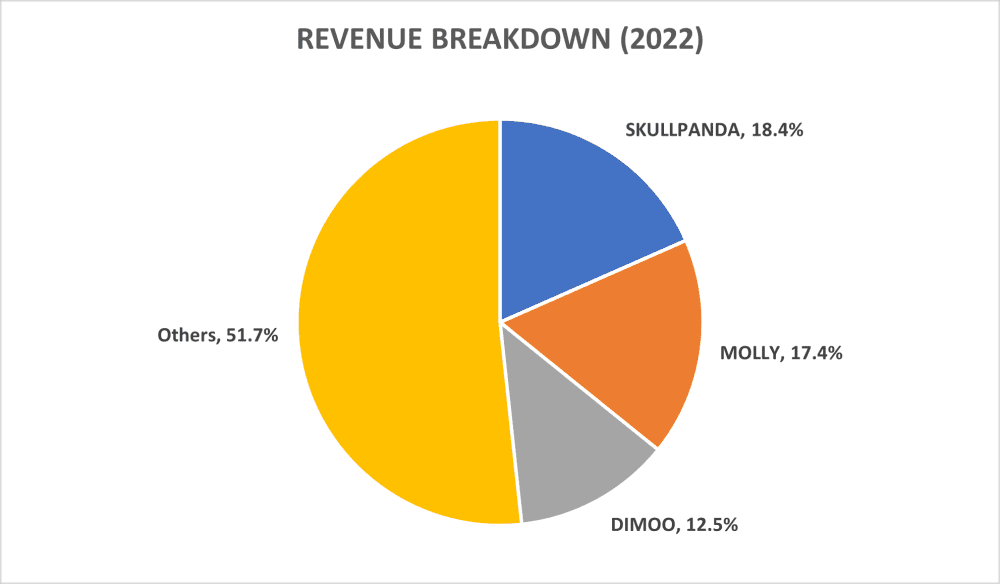

SKULLPANDA may just be a weird-looking random character to you. But what if I told you that this one character belongs to a company called Pop Mart and raked in RMB851.6 million for the company in 2022 alone. Together with MOLLY and DIMOO, these characters contributed close to half of Pop Mart’s revenue in 2022. The revenue contribution from SKULLPANDA looks on track to exceed the one billion renminbi mark in 2023 based on its 1H2023 revenue of RMB526.4 million.

Listed in 2020 on the Hong Kong Stock Exchange, Pop Mart specializes in the creation and sale of collectible toys. These toys, known as pop/art/designer toys, are designed to be showcased and are primarily tailored to appeal to 15 to 40-year-olds who value the aesthetic aspect of these toys.

Business model

Pop Mart’s toy offerings can be categorized into three groups: proprietary intellectual properties (IPs), exclusive licensed IPs, and non-exclusive licensed IPs. Within the proprietary IPs, you’ll find popular characters like SKULLPANDA, MOLLY, and DIMOO, for which the company holds complete IP rights, enabling them to create and market these toys. As for exclusive licensed IPs, the rights are contingent on specific contracts and are temporary in nature. Meanwhile, non-exclusive licensed IPs, such as Mickey Mouse, Minion, and HELLO KITTY, have the freedom to collaborate with other entities besides Pop Mart to produce and distribute toys.

The margins of proprietary IPs are usually higher than the other two categories as Pop Mart pays IP licensing fees for the latter two. As a result, Pop Mart has gradually shifted its attention to selling more proprietary IP toys. The revenue contribution from proprietary IPs increased from 25.9% in 2017 to 65.0% in 2022.

Designer toys used to carry a hefty price tag until they underwent a democratization process, becoming available in ‘blind boxes’. The concept of blind boxes draws inspiration from Gashapon, the capsule toys distributed via vending machines. A typical set of blind boxes comprises 12 individual palm-sized figurines, all identical in appearance from the outside. This gives shoppers a sense of uncertainty and excitement as they unveil its contents. In some cases, a blind box series may include a rare hidden design, found in just one out of 144 blind boxes. The supply of this toy is artificially limited. As a result, some shoppers may spend substantial amounts of money in pursuit of obtaining this rare item, evoking parallels with gambling. This element of chance can be addictive, motivating repeat purchases.

