.

New entrants will have a hard time establishing a new network to compete head-on with incumbents as it requires a lot of capital and technological expertise to build data centers, and trust from financial institutions and cardholders to switch to a new provider.

Despite numerous competitors such as Google Pay, Apple Pay and PayPal, digital wallets and payment processers have not been successful in bypassing Mastercard’s network like what Alipay and WeChat Pay has done in China. Protected by a wide economic moat, Mastercard’s growth has been nothing short of spectacular – revenue grew at a CAGR of 12.73% for the past 10 years to US$16.9 billion in 2019.

Growth drivers

Mastercard will benefit greatly as we move towards a cashless society. The e-commerce industry is projected to grow from US$2.4 trillion in 2017 to US$6.5 trillion in 2023. This will drive the number of card transactions, which is expected to increase from 369 billion in 2018 to 854 billion in 2028.

The COVID-19 pandemic has only accelerated the change in consumer behavior as more and more of us shop for our essentials online. Even the older generation who are not as tech savvy are learning to navigate different e-commerce platforms during this period. Even in physical stores, we are turning to contactless payments as the fastest and safest way to transact as opposed to cash transactions.

Risks

In an oligopoly controlled by three companies, it common for Mastercard to get caught up in antitrust lawsuits from time to time. For example, in 2005, Mastercard, Visa, and a number of banks including JPMorgan Chase, Citigroup, and Bank of America were sued by 12 million merchants, alleging that they colluded to inflate interchange fees and prohibited them from directing consumers toward other methods of payment.

To settle, Mastercard, Visa, and the banks agreed to pay the merchants US$6.2 billion in 2018. Under the settlement agreement, merchants will be restricted from suing the card networks over the same card-swipe-fee claims for several years.

Thus, 8,000 retailers decided to opt out of the settlement, shrinking the settlement amount down to US$5.7 billion, as they chose to file their lawsuits separately.

Companies with dominant positions in the market get caught up with antitrust lawsuits repeatedly. It happens to Google, Facebook and Amazon all the time. It is a sign of Mastercard’s influence in the market that regulators must keep in check to protect the merchants.

The fifth perspective

Mastercard has been a stock market stalwart from its listing in May 2006. Besides the stock market crash in 2008, Mastercard has been on a steady upward trend ever since. If you invested $10,000 in Mastercard at its IPO, your stake would now be worth over $766K (as of October 2020).

In the near term, Mastercard looks like it will continue to ride on secular growth trends in the e-commerce and payments space. With its dominant position in an oligopolistic industry, Mastercard’s upward trend may well continue for many years to come.

Will player like Union Pay affect Mastercard market? Also new digital payment company like Square, will it affect the long term market share of Mastercard, Visa? What’s your thought on this. Thanks for your article.

Hi Dave,

No. Mastercard and Visa are the dominant networks outside of China. UnionPay is strong is China but it has been disrupted by Alipay and WeChat.

PayPal and Square are great platforms to make online transactions but they do not have the same influence as Alipay and WeChat. The networks were smart to partner with tech firms that wanted to offer digital payments before they could establish their own to bypass them. That’s why to this day, you can see Visa or Mastercard in digital wallets.

Does VISA operate the same as MasterCard? What is the comparison between them?

Hi Kin,

Both Visa and MasterCard are largely the same, except that Visa has a larger market share. Both are acquiring companies in the last couple of years to offer more features to their customers or serve their fintech partners better.

Hi Kenny,

Thanks for this piece. Just want to make a minor correction – the interchange fee is not the same as the merchant discount rate. The latter is what the acquirer charges the merchant (the $2 in the illustration). The former is what the acquirer pays the issuer.

Thanks, Lim! I’ve edited the sentence to illustrate the process better.

Very soon, new smart financial telecom companies will compete with the dominant ones

Hi Ziem,

It’s really hard to say if financial telecoms will beat Visa and MasterCard at their game. You really need to have a perfect mix of ingredients which TikTok has to light their platform on fire. Facebook though they can copy and succeed like they did with SnapChat but it didn’t work. It’ll also take time for financial telecoms to establish their network so you can dine anywhere in the world with the service that they are offering.

Hello – I noticed in the diagram that the merchant collects $98.00, while the banks take a total $2.00 and the network takes $0.02.

Which bank is paying the network that $0.02? Or is it passed to the merchant, in which case the merchant would only collect $97.98?

Thank you,

Ted

Hi Ted,

I see where you are coming from. Let me just lay everything out here to make it clearer.

1. The acquirer will collect a $2.00 merchant discount from the merchant

2. Then it will pay the interchange fee of $1.52 to the issuer

3. The issuer will pay the network $0.02

So technically, netting out the fee, the issuer receives $1.50 from this transaction.

I hope this helps! 🙂

I bought into Visa not long after it was floated on the stock exchange, and I remain a Visa shareholder (although I’ve now cashed out my original investment). I think MasterCard also looks great, and sometimes wonder I should hold both.

This SeekingAlpha posting is pretty interesting and is worth reading:

https://seekingalpha.com/article/4420318-visa-and-mastercard-showdown?mail_subject=v-visa-and-mastercard-a-showdown-between-two-of-the-largest-credit-card-companies&utm_campaign=rta-stock-article&utm_content=link-2&utm_medium=email&utm_source=seeking_alpha

My own reasons for buying V instead of MA were based on a very simplistic bit of research. I asked 20 friends to tell me how many credit or debit cards they had in their wallets that were either MasterCard or Visa. Visa won!

Hi Jonathan,

You can’t go wrong with either payment processing networks, but MasterCard is superior in terms of price performance due to a higher return on capital compared to Visa. In the past ten years, MA appreciated by 1,300% versus V of 1,070%.

I agree. I just wonder how long this outperformance can be sustained.

Hi Kenny,

Thank you for sharing this of Master/Visa’s Merchant model. Can tell that you are familiar with both companies businesses.

During recent period, we do see Master/Visa going into Cross-border Payments/Remittance, with acquisition of remittance companies such as Homesend, Earthport & few others. Just like to see your views on

a) how would Master/Visa transfer funds?

b) is their model likely sustainable or competitive? – when Banks or Western Union have been doing this for ages.

Look forward to your views/opinion.

Hi Kenny, very informative. I am looking at Supplemental Operational Performance Data at mastercard investor relations website and i cant understand what is the difference Purchase Transactions (Millions) (34,121 in 2q21) on page 3 and switched transactions (27,288 in 2q21) on page 8. I did try to look online for the answer but i am still not sure. I was wondering if you could help me with that. Cheers

Hi Jair,

According to the Supplemental Operational Performance Data (page 7):

‘The Mastercard payment product is comprised of credit, charge, debit and prepaid programs, and data relating to each type of program is included in the tables. The tables include information with respect to transactions involving Mastercard-branded cards that are not switched by Mastercard and transactions for which Mastercard does not earn significant revenues.’

This would explain the difference in the number of purchase and switched transactions.