It’s safe to say that you have heard of Microsoft and used many of its products. Indeed, Microsoft is one of the most successful technology companies worldwide since it was founded 45 years ago by the legendary Bill Gates. It is also the third largest company listed in the U.S. (as of 2 September 2020).

Microsoft’s success intrigues me, so I proceeded to dig up more about the company’s business performance from an investor’s perspective. In this article, I’ll also cover the company’s economic moats, growth drivers, and some of the business risks it faces. Through this, I hope to give you a good overview of Microsoft’s business model and how it generates its revenues.

Business model

Microsoft is a technology company that provides software products and services to its consumers. It reports three business segments:

1. Productivity and Business Processes

This segment comprised 33% of Microsoft’s revenue in 2019. It consists of products and services in Microsoft’s portfolio of productivity and information services which include:

- Office Commercial/Consumer — Revenue is derived from users subscribing to Microsoft’s Office software suite. Services in this segment are intended to enhance personal and organisational productivities. This segment is a key driver of revenue in this business segment of Microsoft.

- LinkedIn — The professional social network makes money by offering three categories of monetised solutions: Talent solutions, marketing solutions, and premium subscriptions.

- Dynamics — This business provides cloud-based and on-premises business solutions for business applications like enterprise resource planning (ERP) and customer relationship management (CRM). Dynamics revenue is driven by the number of users licensed, expansion of average revenue per user. and the shift to Dynamics 365 — the cloud component of Dynamics.

2. Intelligent Cloud

This segment comprised 31% of Microsoft’s revenue in 2019. It consists of Microsoft’s public, private, and hybrid server products and cloud services that power modern businesses:

- Server Products and Cloud Services — Microsoft’s server software provides integrated server infrastructure and middleware designed to support software apps built on Windows. Server products include Microsoft’s SQL Server and Windows Server. Server products revenue is driven through volume licensing programs, licenses sold to original equipment manufacturers, and retail packaged products. Microsoft also provides a comprehensive set of cloud services through Microsoft Azure. This is in line with the secular growth of cloud computing as opposed to managing on-premises hardware and software. Azure makes money through users subscribing to its service.

- Enterprise Services like Microsoft Consulting Services are project-based engagements to help customers plan and implement Microsoft products so they can reap as much value from Microsoft’s products as possible.

3. More Personal Computing

This segment comprised 36% of Microsoft’s revenue in 2019. It consists of products and services mainly catered to improving the user experience:

- Windows – the operating system is still the most used desktop operating system in the world. Windows original equipment manufacturers’ (OEMs) revenue is derived from the purchase of Windows licenses by OEMs, which they pre-install on the devices they sell.

- Devices — including Surface, PC, and other Microsoft intelligent devices. Revenue is derived from this segment from the sale of these devices.

- Gaming — Microsoft’s generates gaming revenue from the sale of Xbox consoles and games.

- Search – Microsoft’s search engine, Bing, generates advertising revenue.

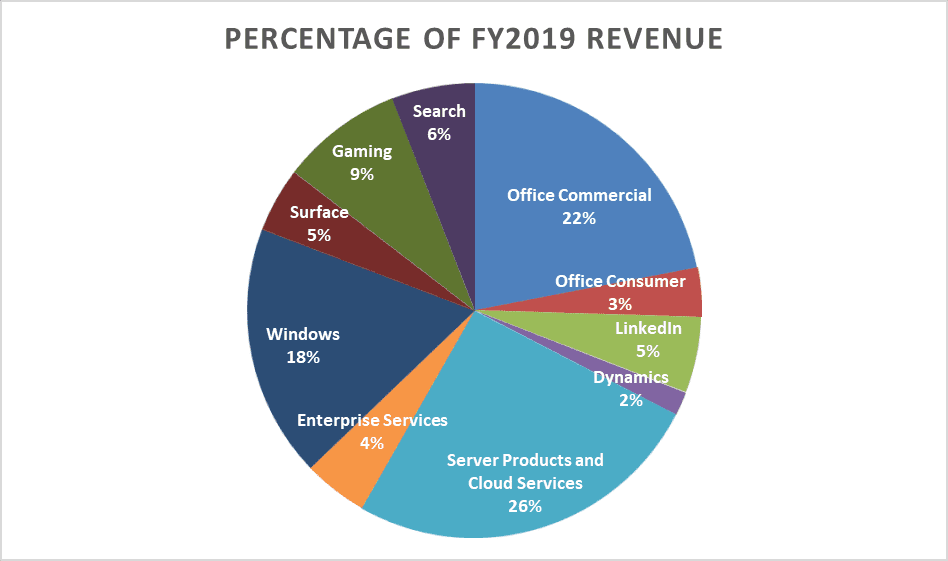

Here’s a breakdown of Microsoft’s segmental revenue for FY2019:

As you see from the chart above, Microsoft’s server products, Office, and Windows comprised more than 69% of Microsoft’s revenue in FY2019. Microsoft’s success lies in its ability to form economic moats around its key business segments/products.