Besides blind boxes, Pop Mart also offers its toys in other formats including action figures, ball-jointed dolls, and accessories. However, blind boxes are the most prevalent, but they introduce an element of controversy.

Financials

Pop Mart sells its toys via different channels including retail stores, roboshops (vending machines) as well as online and wholesale channels. In 1H2023, Pop Mart had 395 retail stores and 2,328 roboshops globally. About 10.3% of its revenue in 2022 was obtained from wholesales and other channels while the remaining portion was approximately equally contributed by online and offline channels.

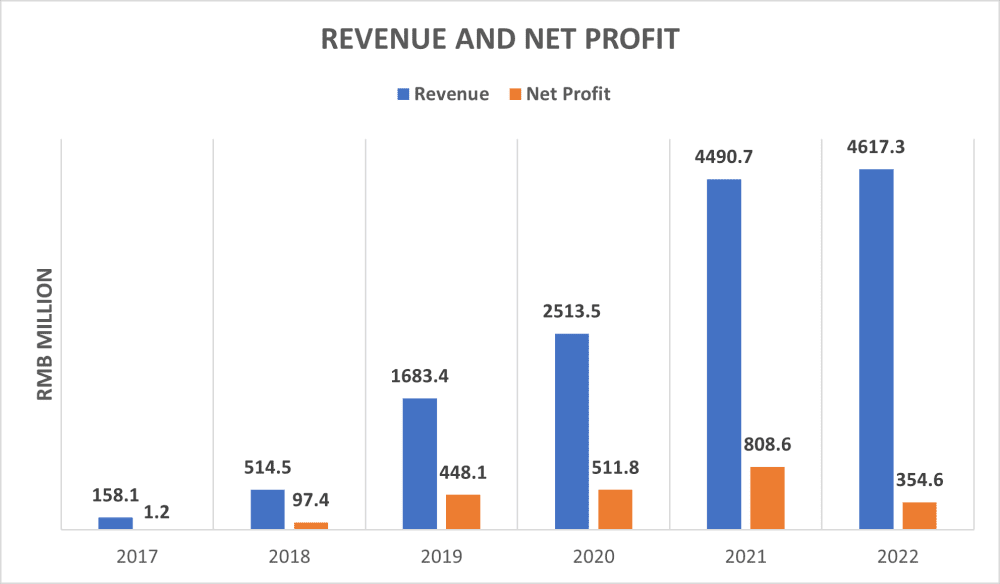

From 2017 to 2022, the company recorded impressive compound annual growth rates (CAGRs) of 96.4% and 212.0% in revenue and net profit respectively. As of 2022, Pop Mart derives 90.2% of its revenue from mainland China but was hit by strict lockdowns there during the year. As a result, revenue and net profit were affected in 2022. In line with its revenue growth, Pop Mart is the leading retail pop toy player in China; its market share there grew from 8.5% in 2019 to 13.6% in 2021.

Its market outside of mainland China is also growing fast. Revenue contribution from Other Regions increased from just 0.4% in 2017 to 9.8% in 2022. The company has been expanding overseas to support its growth as the domestic economy slows down. The number of overseas retail stores and roboshops increased from 24 and 98 in 1H2022 to 55 and 143 in 1H2023 respectively.

In 1H2023, revenue from mainland China and Other Regions grew 10.7% and 139.8% year-on-year. Overall revenue and net profit excluding extraordinary items grew 19.3% and 53.3% year-on-year respectively. Revenue growth was offset by the drop in revenue from online channels in mainland China.

