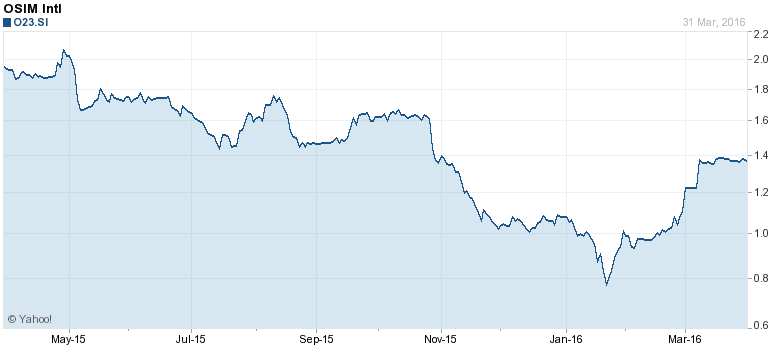

Chairman and CEO of OSIM International, Ron Sim, announced on 7 March 2016 that he plans to take the company private and offer to buy out remaining shareholders at $1.32 per share – a 7.8% premium to OSIM’s last traded price of $1.225 on 1 March. Shortly after the announcement, OSIM surged to $1.38 per share – six cents higher then Sim’s offer price. It seems investors are valuing the company higher than Sim’s $310 million cash offer.

OSIM traded as high as $2.90 per share in 2014 but fell to as low as 77 cents in the last twelve months. The main reason for the drop is the poor performance in OSIM’s key markets, especially their largest market China. The company’s net profit dropped nearly 50% to $51.5 million in 2015 from $102.2 million the year before. This has pulled OSIM’s valuation downward and, in turn, Ron Sim’s privatization offer. But to price OSIM based on its short-term performance and does not, in my opinion, do justice to its valuation.

So in order for us to get a more reliable valuation of OSIM, we need to determine the normalized earnings of the company over the last ten years.

1. Calculate OSIM’s 10-year average return on equity

Please note that the earnings I used here to calculate the return on equity (ROE) is from OSIM’s core business operations only; I excluded any exceptional gains, impairment losses, etc. To be even more conservative, I also used after-tax figures.

With that, I computed OSIM’s ROE from 2006 to 2015 and its 10-year average is 19.3%. In other words, in a “normal” year, OSIM should generate more or less this amount of ROE.

2. Calculate OSIM’s normalized earnings per share

We already know OSIM’s 10-year average ROE. The next step is to calculate OSIM’s normalized earnings per share (EPS). To do that, I use the ROE formula:

Average ROE = Normalized EPS / Shareholder Equity per Share

Plugging in OSIM’s average ROE (19.3%) and equity per share ($0.54) into the formula, I can derive that OSIM’s normalized EPS is $0.10.

Normalized EPS = 0.193 x 0.54 = 0.10

3. Calculate OSIM’s intrinsic value

With a normalized EPS of $0.10 and assuming OSIM trades at a fair value of 12 times earnings, OSIM’s intrinsic value is $1.20 per share.

EPS x P/E = 0.10 x 12 = 1.20

Now it looks like Ron Sim’s $1.32 per share offer looks like a good deal for shareholders, but OSIM actually has a net cash position of $0.27 per share. So if you add OSIM’s net cash, it’s intrinsic value is actually $1.47 per share — which means Ron Sim’s offer is actually a 10% discount to OSIM’s intrinsic value.

Moreover, I used a rather conservative P/E to value OSIM; I believe a company with a strong consumer brand like OSIM can be valued higher at 15 times earnings. So in short, I personally think OSIM is worth at least $1.47 per share or higher.

The fifth perspective

OSIM’s financial performance may be suffering right now mainly due to China’s economy but it’s important to ask the question: Will the company’s profits remain permanently depressed or is this just a temporary dip?

In the long term, I think it’s safe to say that China’s economy will continue to grow – maybe no longer at a neck-breaking pace of 8% per annum — but China will continue to grow nonetheless in the years to come and OSIM will logically ride on China’s growth.

Another growth driver I see in OSIM is its TWG Tea brand. OSIM doesn’t reveal how much TWG Tea contributes to its total revenue (it’s all lumped together) but what I do know is that TWG Tea is a very successful and fast-growing consumer brand. TWG Tea has grown from ten outlets in 2011 to 52 outlets in 2015, operating in 14 markets internationally. I was in Hong Kong recently and the queue to enter the TWG tea salon was very long! Besides its own stores, TWG Tea also supplies hotels, restaurants, and airlines.

The long-term prospects in China and TWG Tea means that the company has a lot more potential growth ahead of it. And with Ron Sim’s offer price markedly below OSIM’s intrinsic value, I believe Mr Sim is, in my opinion, getting a good deal out of privatizing OSIM right now.

Update: Ron Sim raises offer to take Osim private to S$1.39 a share

Second update: OSIM clarifies final offer price of S$1.41

Read more: 6 Things I Learned from OSIM International’s FY2015 AGM

Ron sim is not really looking to buy. 😉

ron sim succeeded!

Hi.

Normalized EPS should be multiply, EPS = 0.193 x 0.54 = 0.10. result is correct, so I believe it’s just a typo .

Hey Jeff,

Thanks for pointing that out. =)

I didn’t look at OSIM’s nos. but if it is highly leveraged, the ROE would be inflated.

Using ROE to normalize EPS tends to inflate EPS, as ROE doesn’t just consist of EPS but also includes a Financial Leverage (ie debt) component. Your EPS of $0.10 (derived from average ROE) may be overstated, and hence your IV.

Just wondering, why use ROE when one could use average EPS (derived from actual diluted EPS nos) to compute IV?

Hi Anon,

OSIM is highly leveraged but they have reduced their leverage in recent years. Yes, average EPS can be use to calculate intrinsic value too.

Please note that financials is just one factor when it comes to valuation and that can be affected by short-term performance. OSIM’s results have been poor recently due these factors I covered here: https://fifthperson.com/osim-international-6-things-learned-fy2015-agm/

We also need to consider the qualitative aspects of the company. For example, the OSIM and TWG Tea brands are definitely worth something and the latter has plenty of potential growth in years to come. This factor is not included in the IV calculation.