Economic moats

Let’s examine some of the economic moats Microsoft has established.

High switching costs

This is due to the industry standard Microsoft has created with its Microsoft Office software. Business functions like accounting procedures are often centered around Microsoft Excel. Thus, it would take a lot of work for users to transfer their financial spreadsheets to another platform and get used to the unfamiliar tools on the new platform (even if there were a superior alternative to Excel in the first place). Thus, it makes economic and psychological sense for companies to continue using Microsoft Office.

Microsoft’s Windows Server also forms the IT backbone of many of the world’s largest companies today. Given that it would be extremely costly for any company to replace any part of an enterprise’s IT environment, we can expect many companies to continue using Windows Server. Microsoft’s high switching costs lock customers into its unique ecosystem of Microsoft software.

Network effect

For starters, Microsoft’s network effect is established with the increased number of participants of Microsoft products, which improves the value of Microsoft’s platforms for users.

For example, with an estimated 750 million people in the world using Excel, it gives software developers the financial incentives and economies of scale when they create a variety of add-ins for Excel – such as integrating popular finance platforms like Bloomberg and Capital IQ into Excel. When the financial community wants to analyse financial figures via Bloomberg or Capital IQ, they would have an easier time doing so with Excel.

Moreover, Microsoft’s ability to move clients from an on-premises Microsoft environment to a cloud Microsoft environment via Azure has led to a wide variety of developers joining the ecosystem with applications and development tools. This has led Microsoft Server to become very attractive for CIOs and IT managers with a large installed base of users, which attracts developers which in turn attracts more users.

Growth drivers

Cloud computing

The secular growth in cloud computing presents growth opportunities for Microsoft’s cloud business, Azure. With benefits like cost savings on hardware and automatic software integration, many companies are moving to the cloud. According to Gartner, the global cloud computing market size is expected to grow at a CAGR of 15.9% from 2018 to 2022, making it a US$354 billion industry by then. Gartner added that, by 2022, up to 60% of organizations will use an external service provider’s cloud-managed service, double that of 2018.

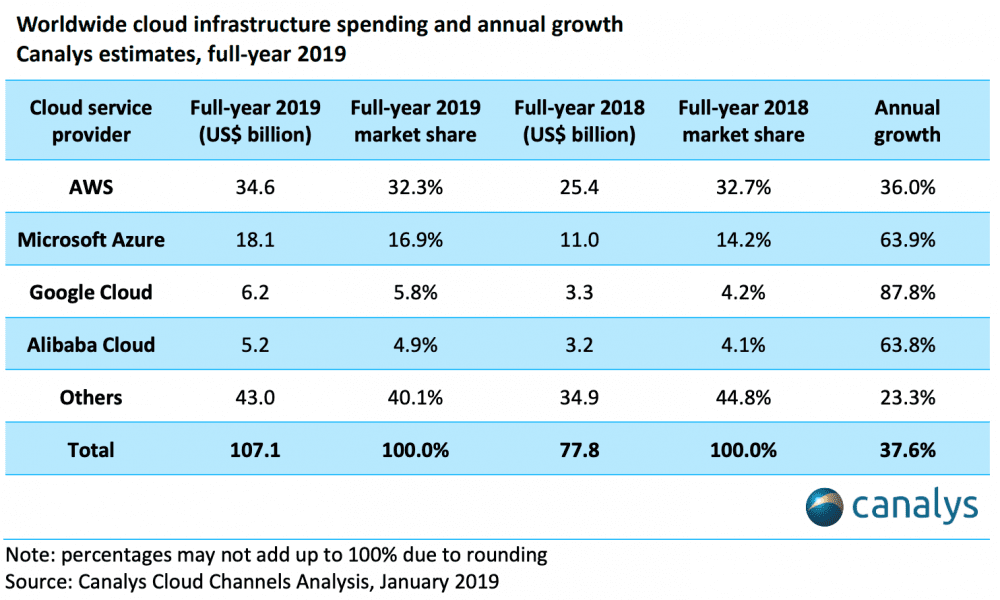

Seizing on the cloud computing trend, Azure’s revenue grew at an astounding year-on-year rate of 91% and 72% for FY2018 and FY2019 respectively. However, as Amazon entered the cloud computing space much earlier than Microsoft did, Amazon Web Services (AWS) still dominates the industry with 32.3% of market share in 2019. Azure is just behind AWS at second place with 16.9% of market share.