The company may not continue to grow at such high growth rates in the future as they decline to more realistic levels. Pop Mart also shed more than 90% of its market capitalisation when its share price dropped from HK$105.00 in February 2021 to HK$10.20 in October 2022.

With the current share price hovering at around HK$23, the company’s P/E ratio stands at a high 87.9 times when excluding extraordinary items from the calculation. This valuation appears to be overextended, considering a more sustainable annual growth rate of around 20%.

Pop Mart’s gross and net profit margins have averaged at 60.8% and 15.4% over the past three years since its listing. Both margins are dropping as Pop Mart was hit by higher commodity prices that were caused by the pandemic-induced supply chain disruptions. The production of most of its toys heavily relies on plastic resins, which are derived from crude oil which have been impacted by higher oil prices. Margins also dropped due to the increased complexity of the design and the manufacturing process.

| Year | 2020 | 2021 | 2022 |

|---|---|---|---|

| Gross profit margin | 63.4% | 61.4% | 57.5% |

| Net profit margin | 20.4% | 18.0% | 7.7% |

The company aspires to emulate Disney and recently unveiled its 40,000-square-meter theme park, Pop Land, in Beijing, China. This theme park resembles a lively carnival and offers visitors a more extensive and immersive retail experience. Additionally, the company plans to introduce a mobile game, reminiscent of Animal Crossing, in 2024, as a strategic move to diversify its revenue streams and bolster its intellectual properties (IPs) within the consumer market.

Key risks

One significant contrast between Pop Mart’s intellectual properties (IPs) and Disney’s Ips, for example, is the absence of distinct characters in Pop Mart’s creations. Pop Mart’s IPs are highly adaptable, seamlessly integrating into a wide range of designs. In contrast, Disney’s IPs, like the Disney Princesses, often exhibit distinctive personalities and quirks. As a result, it is typically easier for the average consumer to relate to characters like them as opposed to, for instance, SKULLPANDA. Pop Mart’s IPs, in comparison, have a limited narrative depth and fewer stories associated with them.

Pop toys typically have shorter product lifespans. For instance, revenue generated from one of Pop Mart’s characters, PUCKY, saw a substantial 62.2% decline, dropping from RMB 315.3 million in 2019 to RMB 119.1 million in 2022. At the same time, successful pop toy IPs from Japan, such as KAWS and Bearbrick, have been thriving since 1999 and 2002. Nevertheless, there’s a possibility that the Pop Mart craze may fade more quickly than anticipated, akin to the rise and fall of the Beanie Babies trend during the 1990s. Hence, Pop Mart must maintain a continuous cycle of innovation to introduce new, popular IPs and designs.

Pop Mart products are relatively expensive. Toys are also non-essential items, especially during times of economic hardship.

| Type | Price |

|---|---|

| Blind box | RMB69 (US$15.99) |

| Figurine | Varied, up to RMB6,999 (US$1,399.90) |

| Ball-jointed doll | RMB429 (US$74.99) |

| Accessories | Varied |

The Chinese government may not always be the most pro-business and may implement restrictions that impact Pop Mart’s business models –in particular, blind boxes, to protect youth and consumers. Europe, for example, is in midst of regulating video game loot boxes (digital blind boxes) for better consumer protection.

The fifth perspective

Pop Mart has experienced remarkable growth, primarily fueled by its innovative approach to the collectible toy market and a strong presence in mainland China. However, challenges loom on the horizon, with the sustainability of their business model, fluctuations in market capitalization, and the absence of distinct IP compared to industry giants like Disney. High product pricing, coupled with the non-essential nature of their toys, poses economic challenges. Supply chain disruptions and government restrictions add further uncertainty. To ensure long-term success, Pop Mart must continue to innovate and diversify, as seen in their theme park and mobile game ventures, adapting to changing market dynamics and consumer preferences. The future of Pop Mart as a turnaround growth stock or a fleeting fad hinges on their ability to navigate these challenges and maintain consumer appeal.