However, Microsoft is slowly closing on the gap. Just late last year, Azure pulled off a stunning upset to win a US$10 billion Pentagon technology contract, beating AWS. This underscores Azure’s growing reputation in the industry.

The top three cloud providers today — Google Cloud, Azure, and AWS — will be competing fiercely to capture market share in the cloud computing industry in the years to come. The cloud business is very technical, so here is an article to help you understand the competition in the cloud industry better.

Office 365

Microsoft is the pioneer in office-related products and Microsoft Office 365 is part of CEO Satya Nadella’s vision for remaking Microsoft into a company where customers rent rather than buy software. Customers benefit as they no longer have to manage software on their own computer or data centers. Rather, Office 365 ensures that users are always on the latest Microsoft versions without having to upgrade anything.

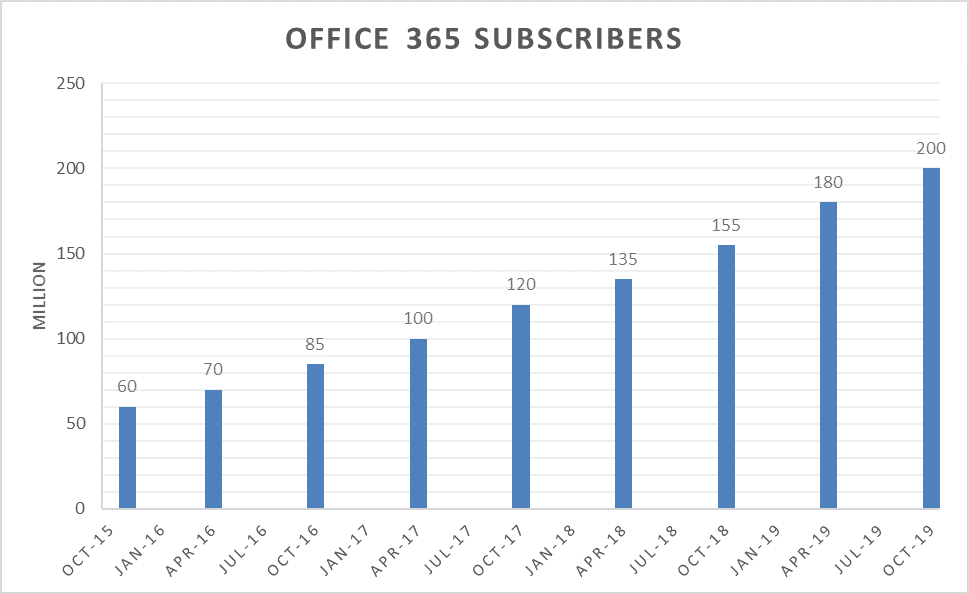

The steadily increasing number of monthly active users on Office 365 indicates that Microsoft have been successful in convincing enterprise customers to upgrade to the subscription-based Office 365 licenses.

Financial performance

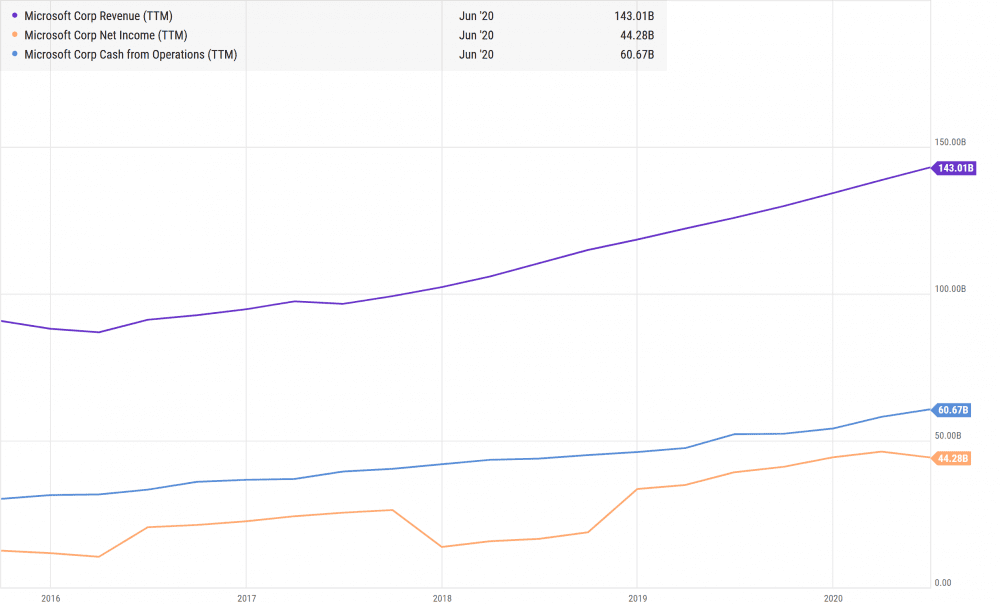

Microsoft is a very profitable company with steady revenue and net income growth over the past five financial years. This displays Microsoft’s ability to expand its user base and increase its average revenue per user.

Microsoft’s net income fell in FY2018 due to the Tax Cuts and Jobs Act which was enacted in December 2017. This required Microsoft to incur a one-time net charge of $13.7 billion on the repatriation of deferred foreign income not previously subject to U.S. income tax.

Microsoft also displays good earnings quality with its operating cash flow comfortable trending above its net income over the past five years. In FY2020, Microsoft generated $1.37 in cash for every dollar of profit.

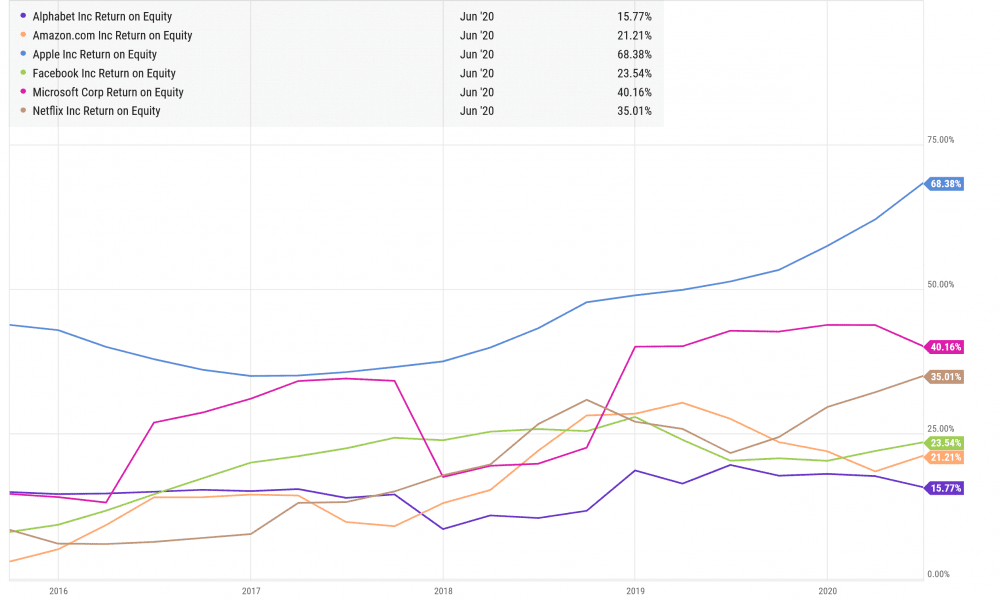

Microsoft has also generates a high return on equity (ROE) relative to its peers.

Microsoft’s ROE of 40.16% as of June 2020 is higher than the FAANG stocks bar Amazon. Microsoft is also able to achieve this with a reasonable amount of debt – its debt/equity ratio in FY2020 is just 0.54.

Risks

Business model competition

Microsoft competes with companies with a growing variety of business models. Some of Microsoft’s competitors offer free applications and content by making money from selling third-party advertising. Hence, the products of Microsoft’s competitors are provided to its users at no cost, competing directly with Microsoft’s revenue-generating products.

Competitors also compete by modifying and then distributing open source software at little cost to users without having to bear the full R&D costs for the open source software. These products are very similar to the functionality and features of Microsoft’s products.

Cloud computing risks

Microsoft’s increasing focus on cloud-based services also presents execution and competitive risks. Microsoft incurs costs in building and maintaining infrastructure to support its cloud computing services. It needs to establish sufficient market share to achieve scale necessary to reap profits from its cloud business. This depends on its execution in several areas.

For example, making its suite of cloud-based services platform-agnostic, available on a wide range of devices; and ensuring its cloud services are secure and reliable for its customers. Not to mention Microsoft’s ability to distinguish itself from the fiercely competitive cloud computing market, notably Amazon and Google.

The fifth perspective

Microsoft is clearly a high-quality company. It scores highly on profitability, has wide economic moats and is venturing into new growth areas. Yet, Microsoft is a company that is heavily involved in the software space with technical concepts that can be hard to understand for the layman.

The technology sector is also a hugely competitive one, so an investor needs to conduct deeper-than-usual analysis of Microsoft’s competition, and assess whether Microsoft can remain relevant and profitable in the many years to come.

May I know how do we evaluate intrinsic value of Microsoft? If one decide to enter a position in this counter, what should be the fair value price?

Thank You

Hi Elim,

One way is to compare Microsoft’s current P/E ratio against its long-term historical average. All things equal, a stock that’s trading below its historical valuation average can be consider undervalued.